The ANZ CoreLogic Housing Affordability Report has asked whether 40% of gross household income on a mortgage is the new 30% of gross household income on a mortgage:

ARE 40’S THE NEW 30’S FOR MORTGAGE SERVICEABILITY?

The rapid increase in the cash rate target, and subsequent mortgage rate rises, have squeezed borrowing capacity and affordability for prospective buyers.

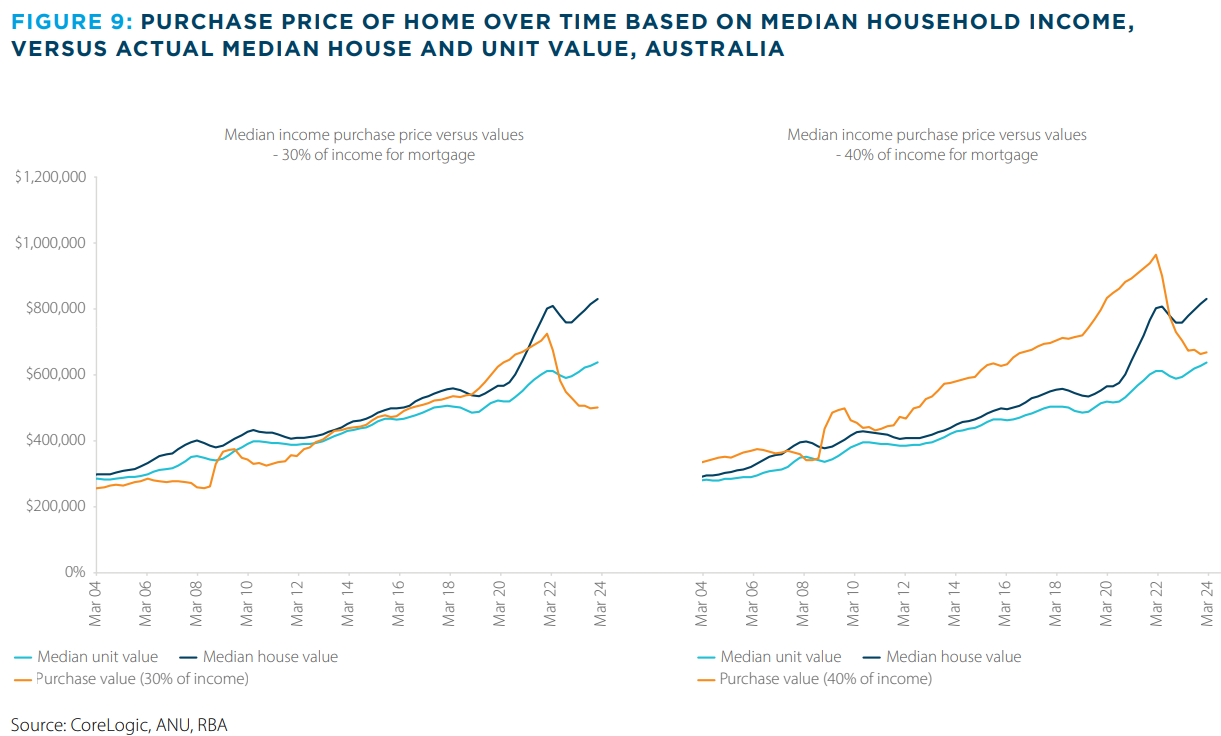

Based on the latest estimate of median annual household income nationally ($100,244 before taxes), and assuming 30% of this income is used on mortgage payments at current average variable rates, an affordable dwelling purchase would be around $503,000.

However, ongoing increases in housing values mean that this affordable purchase price is below most actual dwelling values, with the median Australian unit price around $640,000, and the median house price around $834,000 across Australia.

CoreLogic estimates that only 17.4% of dwelling stock is valued below $503,000.

This is shown in Figure 9, which compares the purchase price that is feasible for the median national income level at 30% or 40%, against the actual median house and unit value over time.

For the same household, extending the portion of income to service a mortgage allows more options, particularly in the unit segment. Under current interest rates, of around 6.3%, dedicating 40% of median household income to mortgage payments would push the dwelling price purchase level to $670,000.

CoreLogic estimates that almost 37% of housing stock has a value of $670,000 or less. This is far from the median income household being able to afford the median dwelling value in Australia (which is currently $773,000).

