Immediately after the release of the Q4 CPI inflation data by the Australian Bureau of Statistics (ABS), I ran through the results with Bill McDonald on 4BC Mornings:

In the extended interview, I explained why the result means the RBA is “certain” to keep the official cash rate on hold at next week’s Monetary Policy Meeting, with rate cuts to follow later in the year.

My view is shared by CBA’s economics team, which tips “rate cuts to come in 2024”.

Below is CBA’s analysis.

Key Points:

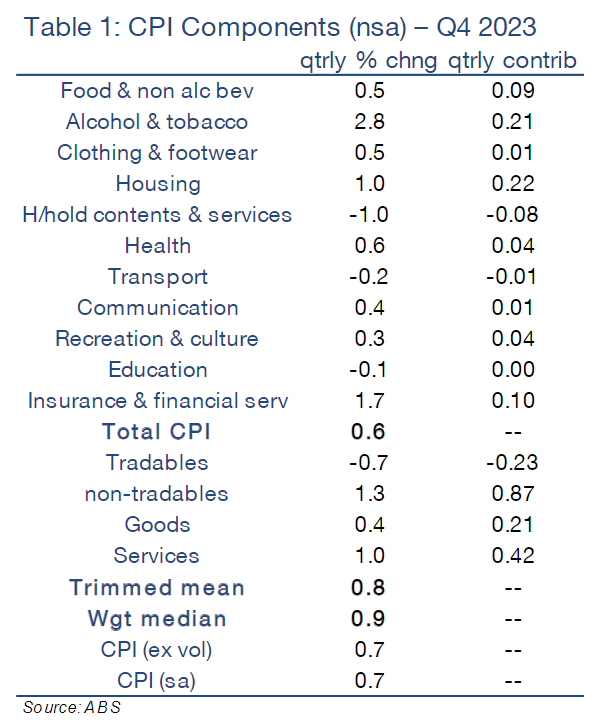

- The headline CPI rose by 0.6%/qtr in Q4 23and the annual rate dropped to 4.1%.

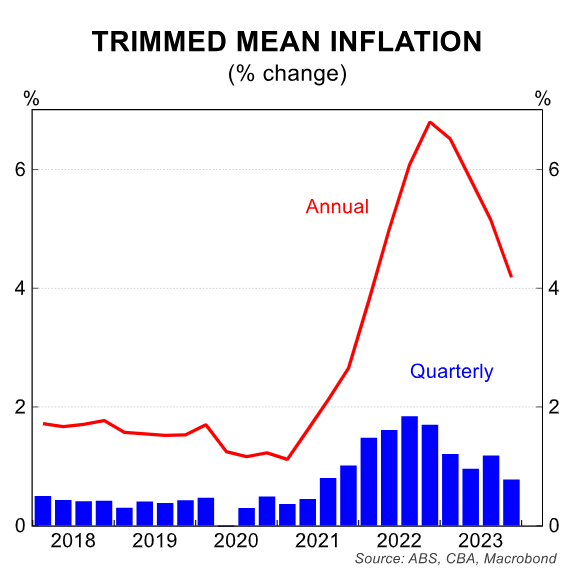

- The trimmed mean CPI increased by 0.8%/qtr and the annual rate stepped down to 4.2%.

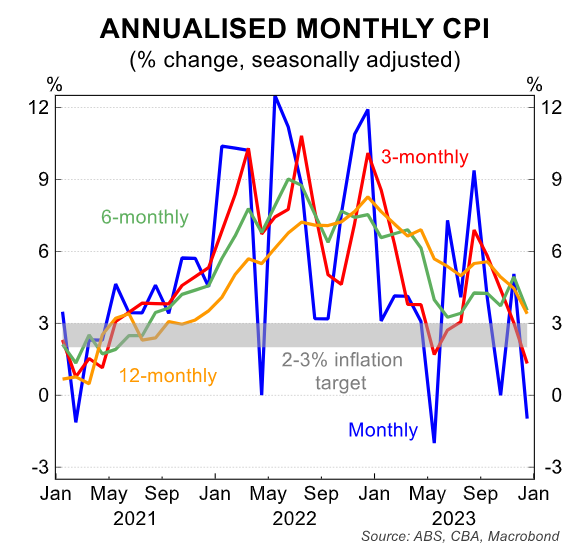

- Inflation as measured by the monthly CPI indicator dipped to 3.4%.

