By Gareth Aird, head of Australian economics at CBA:

Key Points:

- We expect the RBA will leave the cash rate unchanged next week and see no chance of any other outcome.

- We anticipate the Board will retain a mild tightening bias, but the risk sits with the removal of the hiking bias.

- The RBA will publish their full suite of updated economic forecasts in the February Statement on Monetary Policy (SMP) at 2.30pm on Tuesday.

- We expect the RBA to lower their end-2024 inflation forecast to a little above 3%. And we anticipate they will forecast inflation returning to the mid-point of the target band by mid-2026.

- The RBA’s end-24 unemployment rate forecast is likely to be nudged up a little and we expect the GDP growth forecast in 2024 to be downgraded.

- RBA Governor Bullock will hold a press conference at 3.30pm on Tuesday – an hour after the decision is handed down. This will now be a regular feature after each Board meeting.

- The Governor will appear before the House of Representatives Standing Committee on Economics on Friday (9/2) at 9.30am.

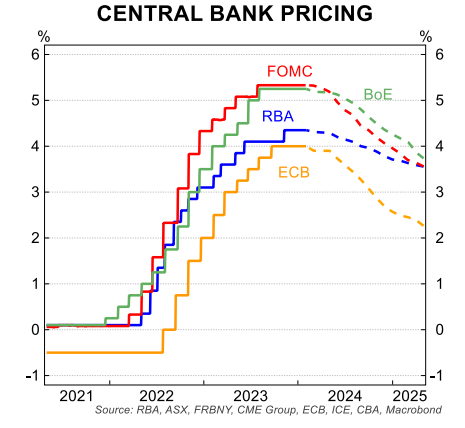

- We continue to expect an easing cycle commencing in September (we have 75bp of rate cuts in our profile in late 2024 and a further 75bp of easing in H1 25, which would take the cash rate to 2.85%).

A straight forward decision – all eyes on the statement:

The RBA Board meets next week for the first time in 2024. We expect the cash rate will be left on hold and see no chance of any other outcome.

The case to leave monetary policy on hold next week is stronger than at any point in the last two years.

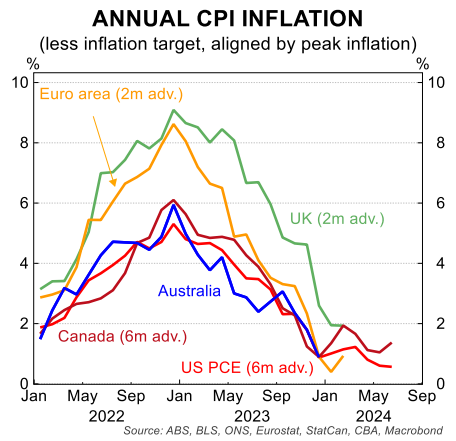

The Q4 23 CPI indicated that more progress has been made in returning inflation to target than the RBA expected when it published its inflation forecasts in November. In addition, economic growth is slowing more quickly than the RBA anticipated.

On inflation, headline CPI rose by 0.6%/qtr in Q4 23 – below the 1.0%/qtr outcome the RBA expected. The annual rate of inflation declined to 4.1% (0.4ppts below the RBA’s forecast of 4.5%).

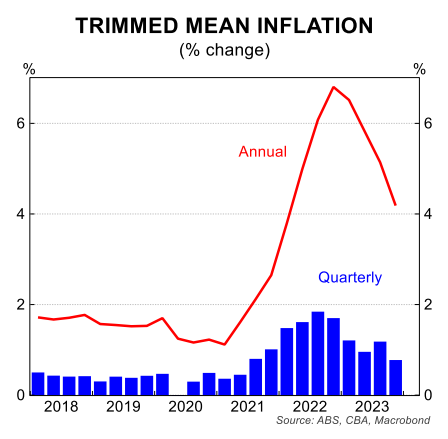

Underlying inflation was also softer than the RBA’s forecast. The trimmed mean CPI rose by 0.8%/qtr in Q4 23 – below the RBA’s forecast of 1.0-1.1%/qtr. The annual rate of underlying inflation fell to 4.2% in the December quarter (0.3ppts lower than the RBA’s forecast of 4.5%).

