Finally, somebody else is making sense on iron ore:

Iron ore prices have run too hard and are now susceptible to a battery mineral-style collapse amid an imminent surge in supply and questions over demand for Australia’s largest export, investment manager Yarra Capital predicts.

If true, that could trigger a $US50 a tonne drop in iron ore prices to $US80 a tonne from their present level of around $US121.20 a tonne, nearly halving the profits generated by BHP and Rio Tinto, and slashing S&P/ASX 200 aggregate earnings by 10 per cent.

The fund manager warned that iron ore markets are not adequately attuned to the wave of new supply coming from Africa’s Simandou region next year, which – unless mitigated by output cuts elsewhere – will push the physical market into a surplus of as much as 10 per cent.

Meanwhile, demand from China, which represents about 70 per cent of the global seaborne market, is slowing as the world’s No. 2 economy shows signs of maturity and saturation.

…“Rather than waiting for history to actually repeat, investors would be wise to look through the current temporary earnings strength in iron ore stocks and reposition to avoid what could potentially be carnage.”

It’s not just Simandou. Australian and Brazilian expansions will add another 100mt before most Pilbara killer volumes arrive.

The major miners have lost their supply discipline at the worst possible moment.

The demand outlook is equally dire as China goes off its apartment “completions cliff”, from which its steel demand will never recover.

This is 160mt of new ore, plus Chinese steel demand crashing by about 100mt.

That’s a potential 300mt swing in the seaborne market. A surplus 50% larger and more persistent than the iron ore surplus of 2015, when prices hit $37.

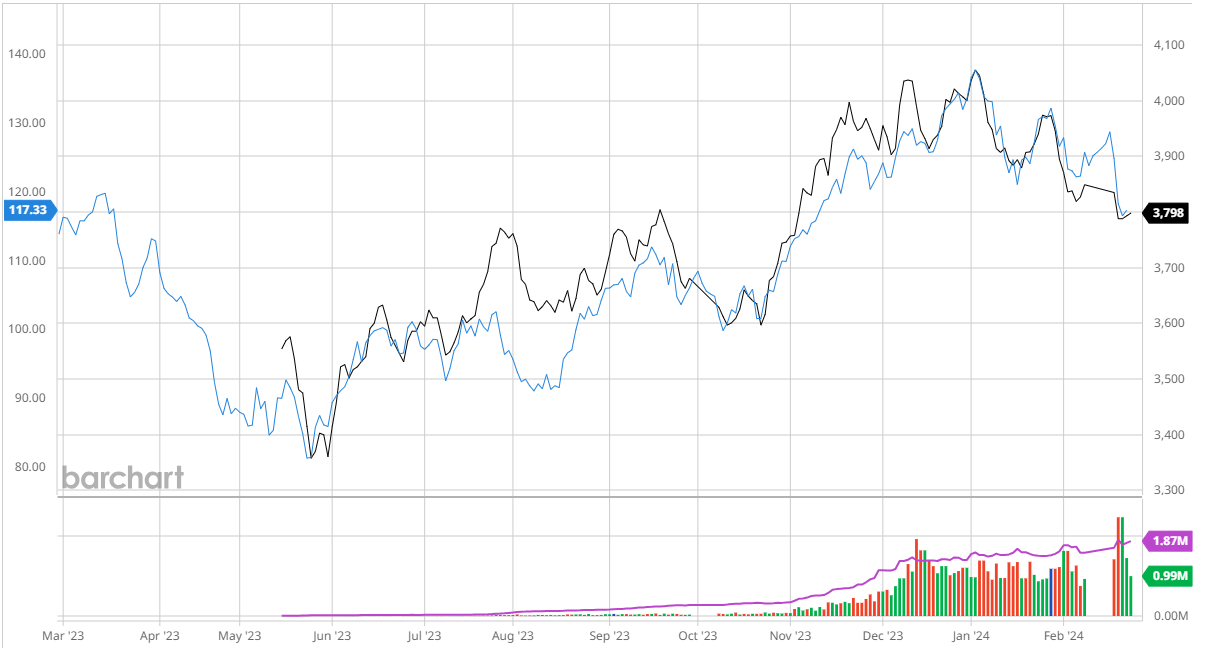

In the meantime, prices are still struggling with May rebar and SGX futures stalled:

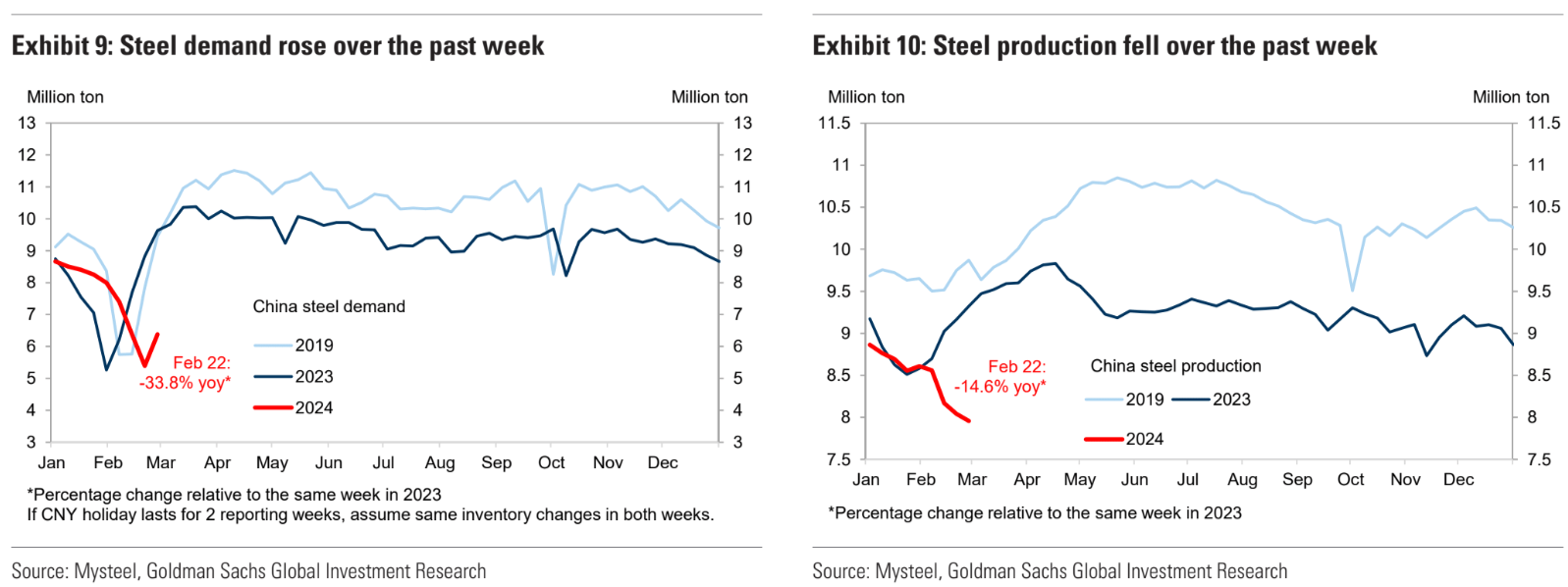

The latest MySteel steel output data is apocalyptic. LNY fogs the demand side. But the supply side is off a cliff even though it should not be affected by LNY:

MySteel data can be a bit wild, and we’ll need to see CISA data for mid-Feb in a few days for corroboration before panicking.