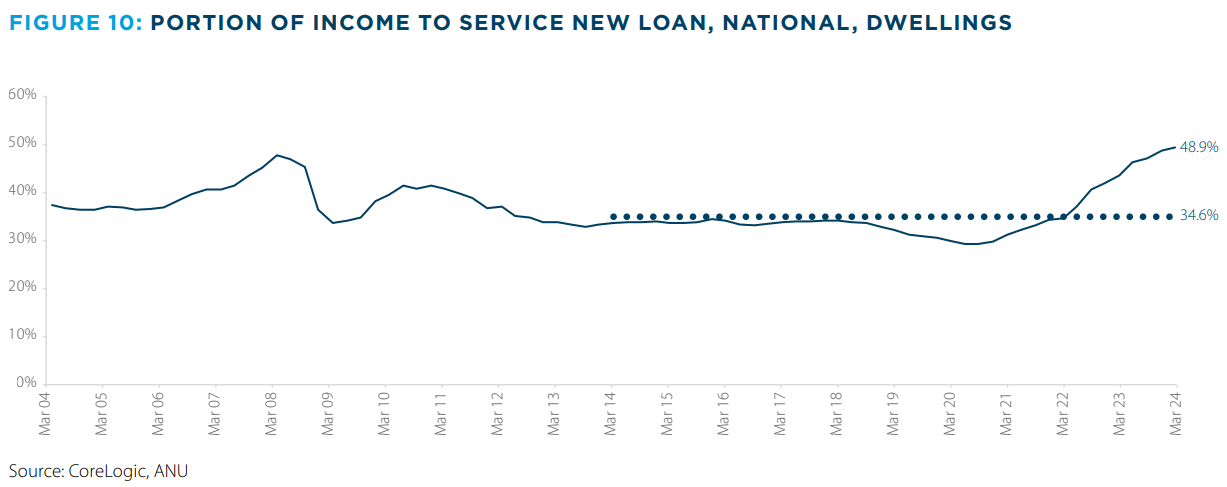

PORTION OF INCOME REQUIRED TO SERVICE A MORTGAGE HITS SERIES HIGH

With home values reaching new record highs in November last year, and the cash rate rising a further 25 basis points in the same month, the portion of median income needed to service a new loan on the median dwelling value reached 48.9% nationally.

This is a record high for the series, and sits well above the previous decade average of 34.6%.

While the median income household is unlikely to be spending this high a portion of income on mortgage costs, it reinforces how out of step home values are with current income and interest rate levels.

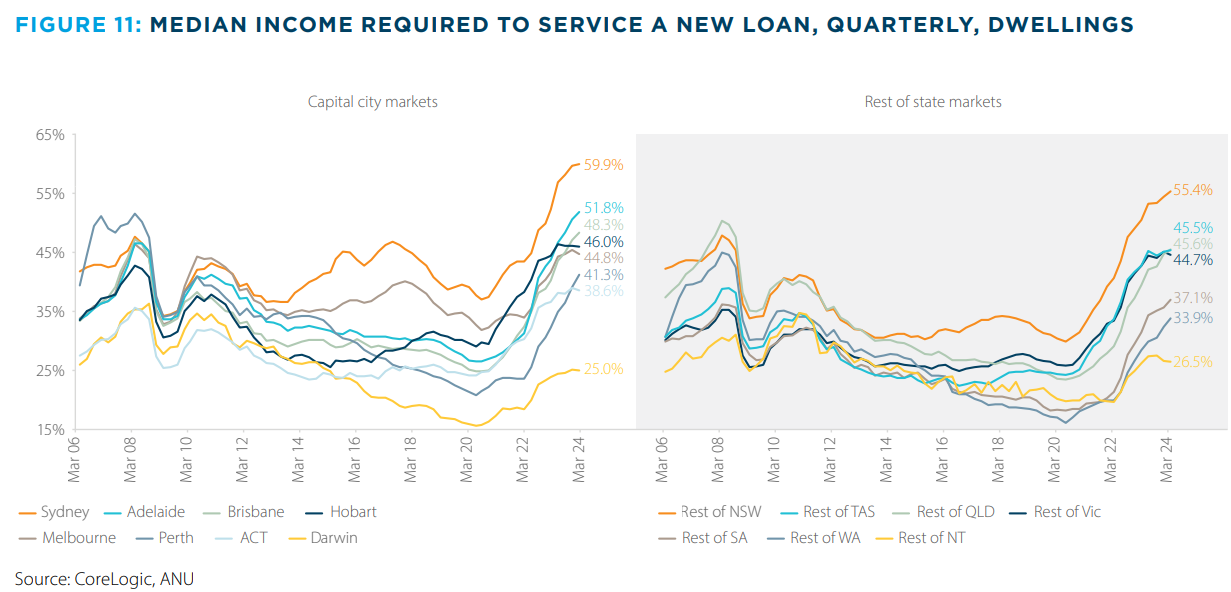

Figure 11 shows the time series of the portion of income required to service a new mortgage for the greater capital city and rest of state regions.

The mortgage serviceability indicator is highest across NSW, with just under 60% of median income required to service a new loan on the median Sydney dwelling value, and 55.4% in regional NSW.

Looking ahead, there is little prospect for the mortgage serviceability indicator to move back into the 30%-range any time soon.

This is because the cash rate is not expected to be cut until late 2024, and home values have continued to rise, even amid relatively high interest rate settings.

Based on current levels of income and dwelling values across Australia, and assuming a 20% home loan deposit, mortgage rates would need to fall to around 4.7% to get serviceability just under 40% of median income.

Several mortgage providers have introduced 35- and 40-year mortgages in a bid to lift borrowing capacity.

For example, NAB affiliate Ubank extended a 35-year mortgage that was previously exclusively available to new buyers to those wishing to refinance.

Australian Mutual Bank, Pepper Money, and RACQ Bank also now offer 40-year mortgages.

Extending a 25-year loan to 40 years saves around $460 per month on a $500,000 mortgage. As a result, it significantly boosts borrowing capacity.

However, it would cost $377,000 more in interest over the loan’s term, implying that more people would retire with housing debt.

It is classic ‘extend and pretend’ policy aimed at turning Australian housing into feudal serfdom.