A new year but an old story:

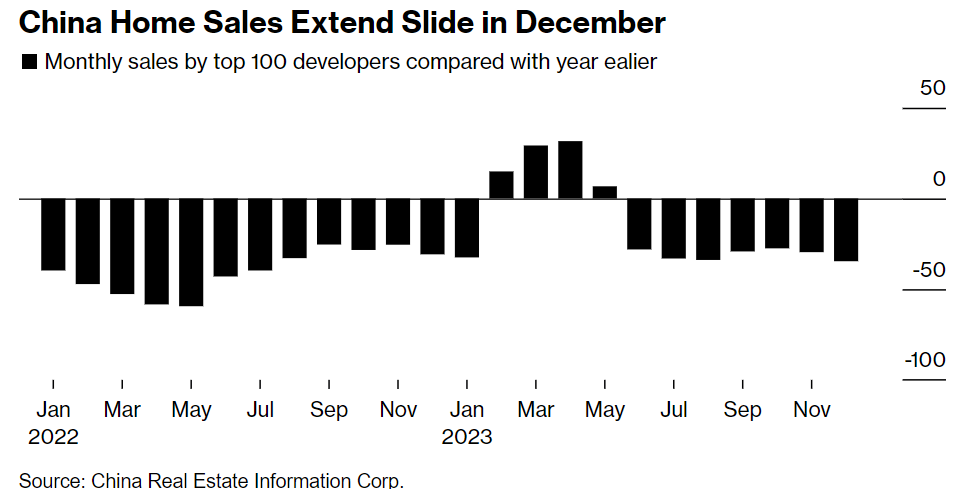

The slide in China’s home sales accelerated in December, underscoring the challenges to arrest the country’s property slump.

The value of new home sales among the 100 biggest real estate companies fell 34.6% from a year earlier to 451.3 billion yuan ($64 billion), compared with a 29.6% decline in November, according to preliminary data from China Real Estate Information Corp. on Sunday.

That puts major developers’ full-year sales 16.5% lower than 2022, worse than the institution’s earlier estimate of a 15% drop. December’s sales were up 15.7% compared with the previous month.

Rising December sales are seasonal.