- The RBA will leave the cash rate on hold at the February Board meeting in what should be a straight forward decision.

- We continue to expect an easing cycle commencing in September (we have 75bp of rate cuts in our profile in late 2024 and a further 75bp of easing in H1 25, which would take the cash rate to 2.85%).

Inflation prints materially below the RBA’s forecasts:

The December quarter CPI was below market expectations on both the headline and underlying measures.

Importantly for the outlook for monetary policy, it was materially below the RBA’s forecasts.

Headline CPI rose by 0.6%/qtr in Q4 23–below the 0.8%/qtr market median forecast (CBA in line with consensus).

The annual rate dropped from 5.4% to 4.1%. For context the RBA forecast Q4 23 CPI to be 4.5% (0.4ppts higher than today’s outcome of 4.1%).

The trimmed mean CPI rose by 0.8%/qtr – just under the 0.9%/qtr market median forecast (CBA in line with consensus). The annual rate fell from a revised 5.1% to 4.2%. Again for context, the RBA forecast the Q4 23 trimmed mean CPI to be 4.5% (0.3ppts higher than today’s outcome).

The miss for us was on housing (smaller rises in utilities), financial services and groceries. We noted that the risk to our forecast sat with a weaker outcome.

Today’s data will be viewed favourably by policymakers. The fall in the rate of inflation over the past year has been swift. CPI inflation peaked at 7.8%/yr in Q4 22 (i.e. the annual rate of inflation has declined by 378bps over the past year).

The job of returning inflation to the 2-3% target band is not yet done. But the RBA is now on the home straight.

Our central bank will take comfort that the disinflation trend observed in other jurisdictions is at work in Australia. Indeed, there has been a downward trend in the quarterly change in core inflation over the past year.

The September quarter was the anomaly last year. But context is important. The lift in underlying inflation in Q3 23 was due to the big increase in the minimum and award wage.

Many firms increased consumer prices in Q3 23 to recoup some of the increase in labour costs imposed on them because of the large increase in award wages.

But that was essentially a ‘one-off’ bump in the trend decline in inflation. Wednesday’s data is confirmation of that.

The key components:

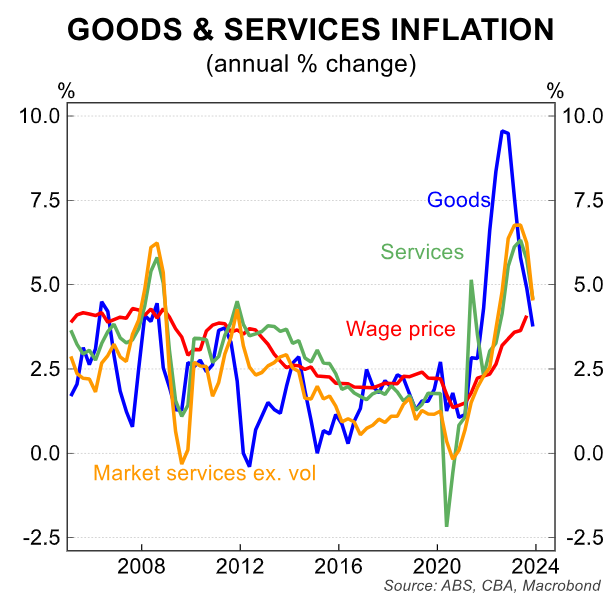

Goods disinflation continued to drive overall inflation lower. Goods inflation rose by 0.5% in Q4 23 and the annual rate eased to 3.8% (from 4.9%).

