CBA economist, Stephen Wu, has published the bank’s Q4 CPI preview (below), which is “slightly skewed to the downside”.

Wu believes “an outcome in line with or below our forecast is consistent with monetary policy on hold in February (our base case)”.

MB’s view is that rates will remain on hold until late in the year when the RBA will commence an easing cycle.

Overview

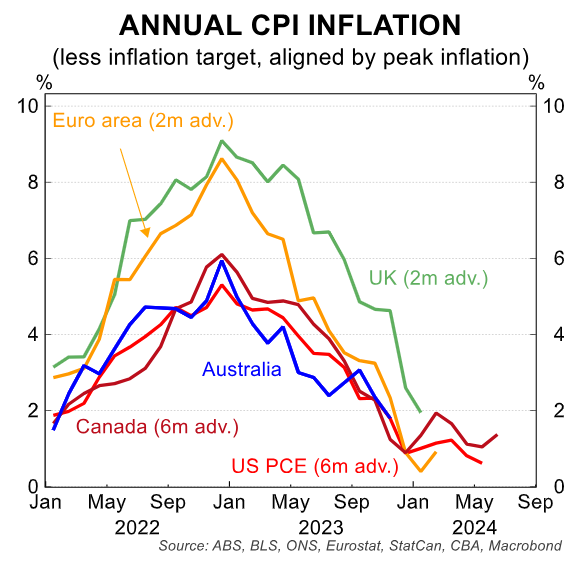

Inflation has come down swiftly across the advanced economies, including in Australia. At its peak, inflation was between 6-8ppts above central banks’ targets. Now, inflation is less than 2ppts above central banks’ inflation targets.

The Q4 23 CPI in Australia, due out next Wednesday (31/1), should show further progress on disinflation. The RBA will take stock of the figures when they update their economic forecasts ahead of the February monetary policy meeting (5-6/2).

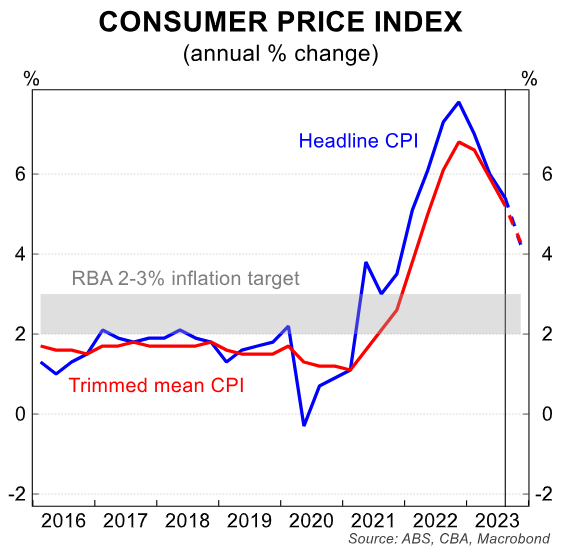

We forecast Q4 23 CPI rose by 0.8%/qtr. The easing in the quarterly pace will see the annual rate dip to 4.2%, the lowest since Q4 21.

Our quarterly estimate is consistent with a 3-handle on inflation in the December monthly CPI indicator (released at the same time as the Q4 23 data). This is something we have flagged since late last year and we pencil in a 3.9%/yr print.

The more policy-relevant trimmed mean CPI we estimate rose by 0.9%/qtr to take the annual rate to 4.3%. Such an outcome would be a 0.9ppt decline from the Q3 23 annual rate and 0.2ppt lower than the RBA’s forecasts from late 2023.

The RBA forecasts both trimmed mean inflation and headline CPI inflation of 4.5%/yr. We note that these forecasts will not have embedded the weaker-than-expected CPI indicator in both October and November.

The ABS’ new monthly CPI indicator has provided a strong signal that inflation moderated in October and November. But, price movements are very seasonal in December, and particularly so since the pandemic.

We anticipate strong seasonal lifts in parts of the CPI basket (but not as strong as in Q4 22). However, we view the risks to our baseline inflation forecast as slightly skewed to the downside.

In particular, the very volatile holiday travel & accommodation prices may not have increased in December by as much as we expect.

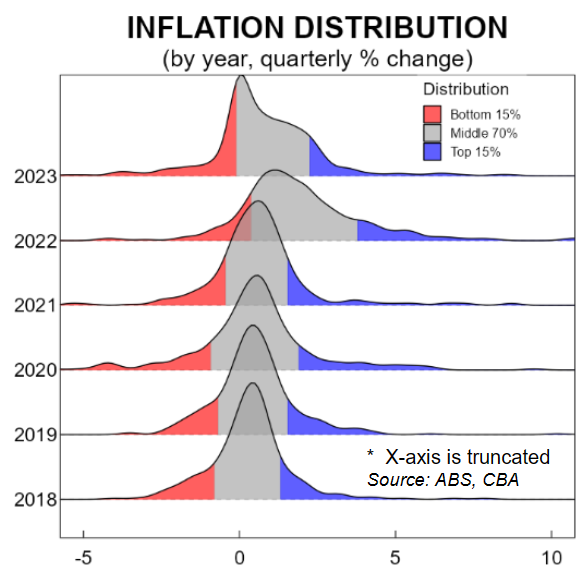

Nevertheless, the breadth of inflationary pressures was subsiding over 2023, as the below chart shows.

The right tail of the distribution of price changes has noticeably improved; that is, the parts of the CPI basket experiencing elevated inflation has declined to levels that are more normal.

Indeed, we expect further disinflation this year. For more details, please see here for our latest piece summarising CBA’s outlook for the economy and the RBA, published by our Head of Australian Economics Gareth Aird earlier this week.

