On Saturday morning, I was interviewed by Luke Grant on Radio 2GB where I ran through the latest national accounts data from the Australian Bureau of Statistics (ABS) and explained why the Reserve Bank of Australia’s (RBA) employment forecasts are way too optimistic.

The upshot is that Australia’s labour market is deteriorating far quicker than the RBA anticipated, which will force rate cuts later this year.

Below are highlights from the interview.

Leith van Onselen:

Australian households are going backwards at a rate of knots.

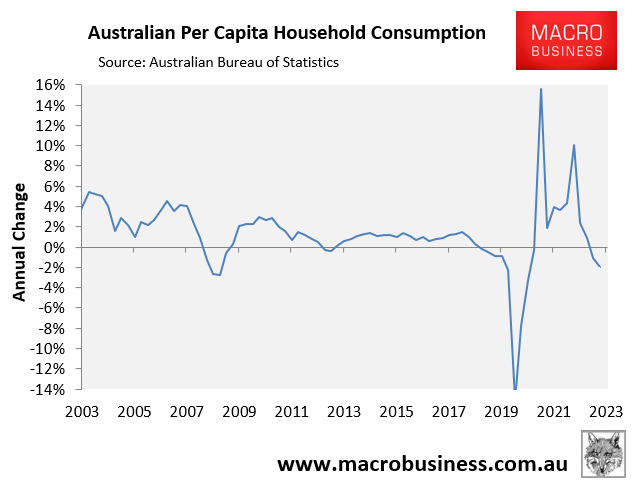

Real per capita household consumption plunged by 2.5% last year, which was a lot worse than what the Reserve Bank had forecast.

In its November Statement of Monetary Policy, the Reserve Bank forecast that household consumption before adjusting for population growth would be 1.1%. It then revised that down in February to 0.4%. And it ended up coming in at 0.1%.

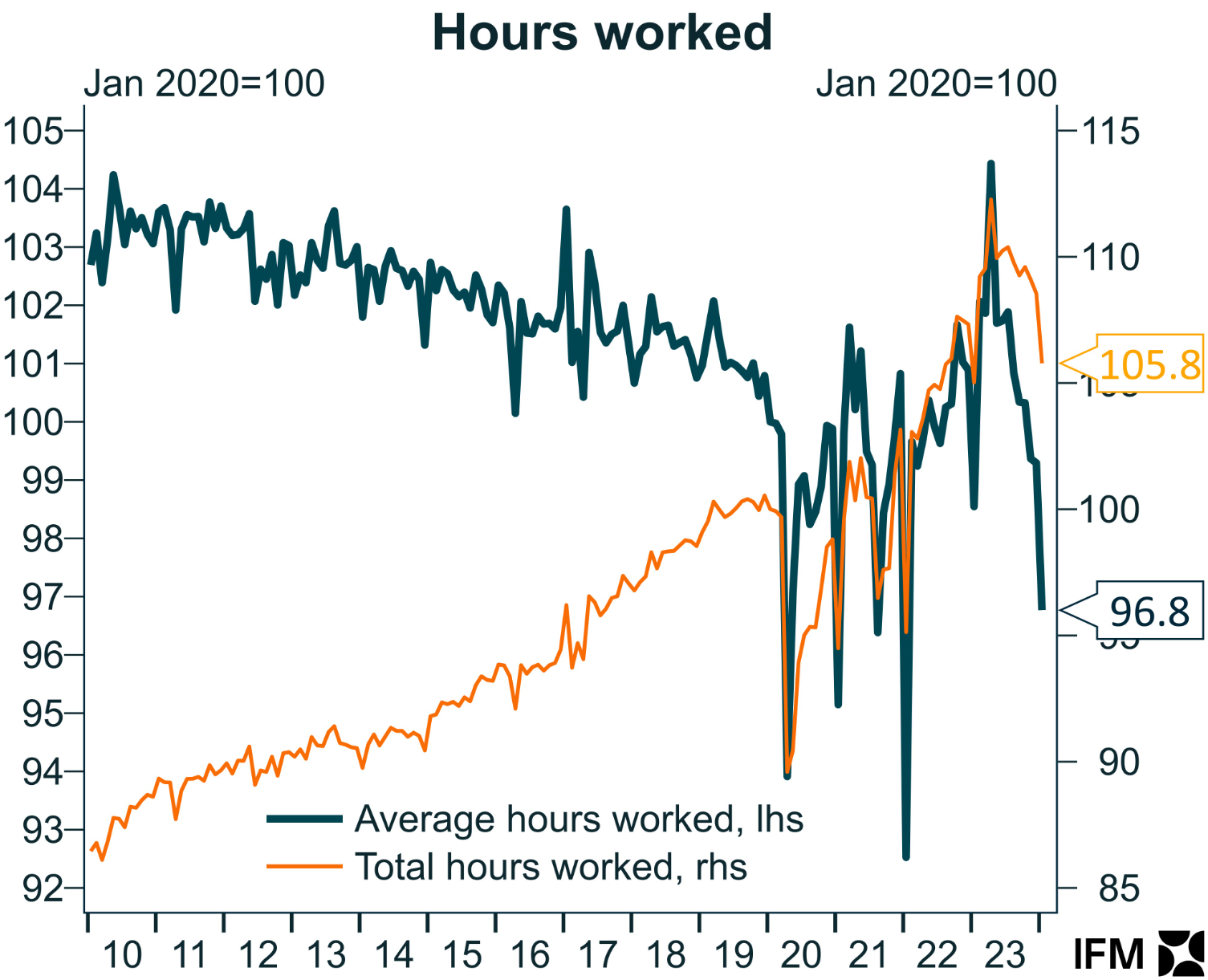

So basically, the household sector is a lot weaker than anticipated. Consumers are cutting back a lot harder than it expected. This has been reflected in weak retail sales, the number of hours worked in the economy has collapsed over the last 6 months.