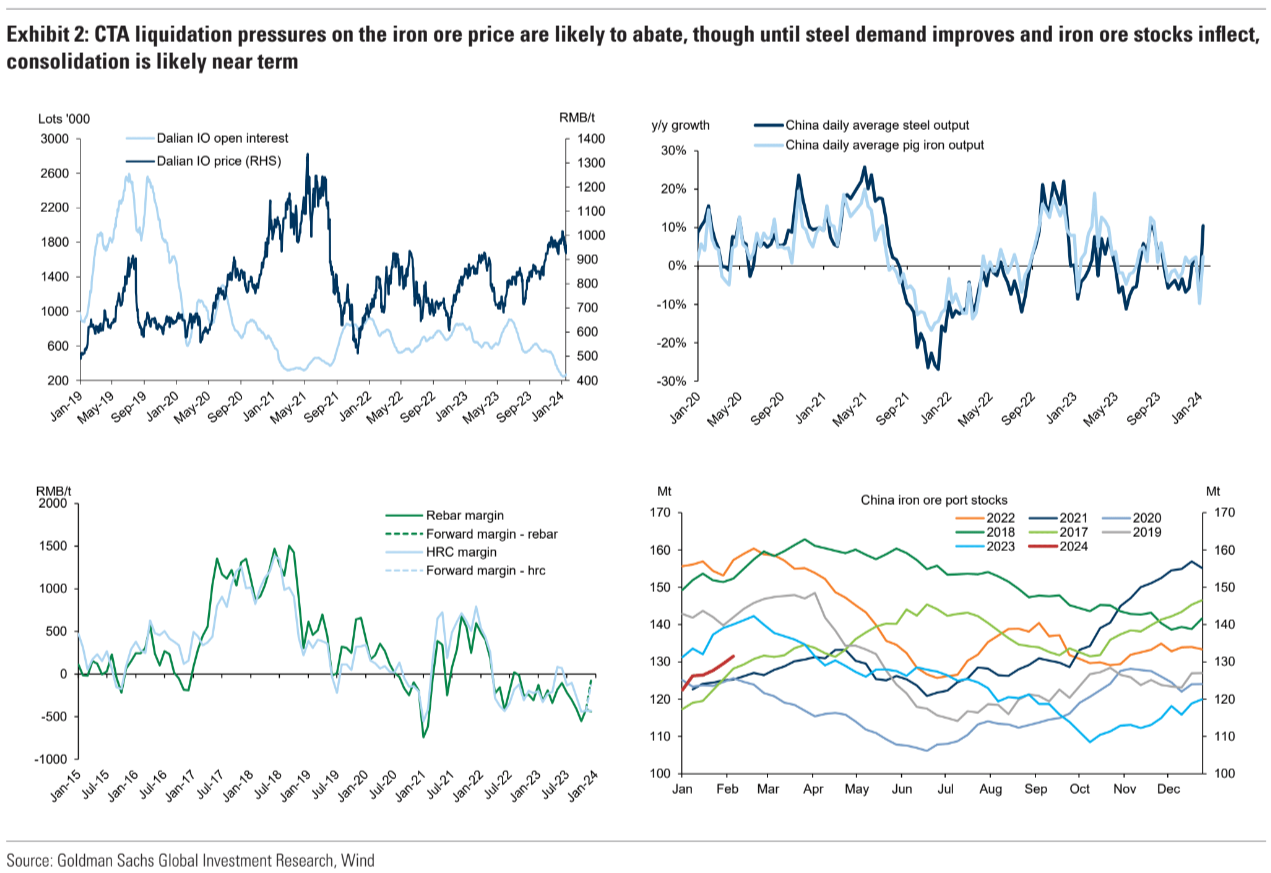

Goldman sees the recent iron ore weakness as a CTA liquidation:

Iron ore liquidation. Over the past month iron ore prices have fallen sharply, with the front end SGX contract down 8%.

We are now within touching distance of our 3M price target ($115), having gsignalled this downside path mid-January.

We do not however expect this sell-off to extend materially from current price levels, with consolidation in the near term.

The sell-off in iron ore has primarily been tied to CTA long position liquidation, though micro trends onshore have neither offered much counteraction.

Port iron ore stocks have risen more ytd than in recent years, up just over 12Mt, which compares to just 4Mt and 6Mt builds over the equivalent period in 22’ and 23’.

This has in turn reflected an environment of only modest recovery in hot metal production after maintenance depressed utilisation rates at the turn of the year, with continued negative mill margins limiting the incentive for the typical seasonal recovery in utilisation rates.

Apparent steel demand has been in modest contraction ytd though steel inventories remain at relatively modest levels.

For now we continue to expect the iron ore market to tighten into Q2 as seasonally stronger onshore steel demand (and production) support an inflection into deficit state.

In that context, on that base case fundamental path, we see limited downside to iron ore pricing from current levels into March.

Absent a significant supply shock or more significant policy stimulus supporting steel demand expectations, we believe the most likely path for price into March is one of consolidation close to current levels.

There is no evidence of CTA liquidation in those charts. In fact, Dalian open interest crashed before prices did.

There is evidence of a big rebound in EAF output in the top right chart as pig iron lags.

The Goldman argument makes sense if this is an ordinary year. However, the Chinese completion cliff is unpredictable, and demand may falter.

After all, iron ore is falling despite seasonal tailwinds and supply disruptions all over the place, including a cyclone closing Port of Dampier.

But LNY clouds all this data, so I wouldn’t draw any firm conclusions yet.