Services inflation rose by a stronger 1.0%/qtr and the annual rate dipped to 4.6% (from 5.8%). Services inflation is the key area of concern for the RBA given it has historically been stickier than goods inflation.

But we don’t think services inflation will be a problem as we move through 2024. The ongoing loosening in the labour market will put downward pressure on wages growth. In turn, this lowers growth in input costs in the services sector, which dampens cost-push inflation.

Context is also important. The pandemic resulted in a massive disruption to services trade. Many businesses in the services sector were unable to adjust their prices upwards in 2020 and 2021 so there has been some catch-up in prices growth at play.

Here we note that services inflation rose by 12.9% over the three years to Q4 23. Over the same period goods inflation rose by a larger 18.5%.

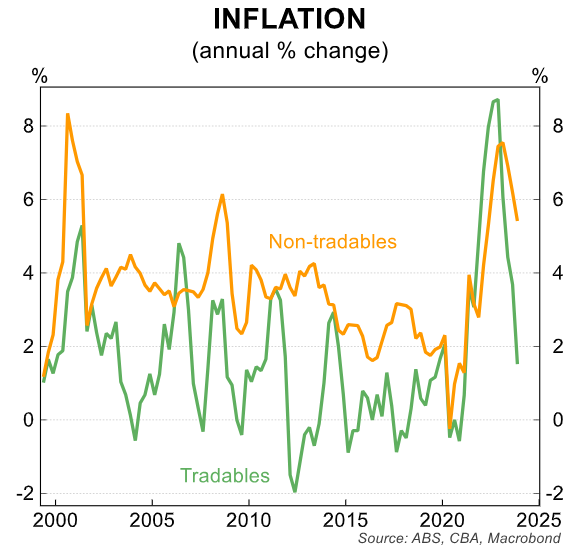

Non-tradables inflation (1.3%/qtr and 5.4%/yr) accelerated by more than tradables (domestic inflation) in the December quarter.

The lift in non-tradables inflation was primarily due to price rises for new dwellings, rents, insurance and electricity.

Tradables prices fell by 0.7%/qtr and the annual rate dropped to 1.5%.

Price falls (i.e. deflation) over the year were observed in clothing, footwear, furniture and household appliances.

Implications for monetary policy:

Monetary policy works with the well documented long and variable lags. The RBA’s highly aggressive tightening cycle had very little impact on price changes in the economy in 2022.

But rate hikes worked to slow demand growth in the economy in 2023 and by extension price rises. That process will continue through 2024.

We retain our view that the RBA will leave the cash rate on hold at the upcoming February Board meeting (6/2). Indeed, the decision next week to leave policy on hold will be straight forward given the inflation data today has come in weaker than the RBA anticipated.

Monetary policy is restrictive and the arguments in favour of any further tightening are weak. We firmly believe the next move in the cash rate is down.

On that score, today’s data gives us higher conviction in our call for an easing cycle to commence in Q3 24 (we have September pencilled in for the first rate cut and look for 150bps of easing by mid-2025).

The RBA will publish updated forecasts next week in the February Statement on Monetary Policy (SMP). We expect the RBA will downwardly revise their inflation forecasts.

The Q4 23 outcome means mechanically the RBA will need to lower their inflation profile over 2024. But the RBA may go one step further and make an additional small downward adjustment to their inflation profile given the recent trends in household expenditure and the labour market.

We will publish our full RBA preview on Friday 2 February…

The monthly CPI indicator in December:

It’s worth also taking stock of the December read of the monthly CPI indicator.

Annual inflation as measured by the CPI indicator fell to 3.4%/yr. That is just 0.4ppts from the top of the RBA’s inflation target.

The seasonally adjusted monthly change was a decline of 0.1%.

The monthly and three-monthly annualised inflation rates are below RBA’s inflation target band, as the below chart shows.