The situation facing working Australian households is bleak.

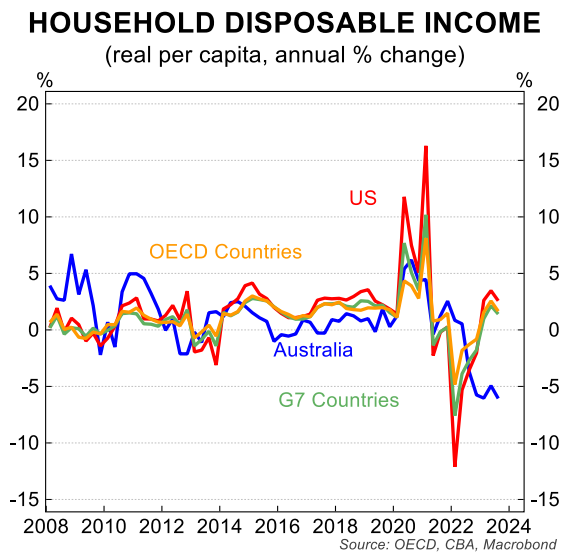

Australian real per capita household incomes collapsed by 6.0% in 2023, the sharpest decline in the world:

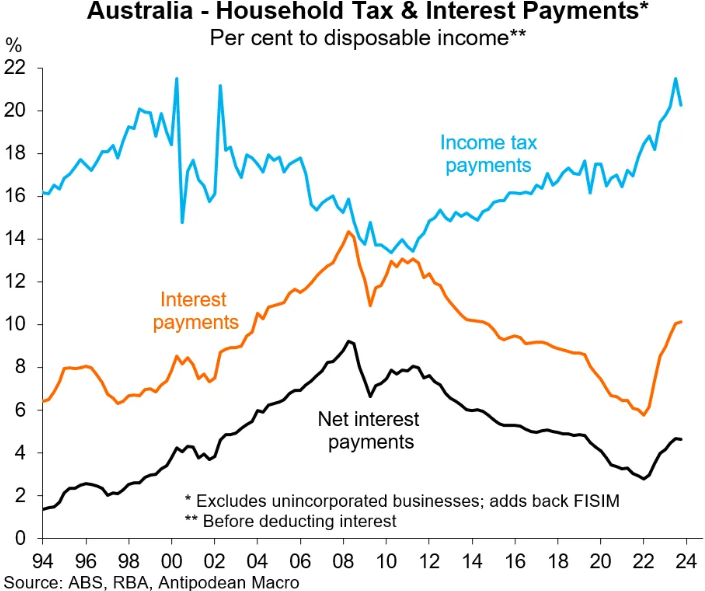

The world’s sharpest increase in mortgage and tax payments was the primary cause of this decline in Australian household incomes:

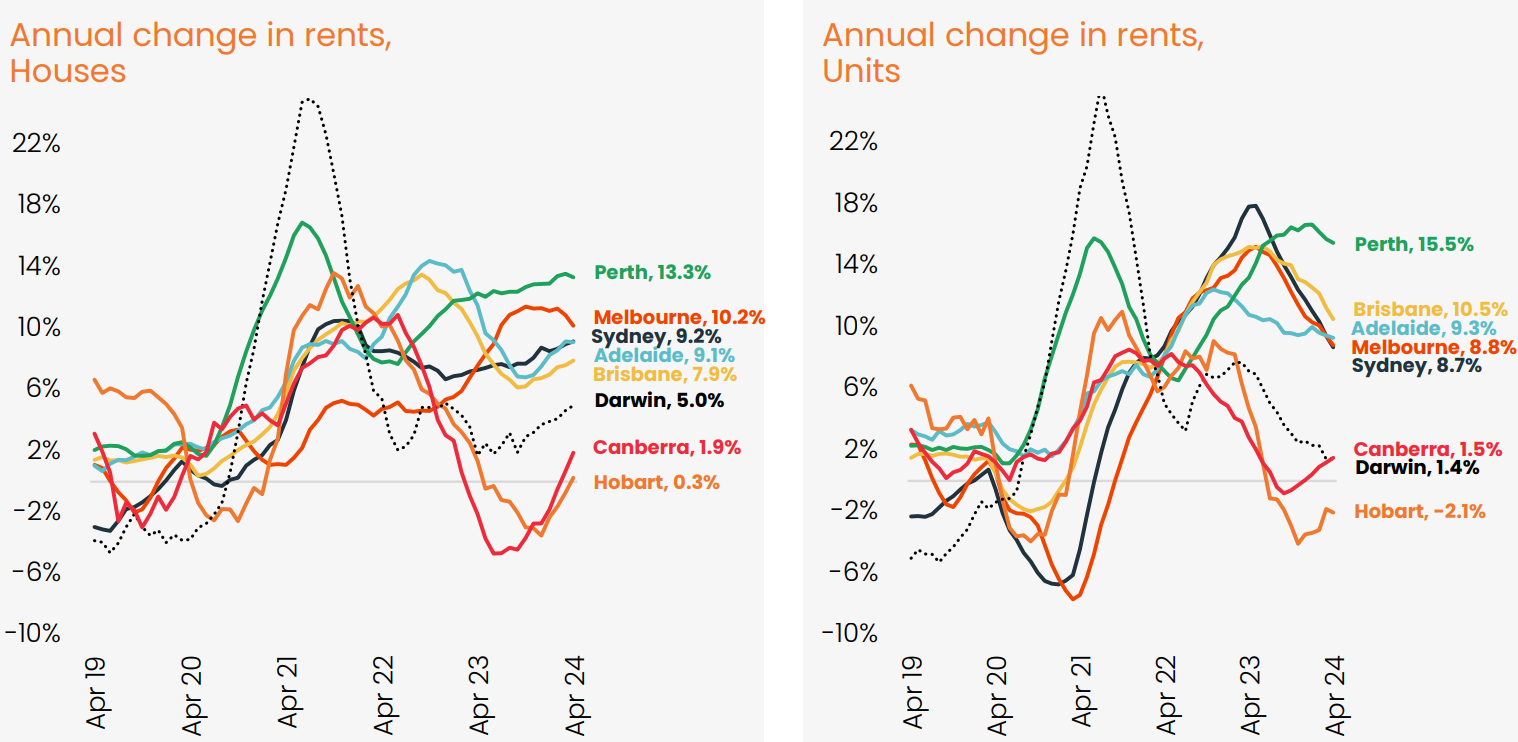

Tenant households across the major Australian capital cities are also suffering from extreme rental inflation, which is further draining household disposable incomes:

Source: CoreLogic

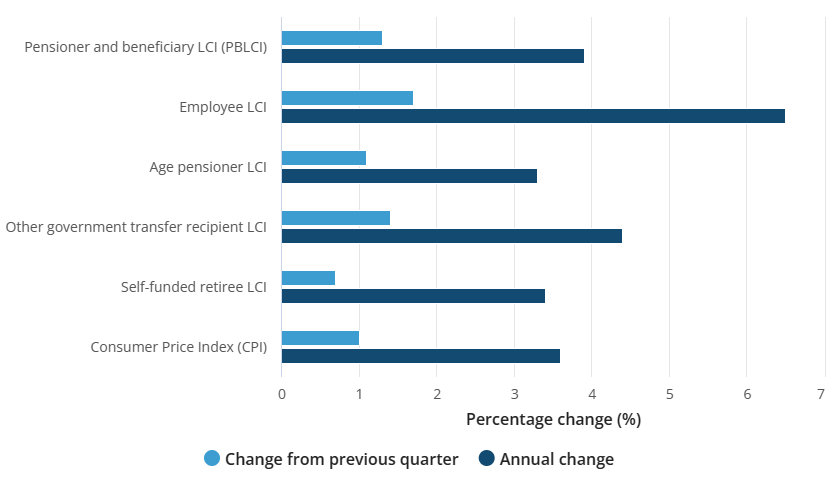

Meanwhile, the latest cost of living index from the Australian Bureau of Statistics (ABS), released on Wednesday, showed that employee households suffered a massive 6.5% increase in their cost of living in the year to March 2024:

Source: ABS

This increase in cost of living easily exceeded the 3.6% increase in CPI inflation and the 4.2% increase in wage growth over the year to December (the latest available observation).

Simply put, rising mortgage payments, rising rents, rising tax obligations, and rising general cost of living (such as energy and insurance costs) are all exerting significant pressure on Australian households.

As expected, households have responded by slashing discretionary spending.

