Westpac with the note.

Since our last commodities update in mid–December, there has been a broad weakening of commodity prices but, as always, not all commodities performed in the same way. Our broadest commodities index (Westpac Exports Price Index) is down close to 5% over the last two months with thermal coal leading the way, falling 20% over that period. LNG prices have fallen 12% while met coal is down 6%. But not all energy prices have fallen since December, Brent crude is up almost 7% on the back of the broadening conflict in the Middle East with Houthi attacks in the Red Sea disrupting shipping activity. Iron ore prices are also down 7% but at US$126/t are still surprisingly resilient compared to wide held expectations for prices to weaken though 2023. The base metals complex is broadly flat, but this was driven by a 5% rise in aluminium and lead contrasted with a 3% fall in nickel. Meanwhile gold has rallied 2%.

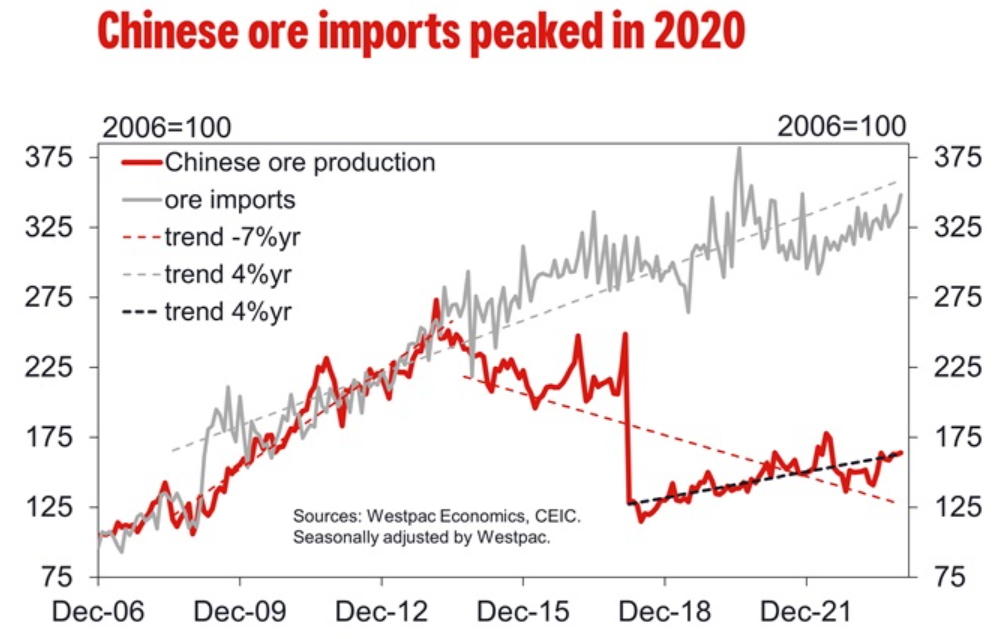

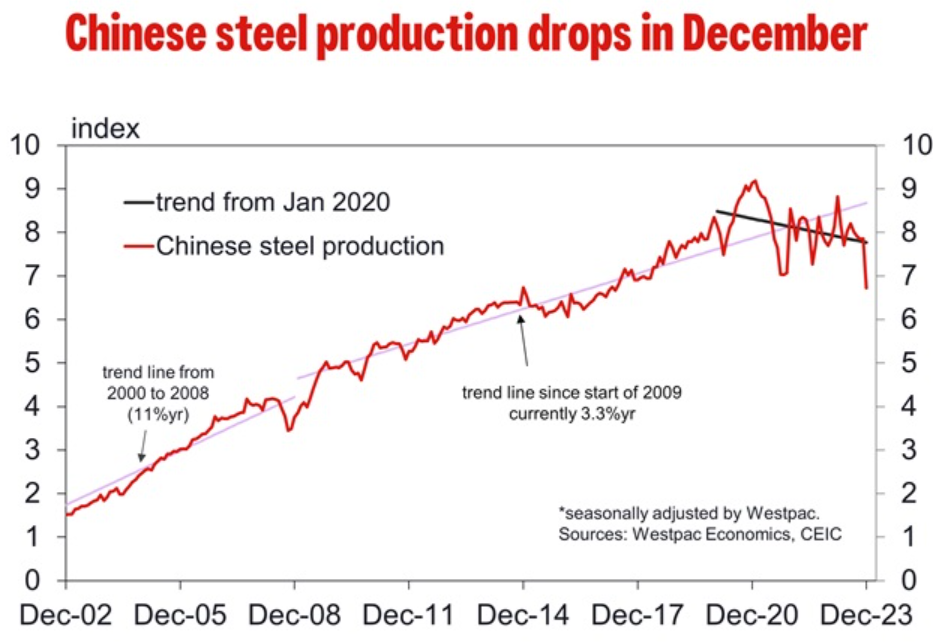

Given the ongoing troubles in the Chinese residential property market and construction industries, there is quite a bit of head scratching on why iron ore prices remain so robust. We have seen the number of foreclosed homes in China rise 43% in 2023 with 389,000 units impacted according to the China Index Academy. More recently, the Chinese administration had instructed heavily indebted local governments to delay or halt some state–funded projects as Beijing is trying to manage debt risks as it attempts to stimulate the economy. To top off 2023, the latest update on Chinese steel production was very disappointing with December output almost 11mt below our ‘forecast’ at just 67.44mt that was based on CISA data. We do note this is consistent with smaller, less efficient steel mills being shuttered, meaning the industry will hit the ‘just over 1bnt’ steel production cap that was imposed in 2023. Backing this up, the NDRC has noted that China will “continue to promote supply–side structural reform in the steel industry this year with a focus on high–end operations” and “will strictly control the increase in new steel capacity … (and) speed up a green transition” suggesting that this story should continue through 2024.