The upshot is that we expect the inflation data to marry up with clear signs of softening demand in the economy, most notably from the household sector. That should see the RBA on hold next month. And it supports our call for an easing cycle to commence in September.

The detail of our Q3 23 CPI call

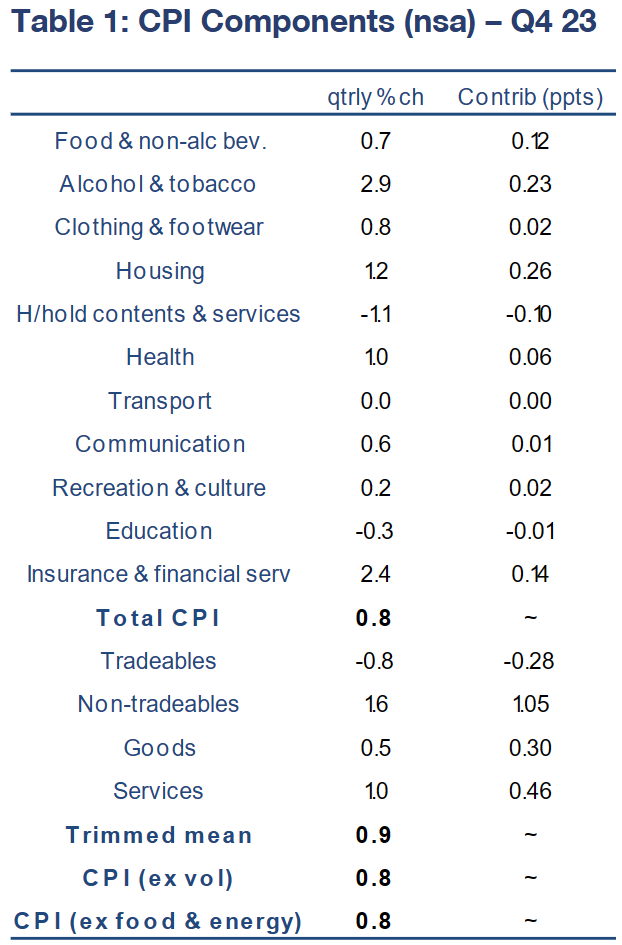

See table 1 below for our detailed forecasts for the Q423 CPI.

Overall, our bottom-up estimates imply headline CPI rose by 0.8%/qtr (4.2%/yr) and the trimmed mean CPI increased by 0.9%/qtr(4.3%/yr).

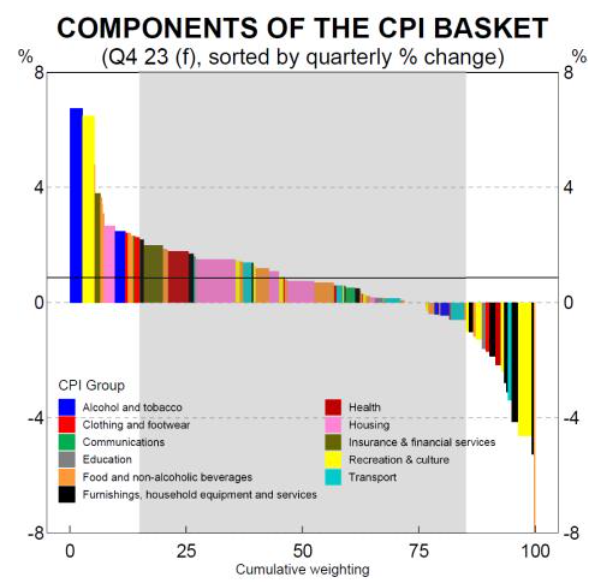

The large expected increases in tobacco, insurance, domestic holiday travel, and electricity will be excluded from the trimmed mean calculation. And many of the outright price declines in household goods, meats, and international travel will be among the bottom 15% of CPI items and be trimmed out (see below chart).

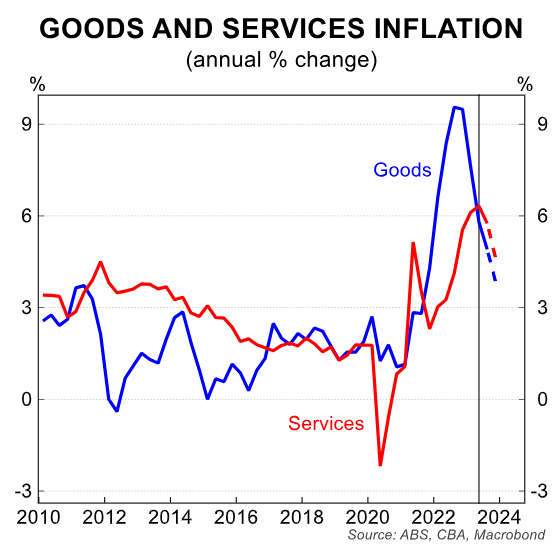

We estimate services inflation remained elevated, at 1.0%/qtr, driving the increase in prices in the quarter. Base effects would mean the annual rate dips to 4.6%.

Goods disinflation also continued, with our estimate of the annual rate at 3.9% by Q4 23.

Inflation remains front of mind for the RBA, and is the single most important data ahead of the February Board meeting.

The RBA will be encouraged by the last two monthly CPI indicator prints. But the quarterly CPI remains the benchmark inflation report.

An outcome next Wednesday in line with or below our forecasts would be consistent with an unchanged cash rate in February.

We note that December retail trade (30/1) also has the potential to shift the balance of risks, particularly as the RBA has consistently flagged weaker-than-expected household consumption as a key risk to the outlook.

Gareth will publish a full preview of the upcoming Board meeting on Friday 2 February.