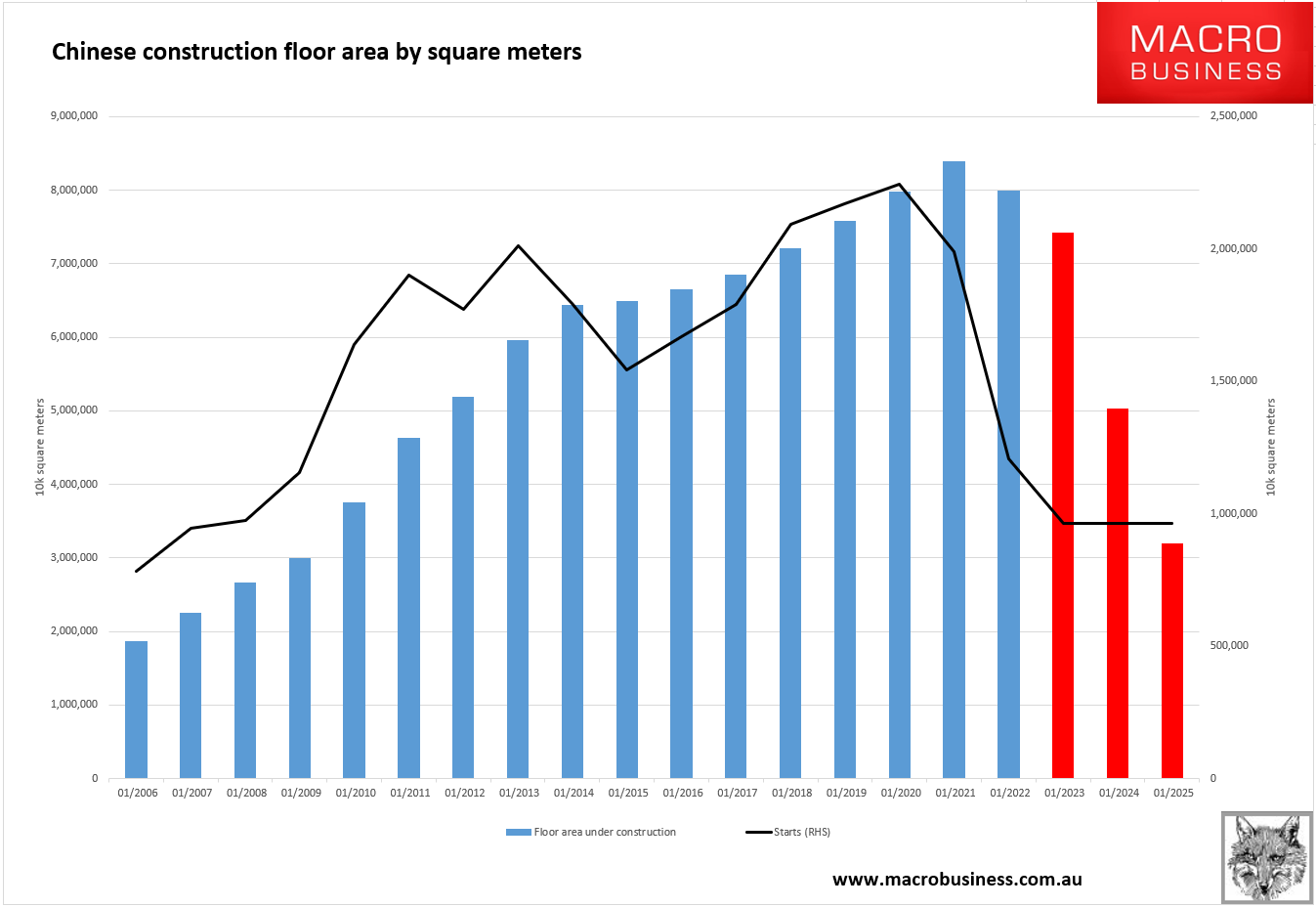

There is no end in sight for this and, eventually, the volume of construction work will catch down to falling sales and starts:

There is still doubt about how swiftly stock catches down to flow given public support for completions, but it will come sooner or later.

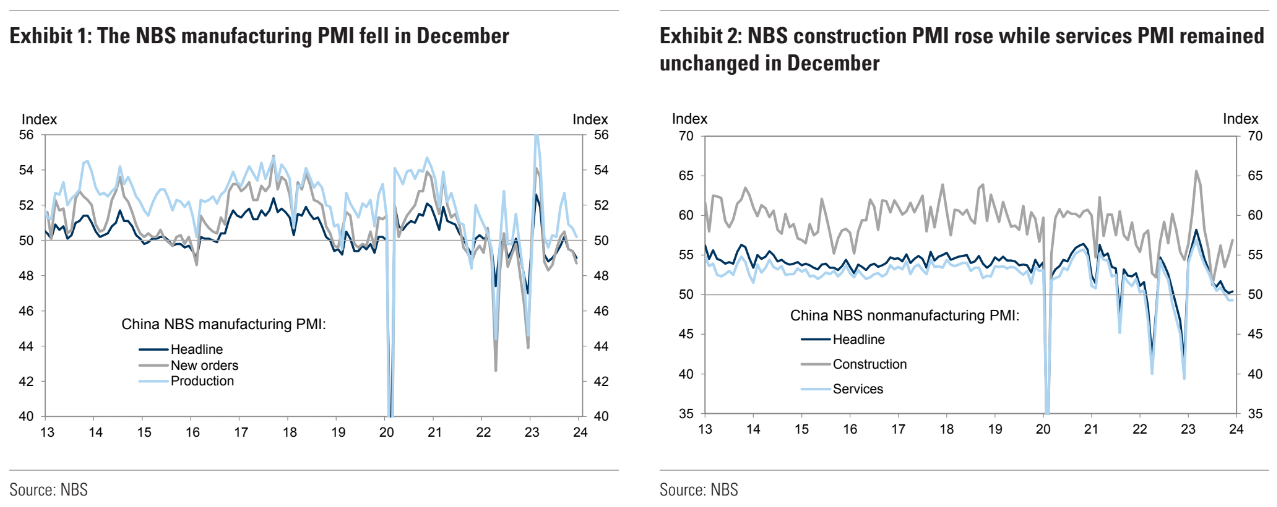

The drag on activity is still evident in the PMIs. Goldman:

The China NBS purchasing managers’ indexes (PMIs) survey showed worse-than-expected manufacturing and slightly improved non-manufacturing activity in December.

