The past several years have been a distressing experience for Australia’s growing army of renters, especially those on lower incomes.

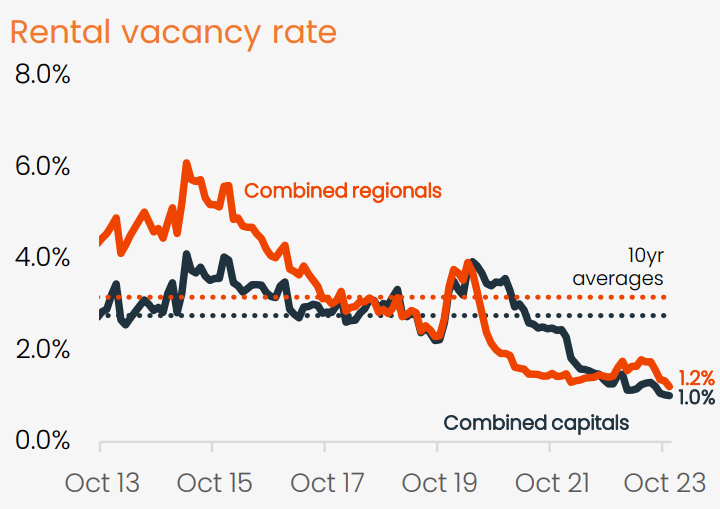

The massive imbalance between demand and supply has driven the nation’s rental vacancy rate to historical lows:

Source: CoreLogic

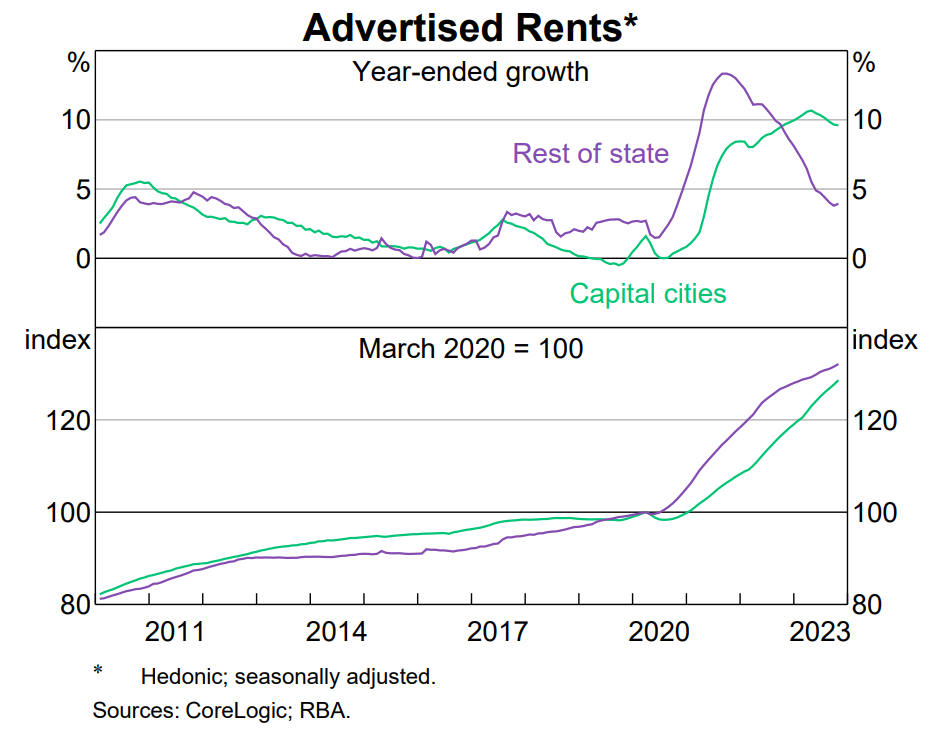

And this has caused advertised rents to soar across the country:

Most analysts expect rents to continue growing much faster than incomes in 2024. However, rents should grow at a slower pace than last year reflecting affordability constraints and more people moving into share housing.

