Summary:

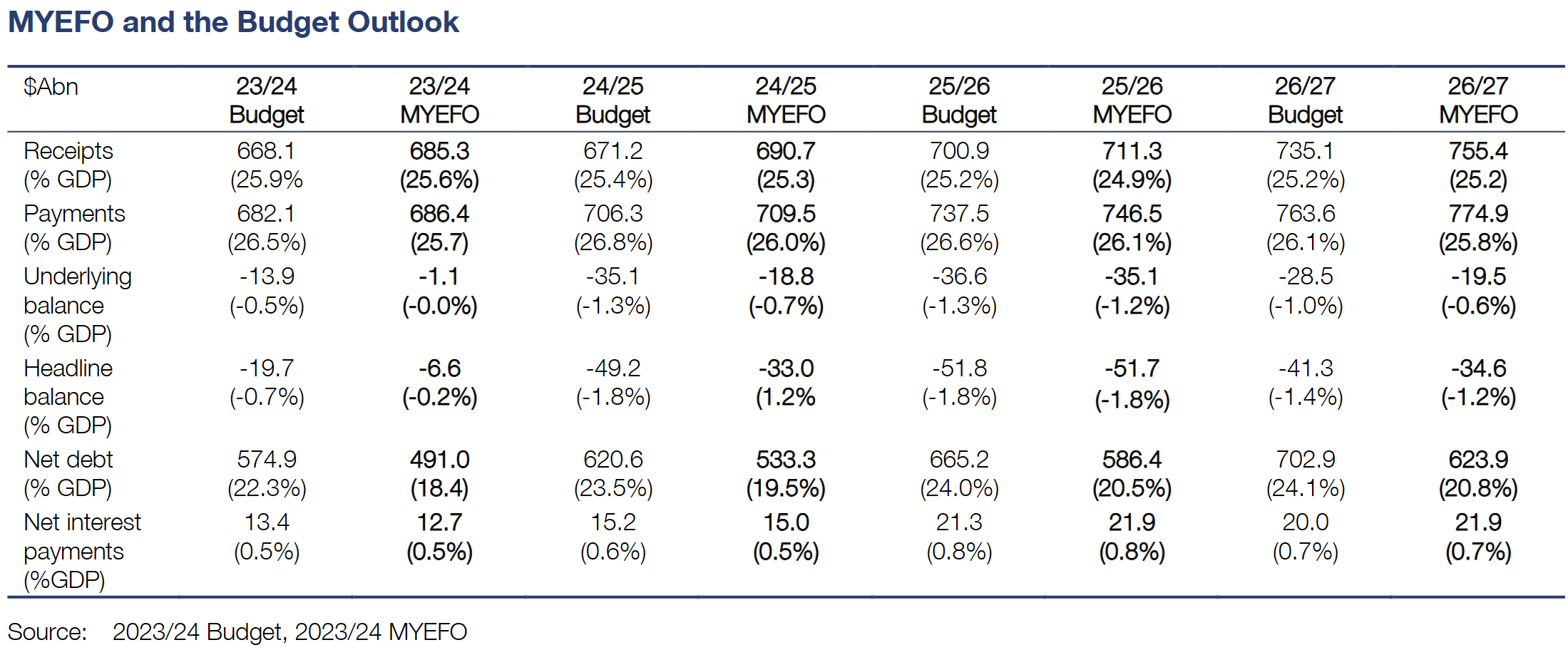

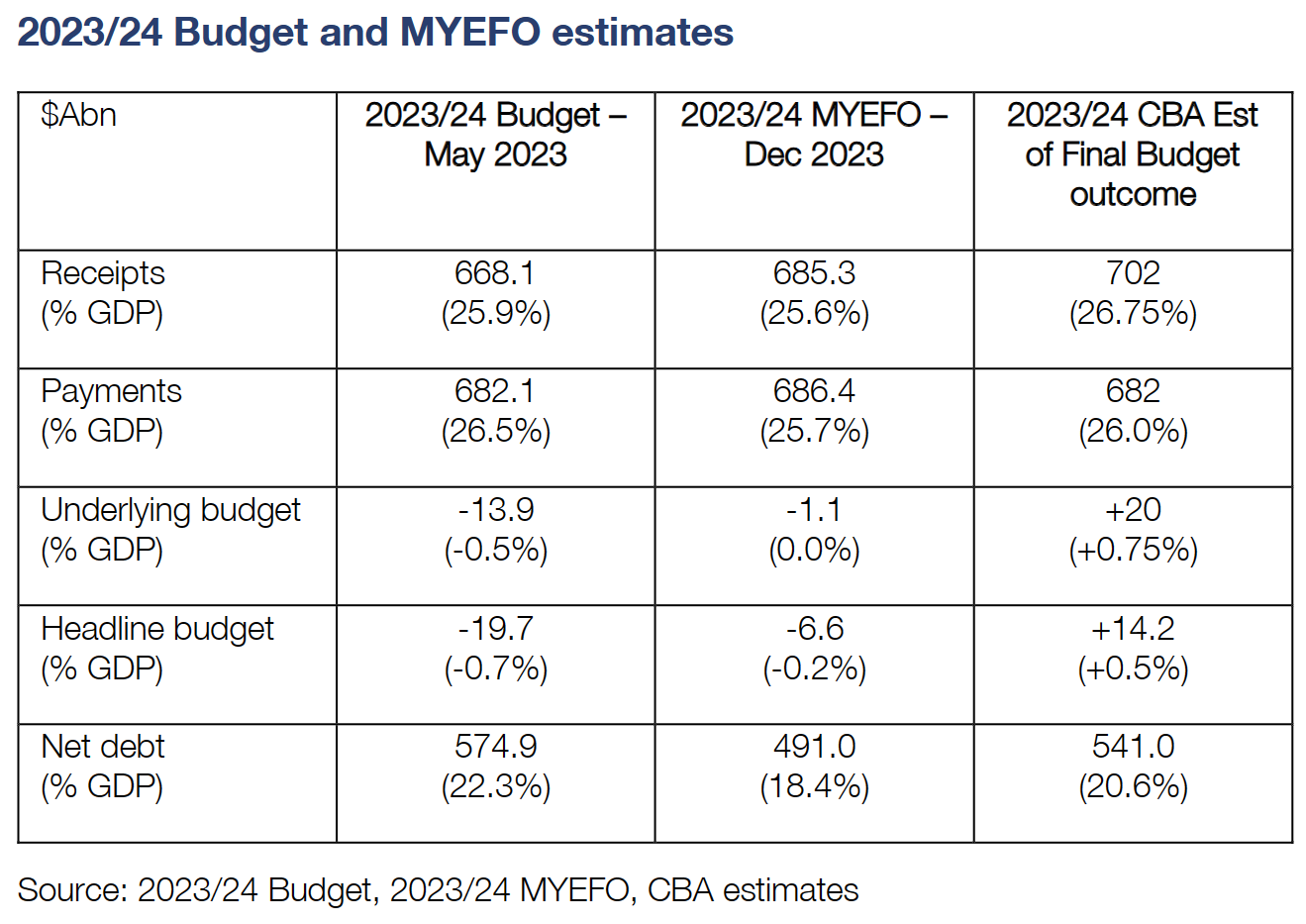

The 2023/24 Budget is now estimated to be in deficit by $A1.11bn (0% of GDP), compared to the estimate back at the time of the May Budget of $A13.92bn (-0.5% of GDP).

However, we stand by our view that the final budget outcome is likely to be better than the MYEFO estimate, with a surplus of ~$A20bn (0.75% of GDP) likely.