Source: Alex Joiner

The only silver lining to all this is it means that the Reserve Bank is more likely to cut interest rates in the second half because the economy is stalling worse than what the Reserve Bank had expected.

Luke Grant:

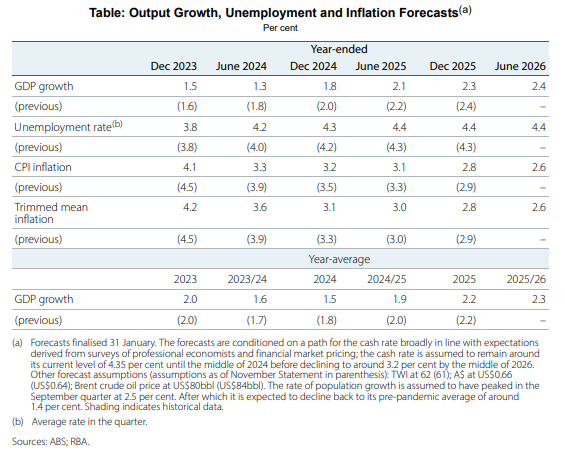

You wrote through the week that the RBA’s February Statement of Monetary Policy projected that unemployment would end this year at 4.3% and only peak at 4.4% next year:

You say that shortly after these forecasts were released, the ABS released the January labour force survey, which revealed Australia’s unemployment rate had gone to 4.1%. And you say the internals were even worse.

But if it was meant to top out at 4.4% and be 4.3% at the end of the year, and it’s already at 4.1%, you make the point that unemployment is going to be a significant driver of rate reductions. Is that right?

Leith van Onselen:

The Reserve Bank is drinking the Kool Aid if it thinks that the unemployment rate is going to peak at 4.4%. It was already 4.1% as of January, with 11 months to go to hit the RBA’s 4.3% forecast.

All the indicators show that the unemployment rate is going to shoot up.

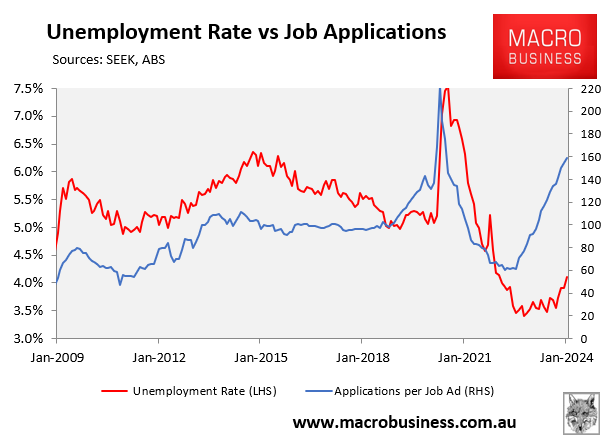

There’s a survey that was released on Thursday by Seek and what that shows is the number of applicants per job advertisement has soared far above the pre-pandemic level.

And when you plot that against the unemployment rate, it shows that it’s a really good leading indicator.

It tells you that the unemployment rate is going to shoot up over the coming months. Maybe not necessarily next month because there is always numberwang, but if you take a six month perspective, it’s going to shoot up.

I firmly believe that Australia’s unemployment rate is going to be closer to 5% by the end of the year. Not necessarily at 5%, maybe 4.8%, but certainly not 4.3% and not peaking at 4.4% like the RBA anticipates.

All this means is that, if the unemployment rate hits 4.3% in May or June, we will already be way ahead of what the RBA was expecting. And it will force them to have to cut rates quicker because it’s just another sign that the economy is slowing a lot faster than what it expected.

Pretty much every economic indicator that’s come in the last 3 months has been worse than what the Reserve Bank forecast.

Luke Grant:

Let me understand that. If you predict unemployment will be closer to 5% than 4.3% at the end of the year, is that driven by having rates higher for too long?

Is it the population issue that you and I discuss here every week?

What’s caused things to go pair shaped more than they projected and sooner than they projected?

Leith van Onselen:

There are two things, and you sort of alluded to it.

First, they probably didn’t need to do the interest rate hike in November, to be quite frank. The economy is slowing quicker than they expected, which means that employers don’t need to hire as many workers. So, demand and job ads have been falling.

The flip side of that is we’re also running this extreme immigration policy. Labour supply is growing faster, and according to CBA estimates, we need to produce nearly 35,000 jobs a month just to soak up the extra labour force that’s coming in mostly through migration.

So, demand is weak at the same time as labour supply is growing massively because of mass immigration.

And you put those two things together, and it’s a powder keg for unemployment because you’re going to have supply growing faster than demand, which means higher unemployment.