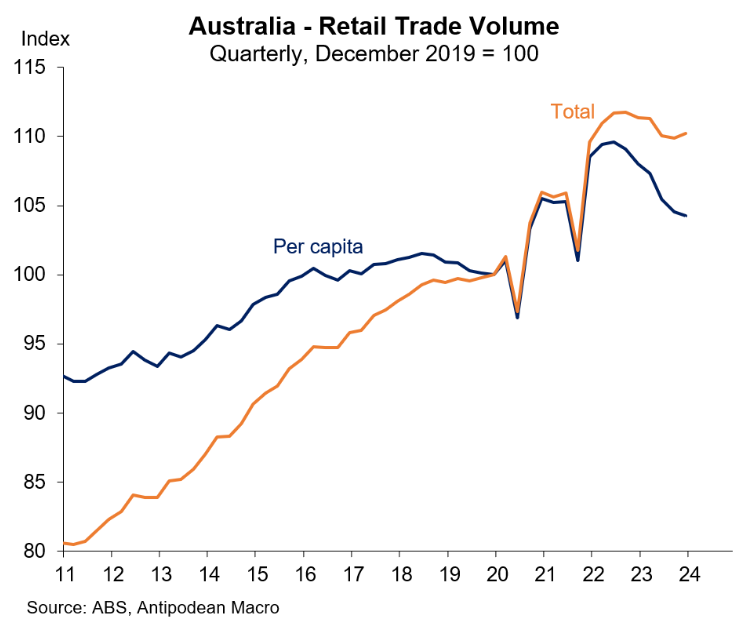

This week’s retail sales data for March showed that real per capita retail sales have collapsed, driven by falling spending on consumer durables:

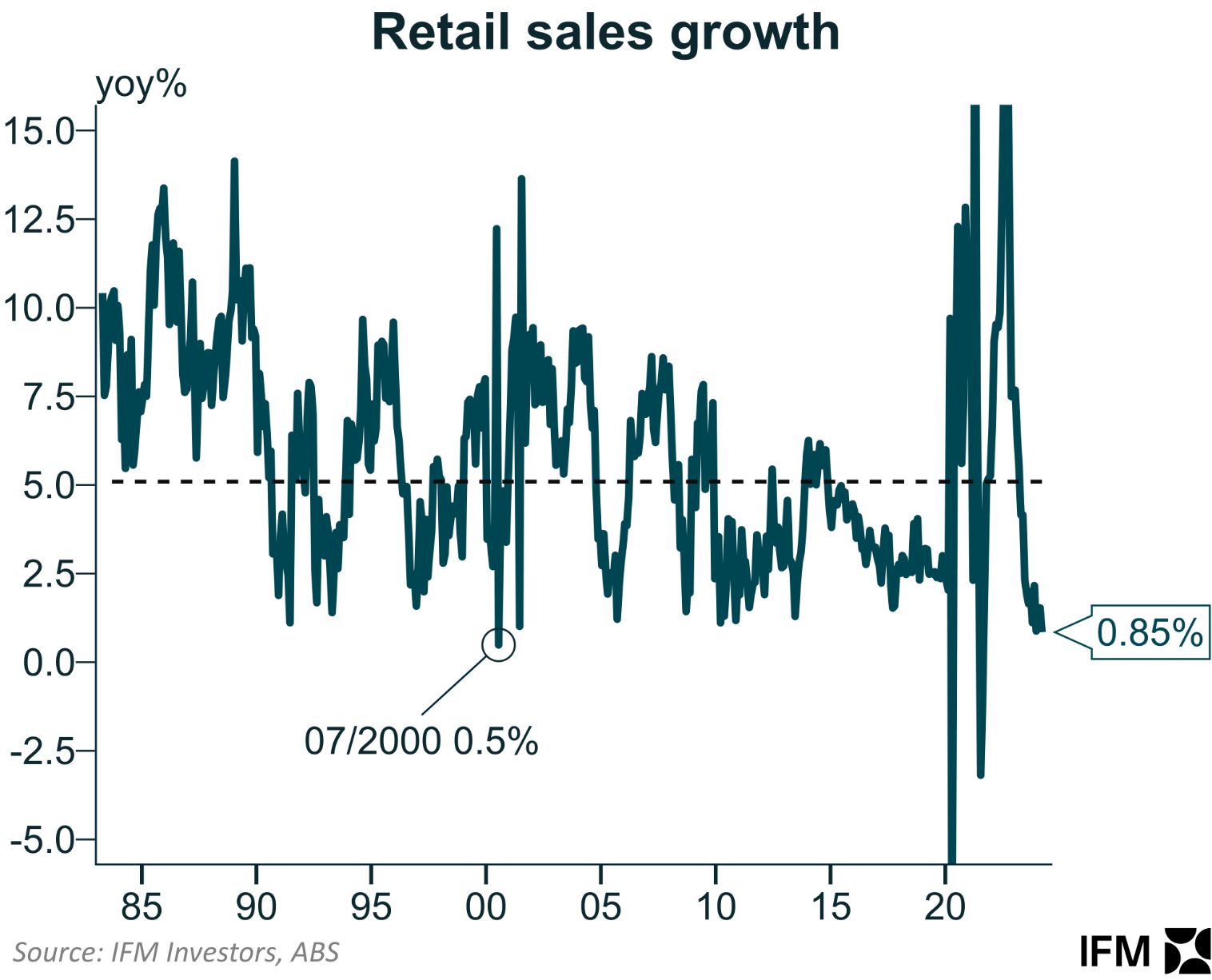

The 0.8% annual nominal rise in retail sales was the lowest annual growth since 2000 outside of the pandemic:

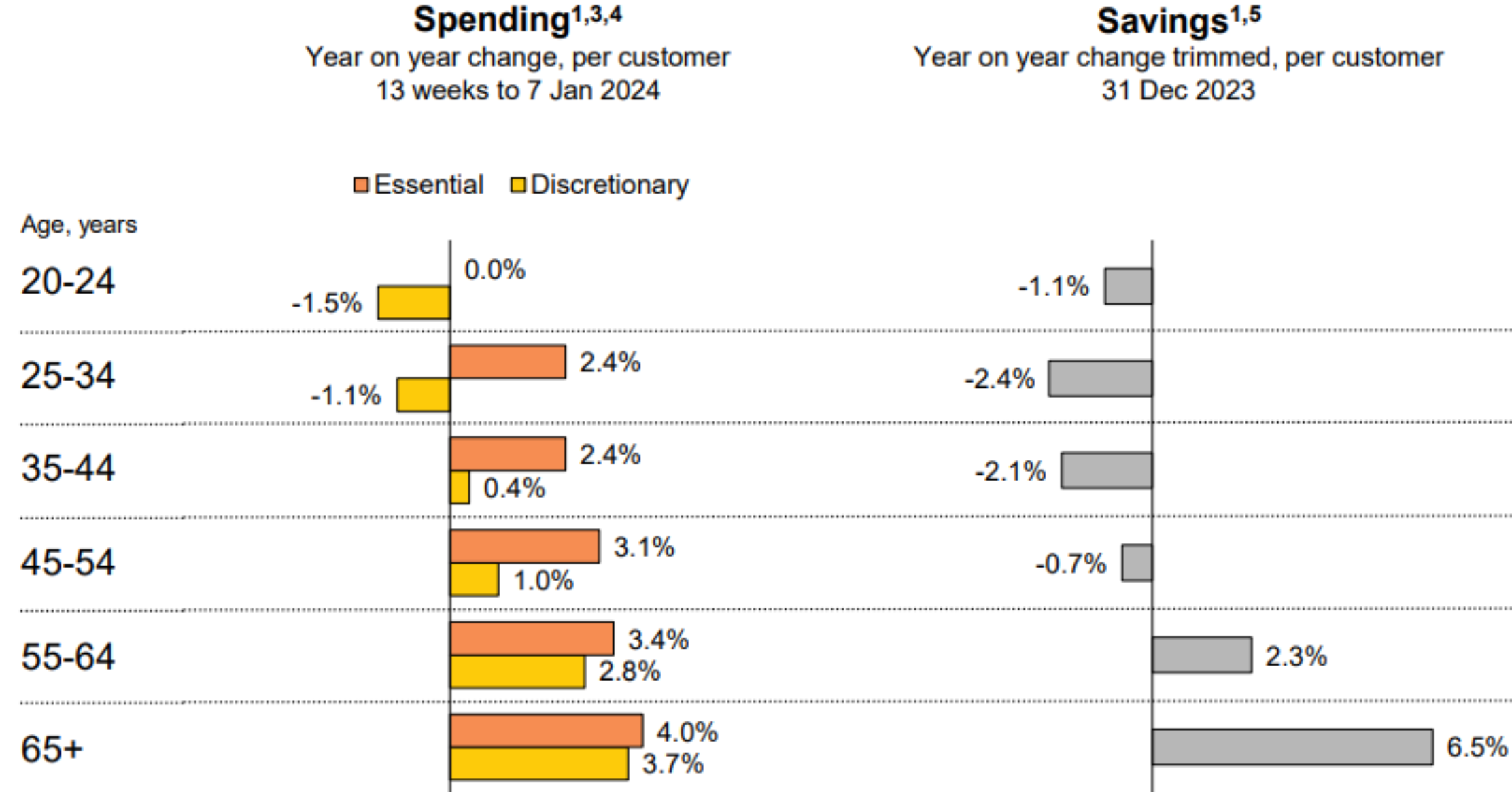

The only segment of the population that is doing fine are older Australians who mostly own their homes outright, do not pay income taxes, rents, or mortgages, and have accumulated massive savings over the pandemic:

These older Australians are insulated from the pain being inflicted on working Australian households and are driving overall household spending.

The above data illustrates why the Reserve Bank of Australia will be highly reluctant to lift interest rates further, given that consumer spending is the main driver of the economy.

Doing so would have no impact on the spending habits of older, mortgage-free Aussies, while inflicting even more pain on the roughly one-third of households with owner-occupier mortgage debt.

Given the precarious state of household finances (baby boomers excluded), the next move in interest rates is still likely to be downward.