Australian households are struggling financially.

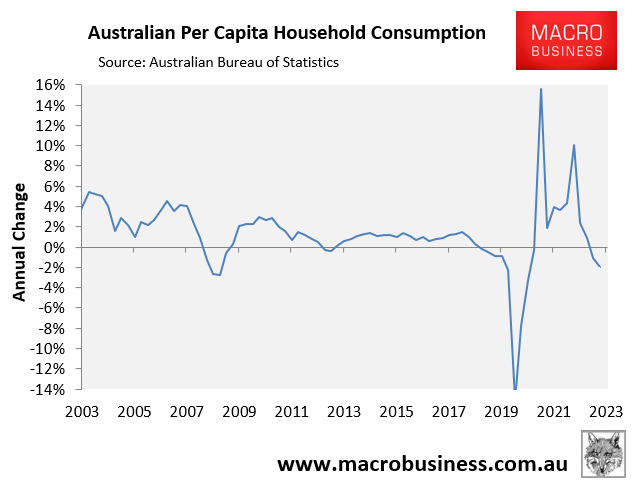

Real per capita household final consumption fell by 2.5% in 2023, driving the nation’s per capita recession:

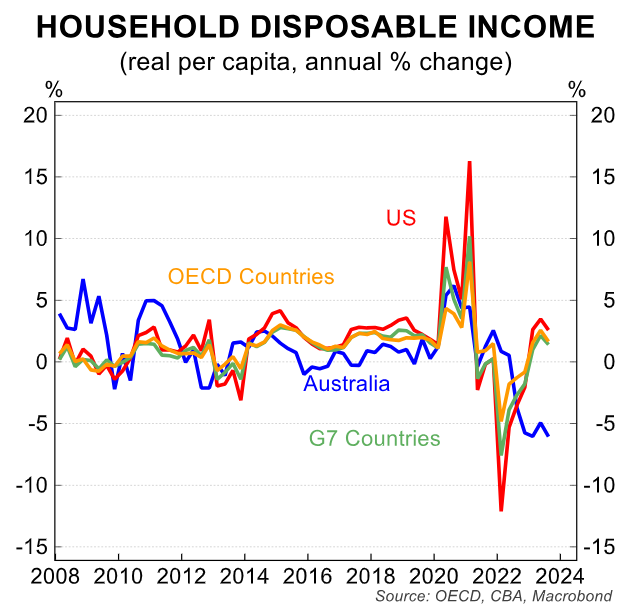

Australian real per capita household disposable income also fell by 6% in 2023, ranking among the sharpest declines in the world:

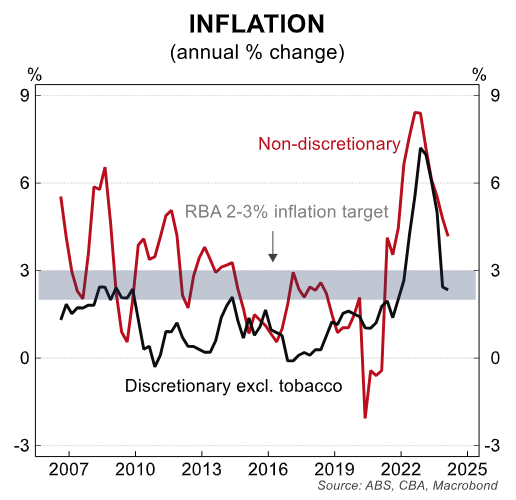

Stephen Wu at CBA’s analysis of Wednesday’s CPI inflation data reveals that non-discretionary items, where consumer demand is less able to respond to higher prices, are the main drivers of inflation in Australia:

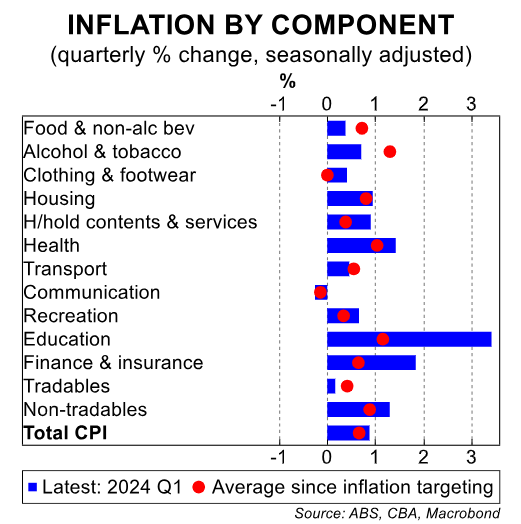

The upside surprise predominantly came through on the non-discretionary and non-tradables components of the basket.

Non-discretionary prices rose by 4.2%/yr, while discretionary (ex. tobacco) inflation eased to 2.3%/yr. Non-tradables inflation was 5.0%/yr, whereas tradables came in at just 0.9%/yr…

Discretionary (ex tobacco) inflation continued to ease, with the annual rate at 2.3%, within the bottom half of the RBA’s inflation target. The ABS considers tertiary education a discretionary item; this has kept discretionary inflation higher than otherwise.

Non-discretionary inflation moderated to 4.2%/yr, the slowest pace of growth since Q3 21, but remains well above its pre-pandemic pace. In the quarter, prices rose by 1.3%. The key drivers for the increase were rents, secondary school fees, health services and products, and insurance.

The upshot is that the key drivers of inflationary pressures in Australia are centred around parts of the CPI basket where consumer demand is less able to respond to higher prices.

Eight of the top 10 contributors to the quarterly increase in prices were non-discretionary items: rents, secondary education, health services and pharmaceuticals, new dwelling construction costs, vegetables, and insurance and other financial services. The two discretionary items rounding the top 10 were tertiary education and domestic travel.

It is a classic case of inflation in everything you need, dis-inflation in everything you want.