Economists are often judged by the accuracy of their forecasts. But some forecast misses are welcome. The RBA will very much embrace the inflation data printing below their expectations.

As we noted on Wednesday, the job of returning inflation to the 2-3% target band is not yet done. But the RBA is now on the home straight.

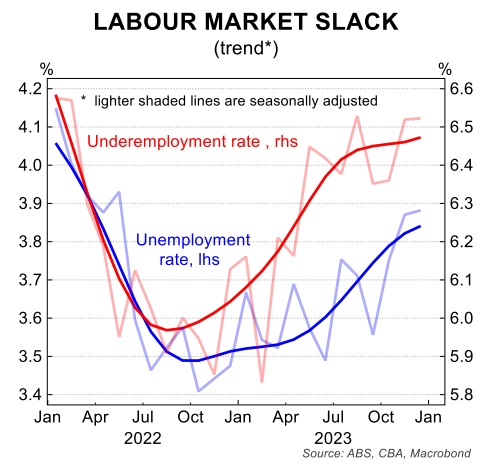

The faster pace of disinflation has been accompanied by slower economic growth compared to the RBA’s forecasts. And the labour market is now loosening a little more quickly than the RBA anticipated.

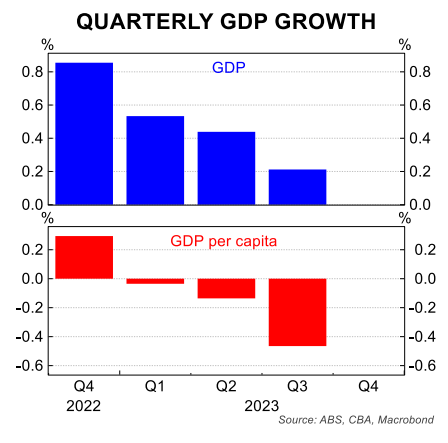

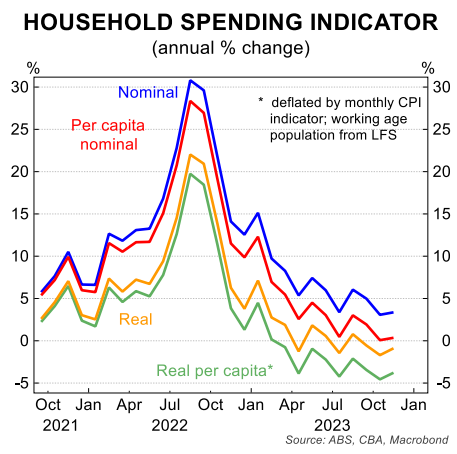

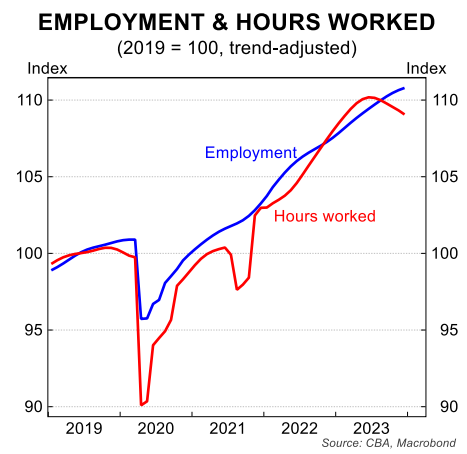

The Q3 23 national accounts, which printed the day after the December Board meeting, were particularly soft on the consumer side.

Real household consumption was just 0.4%/yr in Q3 23. Against the backdrop of ~2.5%/yr population growth there has been a big contraction in the volume of spend per person.

The RBA forecast real household consumption to be 1.1%/yr in Q4 23. For that outcome to materialise the volume of consumer spending would need to have increased by a large 0.9%/qtr in the December quarter. A flat or small increase in spend in Q4 23 looks most likely.

The unemployment rate, which is the key metric of the labour market, has continued to trend up. The unemployment rate was 3.9% in December and it averaged 3.83% over Q4 23.

For context, the RBA forecast the unemployment rate to average 3.8% over the December quarter, which covers the range of 3.75-3.84% on a two decimal basis. As such, the actual outcome of 3.83% was at the high end of the RBA’s point estimate.

Hiking bias likely to be retained, but it’s a close call:

The focus for market participants will be on the RBA’s communication and updated economic forecasts, rather than the widely anticipated ‘on-hold’ decision. On that score, there will be changes to communication.

