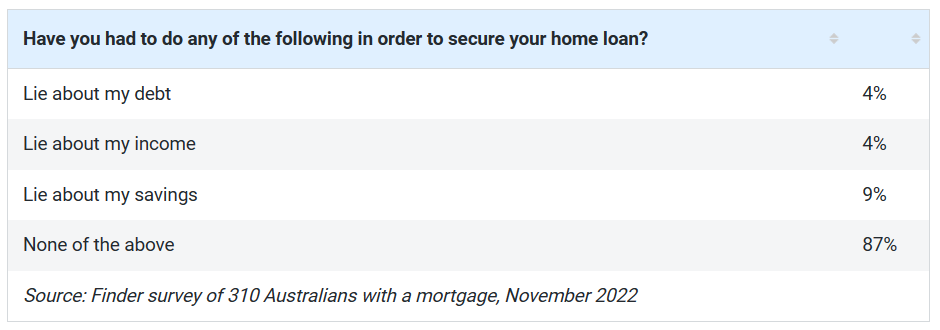

Earlier this year, Finder released a survey which revealed that at least one in every eight respondents admitted they had lied on their home loan application forms.

If the findings of the survey applied to the entire population, it would indicate that an estimated 430,000 mortgage holders fabricated data concerning their home loan applications.

Roughly one in twenty mortgage applicants who confessed to falsifying their applications provided false information regarding their income or debt load.

Richard Whitten, an expert on home loans at Finder, cautioned that these “liar loans” heighten the likelihood that a mortgage holder will experience financial strain.

“While the lies might go unnoticed – the financial burden of an unaffordable loan could create a lot of stress”, he said.

“Legality aside, you’re putting yourself in a risky position if you lie on your application and borrow more than you can afford”.

Whitten also believed it increased the chances that if a borrower fell behind in their repayments, they could lose their homes.

“While small inaccuracies may not be the end of the world, if a lender finds a big discrepancy in the figures you’ve given them or you’ve outright lied about your financial position, the consequences could be severe”, he said.

“Home loan contracts typically contain wording around providing misleading or incorrect information to a lender”.

“In the worst case, lying on a mortgage application is grounds for a default event, meaning the lender could sell your property”.

This week, The ABC reported that liar mortgages have been back in vogue since the RBA began hiking interest rates last year:

Sean Quagliani, the co-founder of financial technology company Fortiro, which big banks and other lenders use to help them detect fraudulent documents, says since interest rates started rising about a year and a half ago, there has been a threefold increase in people lying on home loan applications.

“One example might be, somebody will modify a pay slip to increase the amount of income that they’ve got,” Mr Quagliani says.

“We see other examples of people removing transactions from their bank statements to only show that they might have no kids, but they have kids. People can be very creative.”

Sean Quagliani, the co-founder of financial technology company Fortiro, which big banks and other lenders use to help them detect fraudulent documents, says since interest rates started rising about a year and a half ago, there has been a threefold increase in people lying on home loan applications.

“One example might be, somebody will modify a pay slip to increase the amount of income that they’ve got,” Mr Quagliani says.

“We see other examples of people removing transactions from their bank statements to only show that they might have no kids, but they have kids. People can be very creative”…

Another reason for the threefold increase in “liar loans”, Mr Quagliani says, is that there’s more opportunity to fabricate documents due to the plethora of free tools available online.

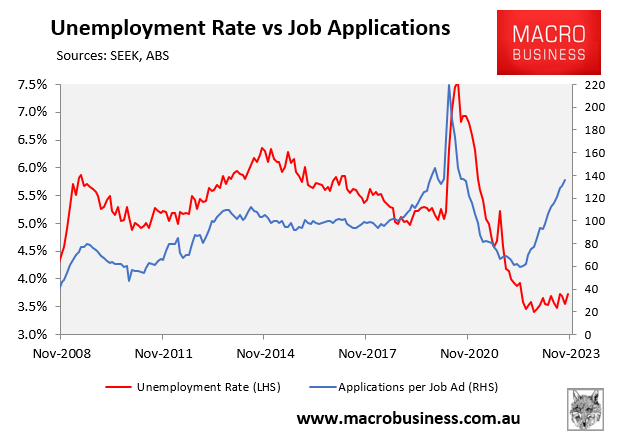

The biggest factor that will determine whether mortgage borrowers get into trouble is the strength of the labour market.

If mortgage holders keep their jobs, most will weather the interest rate hikes okay.

But if unemployment spikes, then the number of housing defaults will rise accordingly.

Unemployment is expected to soar next year, which could place hundreds of thousands of borrowers into severe financial strain:

Thus, next year could see a large volume of mortgage defaults, with highly leveraged ‘liar’ mortgage holders particularly vulnerable.