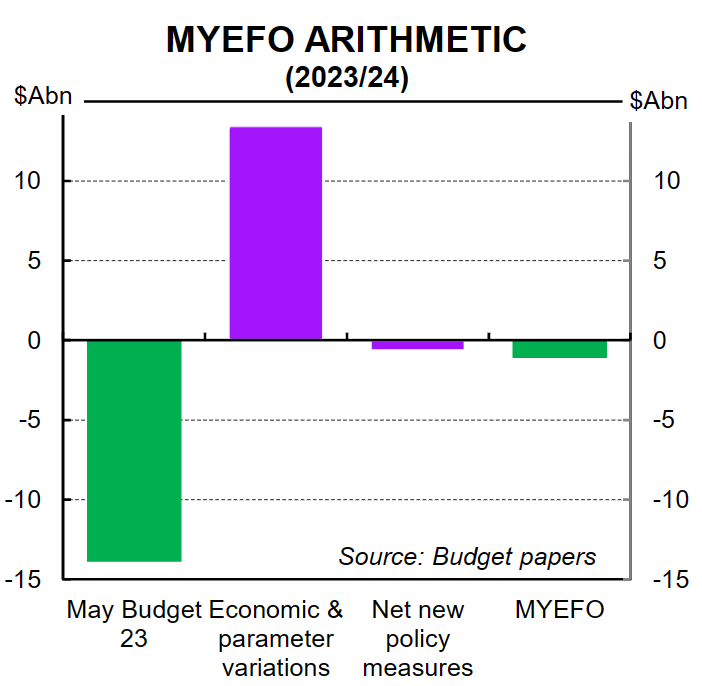

The improvement in the budget has flowed from a large lift in government revenue, from a stronger-than-expected economy and commodity prices that have generally been allowed to flow through to the budget bottom line.

For 2023/24, $A13.5bn of the improvement has been driven by parameter changes, while only $A0.65bn of policy changes has occurred.

There has been a shift lower in the budget deficit profile from 2024/25 through 2026/27. Much of the improvement is coming through in 2024/25 and 2026/27.

The lower deficit profile means that net debt is now expected to rise to $A623.9bn (20.8% of GDP) as at June 2027, lower than the previous forecast of $A702.9bn (24.1% of GDP) from the May budget.

Key policy announcements contained in the MYEFO centre on additional funding for new housing and critical minerals projects. Additional funds for current infrastructure projects has also been delivered, as well as funding for the health sector and the NDIS.

The economic forecasts look broadly ok, there have been little change to the forecasts for GDP growth –although the sources of growth have shifted a little. Population growth forecasts have been revised up in the near term and CPI forecasts have also been nudged higher.

With the 2023/24 budget surplus expected to be little changed from the 2022/23 final budget outcome, we expect fiscal policy to be a neutral for the monetary policy outlook in the year ahead.

MYEFO shows improved budget bottom-line –but final outcome should be better:

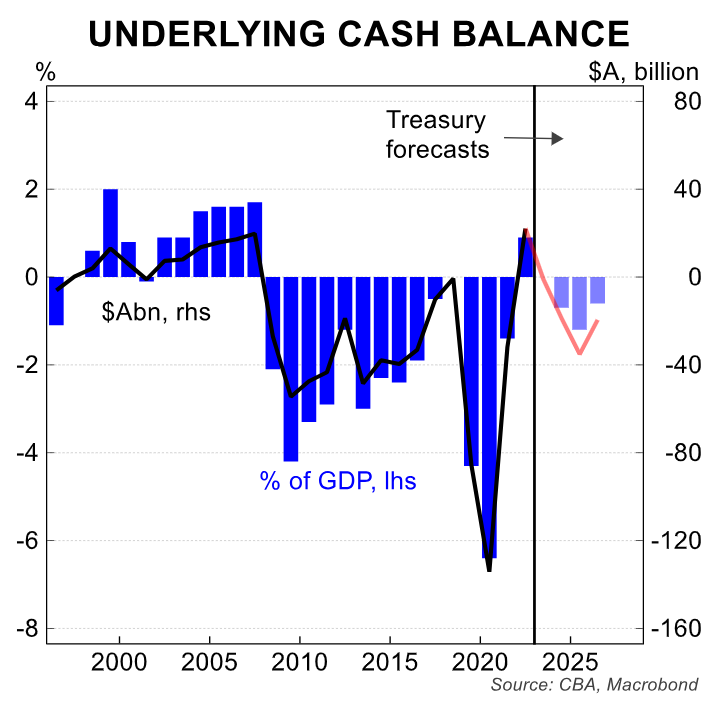

The Mid-Year Economic and Fiscal Outlook (MYEFO) released Wednesday shows an improved budget bottom line for 2023/24, with the original estimate of a -$A13.9bn deficit (-0.5% of GDP) now an estimated at a deficit of just -$A1.1bn (0% of GDP).