The post-meeting statement accompanying the decision will be issued by the Board, rather than the Governor. This raises the risk that we get a fresh statement next week rather than the usual ‘cookie cutter’ approach to the post meeting statement.

Markets will be most interested in the key paragraph pertaining to forward guidance and whether there is a shift away from the Board’s current tightening bias.

Recall in the December Statement the Governor reiterated that, “whether further tightening of monetary policy is required to ensure that inflation returns to target in a reasonable timeframe will depend upon the data and the evolving assessment of risks.”

The recent run of economic data will mean that behind closed doors the Board will be more confident that it does not have to act on its tightening bias. Indeed, the clear trends in the data pertaining to domestic demand, the labour market and inflation mean the arguments in favour of any further tightening are weakening by the month. This lends weight to the Board removing its hiking bias.

But the RBA has both dialled up and dialled down its inflation fighting rhetoric on several occasions over the past year. The Board likely thought and hoped its tightening cycle was over after it left the cash rate on hold in August last year following the Q2 23 CPI. But an upside surprise in the Q3 23 CPI saw the Board resume lifting the cash rate in November.

We suspect that this experience means the Board will not wish to jettison its hiking bias just yet.

The updated Statement on the Conduct of Monetary Policy, released on 8 December, is also worth considering. The Conduct of Monetary Policy now makes an explicit reference to the midpoint of the inflation target rather than simply the target range.

Specifically, it states that “the Reserve Bank Board sets monetary policy such that inflation is expected to return to the midpoint of the target” (our emphasis in bold).

We don’t believe that aiming for the midpoint of the target alters the Board’s reaction function. But this tweak lends weight to the Board holding onto its hiking bias for a little longer.

To be clear, we firmly believe the next move in the cash rate is down, which would be consistent with the removal of the RBA’s tightening bias. But we doubt at this juncture the Board has arrived at the same conclusion as us.

We also think that the RBA will wish to keep the tightening bias for a little longer for their communication strategy.

The Governor and Deputy Governor do not just communicate with market participants. They communicate with households, businesses and policymakers (i.e. government).

Maintaining a tightening bias will signal to the fiscal authorities that it’s too early to declare the inflation fight over. The RBA would not wish to see fiscal settings loosened until further progress on inflation has been made towards the target band.

In summary, we expect a tightening bias to be retained. But it may be a watered down version of the previous forward guidance. The risk of course is that the Board shifts to a neutral bias. If that were to be the case then it would signal the Board is closer to cutting the cash rate than we suspect they are.

Inflation forecasts to be revised materially lower:

The RBA will publish updated forecasts next week in the February Statement on Monetary Policy (SMP). We expect a downward revise to the inflation forecasts.

The Q4 23 outcome means mechanically the RBA will need to lower their near term inflation forecasts. But the RBA may go one step further and make an additional small downward adjustment to their inflation profile given the recent trends in household expenditure and the labour market.

We expect the RBA to forecast headline inflation to be 3.2% by end-2024 and underlying inflation to be a touch lower at 3.1%. The forecast profile will be extended out to mid-2026.

We anticipate the inflation profile over 2025 to mid-2026 will be a glide path to 2.5% (i.e. to the midpoint of the target band).

Some housekeeping on the RBA’s revamped communication:

Next week, the Board will move to the new format of longer but less frequent meetings. The Board meeting will be held over two days (5-6 Feb). The decision will be announced at 2.30pm on Tuesday, as has been the case previously.

As mentioned above, the post-meeting statement accompanying the decision will be issued by the Board, rather than the Governor.

A media conference will be held at 3.30pm (this will be the case from here after each meeting). This will allow the Governor to more fully explain the Board’s decision and the outlook for policy. It will also allow the Governor to ‘jaw-bone’ the market if the market reaction at 2.30pm is not consistent with the message the Governor intended to send.

The RBA will also release the February SMP at the same time as the monetary policy decision (i.e. 2.30pm Tuesday). The SMP will contain a full suite of updated economic forecasts. According to the Governor the ‘look and feel’ of the SMP will change. And the document will be shorter.

On Friday the Governor will appear before the House of Representatives Standing Committee on Economics.