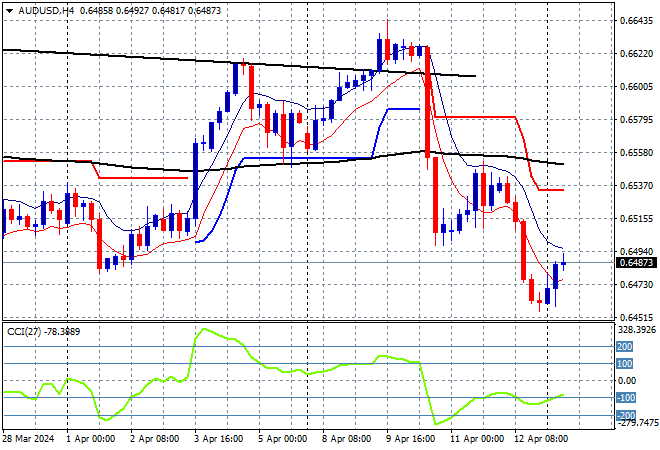

A rocky start to the trading week with most stock markets in Asia losing significant ground in response to the escalation in conflict across the Middle East, with the spike in USD on Friday night seeing some undollars clawback their losses. Commodities and bond markets are still high in volatility while traders await tonight’s US retail sales print after a very firm CPI and jobs report which could see further USD upside. The Australian dollar is trying to rebound after its 100 pips plus reversal as it retraces back to just below the 65 cent level this afternoon.

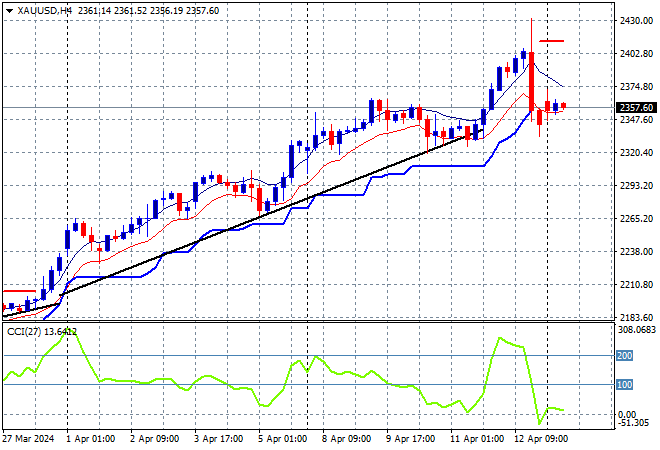

Oil prices are just holding on following the weekend of attacks across the Middle East with Brent crude still well above previous weekly resistance but retracing slightly below the $90USD per barrel level while gold is trying to hold on after its own relatively minor selloff on Friday night, currently looking weak at the $2350USD per ounce level:

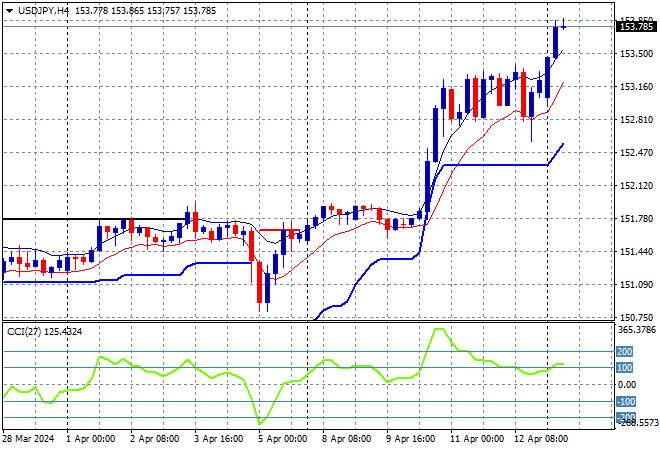

Mainland and offshore Chinese share markets are still quite divergent with the Shanghai Composite lifting more than 1% while the Hang Seng Index is down more than 0.7% to 16590 points. Japanese stock markets were unable to take advantage of a weaker Yen, with the Nikkei 225 down more than 0.7% at 39232 points with the USDJPY pair breaking out on USD strength above the 153 level:

Australian stocks had minor losses with the ASX200 closing 0.4% lower at 7752 points while the Australian dollar is trying to lift itself off the floor after the Friday night rapid selloff, but is still just below the 65 cent level:

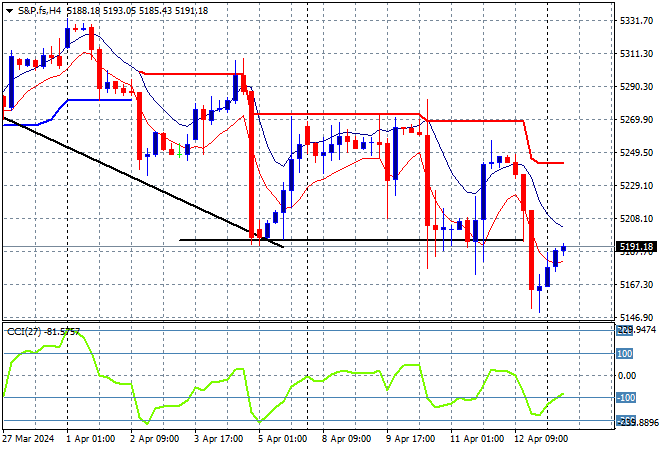

S&P and Eurostoxx futures are trying to fight back from their selloff on Friday night as we head into the London session with the S&P500 four hourly chart showing price action still in a technical downtrend through a series of steps as it fails to recover from short term resistance:

The economic calendar starts the trading week with the latest US retail sales print.