Statistics New Zealand on Wednesday released consumer price index (CPI) data for the December quarter, which came in below the Reserve Bank’s expectations.

Consumer prices rose 0.5% in the December quarter, leaving prices up 4.7% over the past year. That was significantly below the 5.6% CPI inflation recorded in the year to September 2023 and the lowest annual inflation read in more than two years.

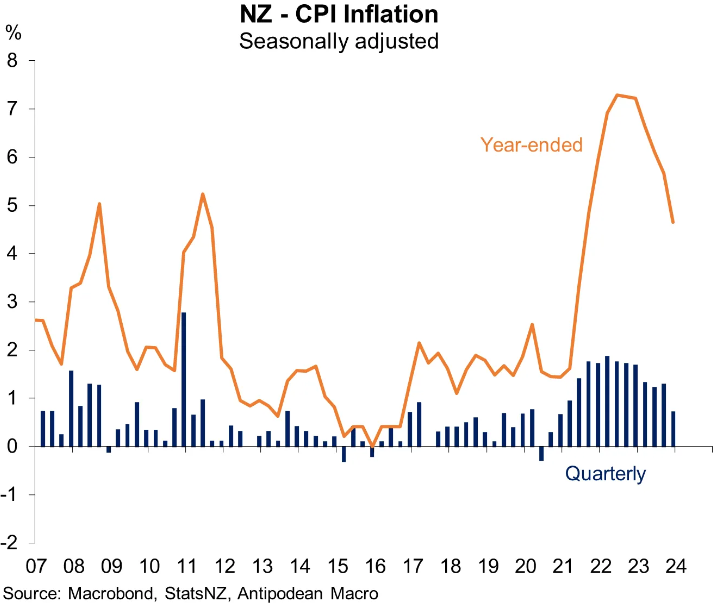

The below chart from Justin Fabo at Antipodean Macro illustrates the sharp deceleration in CPI inflation in seasonally adjusted terms:

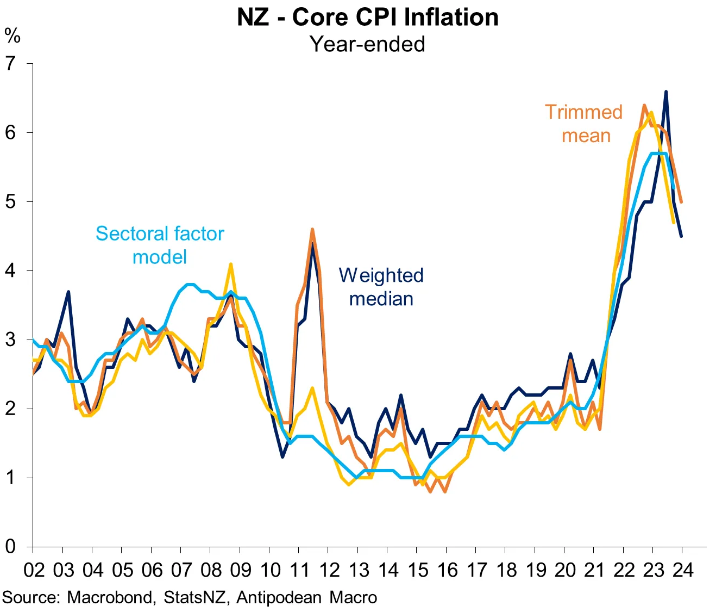

As shown by the below chart from Fabo, “measures of ‘core’ inflation slowed further on a year-ended basis”:

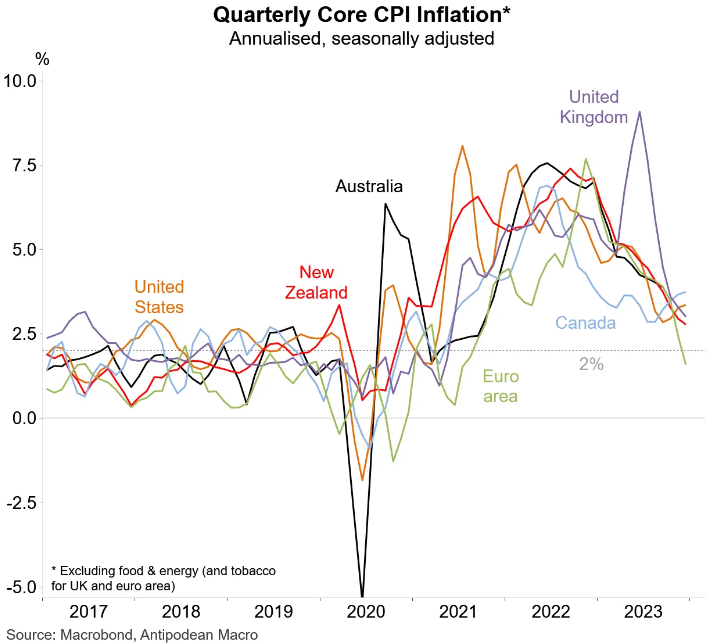

New Zealand’s disinflation is also following the trend of other advanced nations:

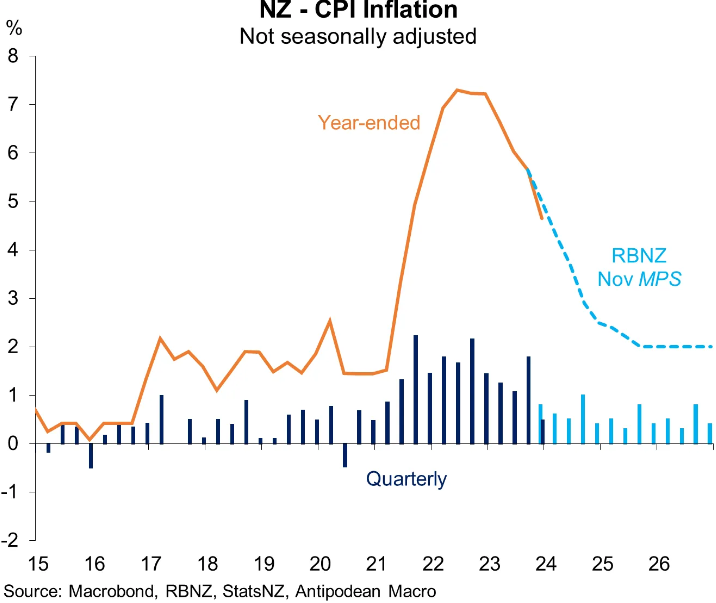

Most importantly, New Zealand’s inflation is running below the Reserve Bank’s last published forecast, which was finalised back in November.

In fact, inflation has been lower than the RBNZ has been expecting for most of the past year:

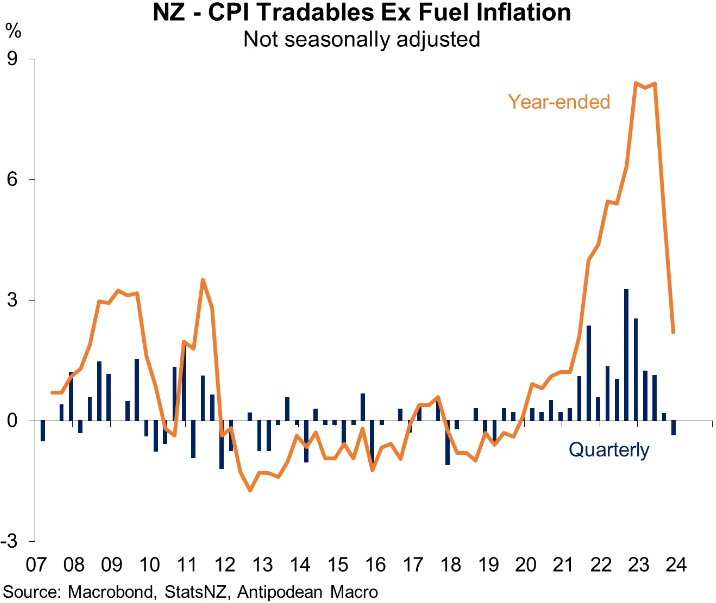

This lower than forecast inflation has been driven by falling import prices (i.e. tradables inflation). Much of these falls relate to volatile items like food and motor vehicles, which the Reserve Bank tends to look through when setting monetary policy:

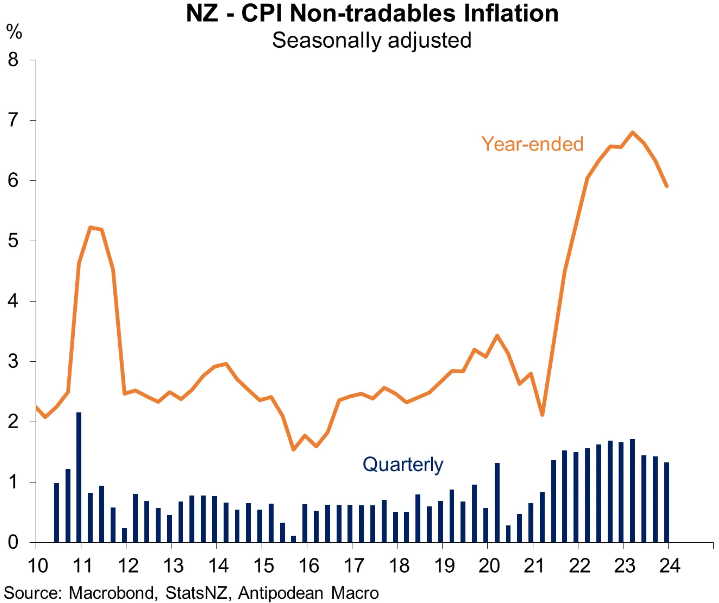

Indeed, according to Justin Fabo, “non-tradables inflation in New Zealand in Q4 was a bit above the RBNZ’s expectation (+1.1% q/q vs +0.9% q/q). On a seasonally adjusted basis, non-tradables inflation edged slightly lower to +1.3% q/q”:

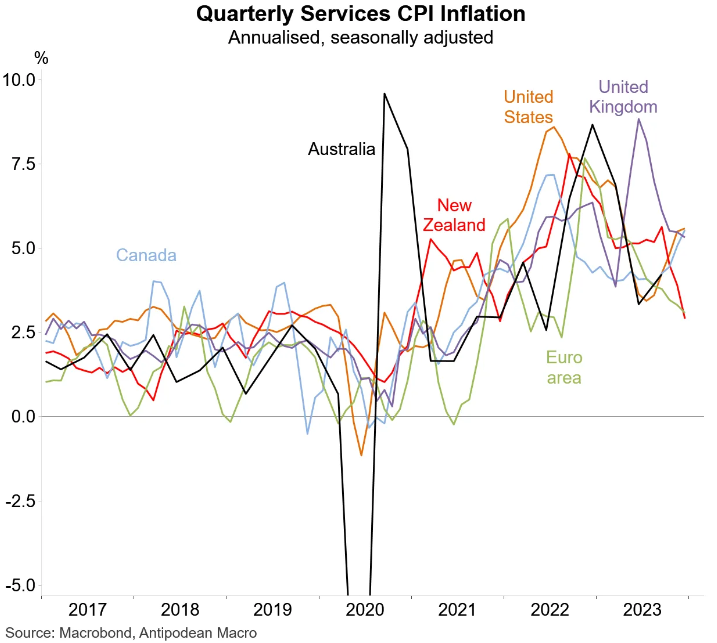

That said, New Zealand services inflation has fallen faster than most other nations:

Westpac believes the CPI print will keep the Reserve Bank of New Zealand on hold through 2024 because inflation is “still uncomfortably high”:

“The easing in underlying inflation pressures will be welcome news for the RBNZ. However, digging under the surface, it’s clear that the RBNZ can’t take its foot off the brake just yet”.

“The easing in underlying inflation is mainly due to falls in the retail prices of imported goods. Domestic inflation pressures, which are a bigger focus for the RBNZ, are still running hot”.

“This CPI is showing some encouraging progress towards the RBNZ’s 1-3% target range, but the strength of non-tradables and other core inflation indicators remains”.

“The lower than RBNZ forecast headline outcome will likely make the RBNZ comfortable that inflation expectations will remain in check”.

“But ongoing sticky core inflation will likely be viewed with caution by the RBNZ and emphasises that there is still work to do before they can be sure that inflation reaches 2% in the second half of 2025 as is required by their new more focused mandate”.

“We remain comfortable with our view that 2024 will be a year of an unchanged OCR. More indications of declining core inflation will likely be required before an adjustment lower in the OCR occurs”.