The NBS manufacturing PMI headline index fell to 49.0 in December from 49.4 in November.

Among the five major sub-indexes, the output and new orders sub-indexes declined to 50.2 and 48.7 from 50.7 and 49.4 in November, respectively.

The employment sub-index edged down to 47.9 from 48.1 in November.

The NBS commented that the decline in manufacturing PMI was linked to some raw materials industries entering the off-season period and also noted that decreasing overseas orders and insufficient domestic demand are the main challenges faced by some surveyed enterprises.

On the trade-related sub-indexes in the manufacturing survey, the new export orders sub-index further decreased to 45.8 in December (vs. 46.3 in November), pointing to still soft external demand.

The import sub-index decreased to 46.4 in December (vs. 47.3 in November). The raw material inventories sub-index declined to 47.7 from 48.0, and the finished goods inventories sub-index fell to 47.8 from 48.2.

By enterprise size, the PMIs of large, medium and small enterprises decreased to 50.0, 48.7 and 47.3 in December from 50.5, 48.8 and 47.8 in November.

Price indicators in the NBS manufacturing survey were mixed in December.

The input cost sub-indexrose to 51.5 (vs. 50.7 in November), while the output prices sub-index decreased to 47.7 (vs. 48.2 in November).

The official non-manufacturing PMI (comprised of the services and construction sectors) rose to 50.4 in December (vs. 50.2 in November).

The services PMI remained unchanged at 49.3 in December.

According to the survey, the PMIs of service industries such as postal, telecommunication and satellite transmission were above 55 while the PMIs of water transport, airline and hotel services were below 46, partly on adverse weather conditions.

The construction PMI increased to 56.9 in December from 55.0 in November, with the NBS mentioning that some enterprises increased the speed of infrastructure project construction ahead of the Chinese New Year holiday.

The construction PMI is weak in context. It seldom contracts!

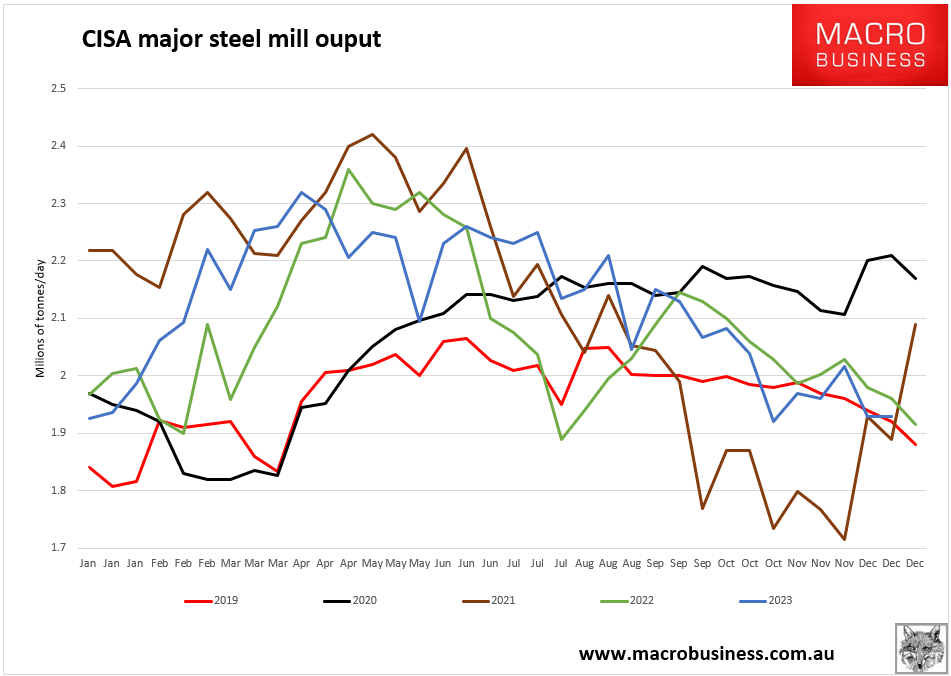

Additionally, last year’s 23mt surge in Chinese steel exports largely replaced crashed Ukrainian shipments.

For Chinese steel exports to keep rising this year, they must compete on price. The year closed out on weak production volumes:

With iron ore above $140 super cycle pricing, the risk is asymmetric to the downside despite low inventories in China.

I am short into the quarter end and EOFY.