Finder’s head of consumer research Graham Cooke, told News.com.au that “Finder’s Consumer Sentiment Tracker shows 42% of renters are currently struggling to pay their rent, which is higher than the 37% of mortgage holders in the same position”.

“Much of the conversation around rate rises focuses on homeowners, but it’s actually renters who are proportionally feeling the impact more, as they deal with flow-on rent increases”.

“Further rent increases won’t be welcome news for those struggling”.

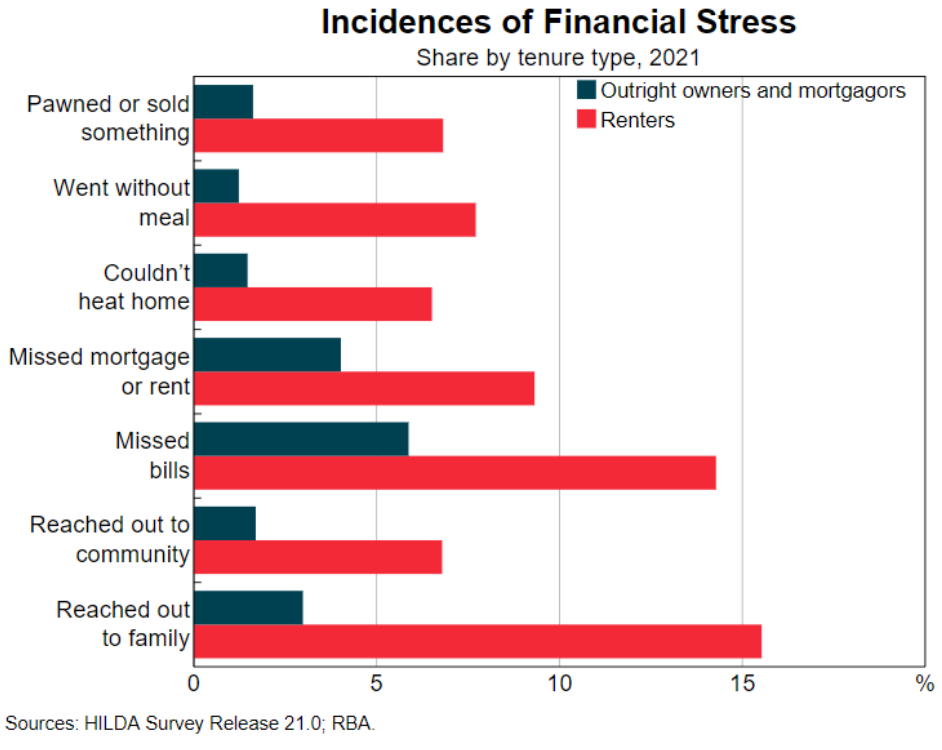

Finder’s results are matched by the Reserve Bank of Australia’s (RBA) latest Financial Stability Review, which showed that financial stress is more likely to occur and is more frequent for renters than for owner-occupier households:

This outcome makes sense.

Renting households have lower wages and significantly smaller savings than mortgage-holding households.

Roy Morgan’s 2023 Wealth Report also showed that renters have fallen substantially behind homeowners.

According to this research, Australia’s wealth increased by 7.0% between March 2020 (pre-COVID) and March 2023.

This increase in wealth was mostly driven by a 43.2% increase in the value of owner-occupied dwellings, which increased in value from $4.16 trillion to $5.95 trillion.

Indeed, 95.4% of Australia’s net wealth was held by half of the population, primarily homeowners.

The bottom half of the population, primarily renters, had its wealth share increase as well, but only from 3.6% to 4.6%.

So basically, renters tend to be poorer and have lower wages.

As a result, rising rents have a greater impact on them than growing mortgage payments have on homeowners.

The vast majority of homeowners may also sell their homes and walk away with large capital gains, whereas renters cannot.

Finally, mortgage holders will benefit whenever the RBA starts decreasing interest rates. Rents, on the other hand, almost never decline.