However, as detailed in our MYEFO preview, we continue to expect that a surplus of ~$A20bn (0.75% of GDP) will be achieved once the final budget outcome is received in the second half of 2024-provided there are no significant new policies announced.

The improvement in 2023/24 is flowing mostly from the better performing economy, with parameter changes accounting for $A13.5bn of the improvement, while policy changes weakened the underlying cash balance byjust$A0.65bn.

The government notes it is returning 92% of all tax upgrades in the MYEFO to the budget bottom line.

The improvements in the underlying deficit have also flowed through to the three years after 2023/24. Over the course of the four year budget profile, the sum of the deficits have been reduced by $A39.5bn.

Parameter changes, largely due to changes in economic assumptions, have reduced the deficit profile by$A44.8bn, while policy changes have added $A5.3bn, largely due to higher expenses.

Receipts from policy changes only add an extra $A1.2bn to the bottom line.

However, while the overall profile of the deficits have shifted lower, deficits are still increasing over time, reaching $A35.1bn (1.2% of GDP) in 2025/26, before starting to improve to $A19.5bn (0.6%) of GDP in 2026/27.

Revenue for 2023/24 is $A17.2bn higher than expected as at the May budget, improvements have also occurred out to 2026/27.

Most of the revenue improvement in 2023/24 has occurred in tax receipts ($A16.4bn). In total, tax receipts have been revised up by $A64.4bn over the four years to 2026/27. Most of the upgrade has been driven by company tax due to persistent strength in commodity export prices and also higher non-mining corporate profits.

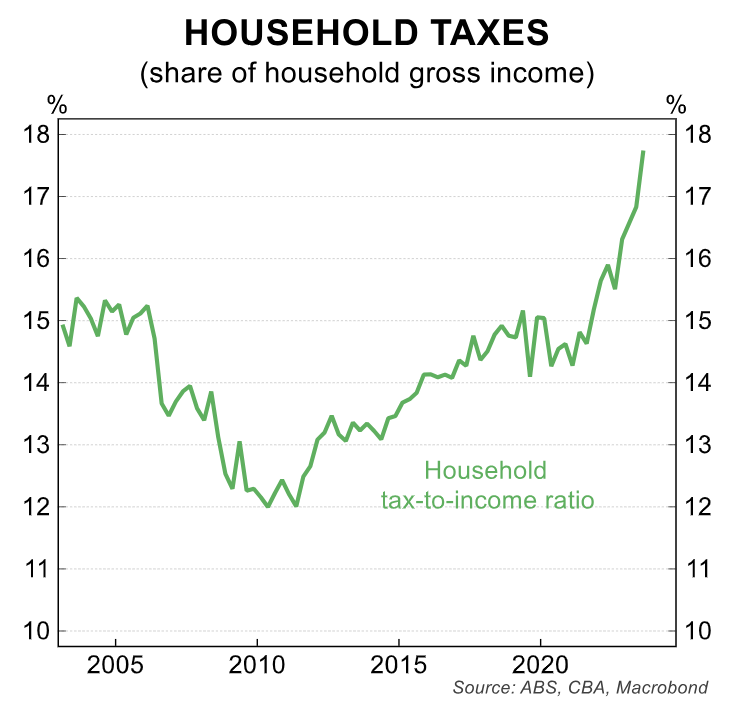

There has also been a lift in personal income tax collection due to stronger employment growth. As the Q3 23 National Accounts illustrated, the household tax to income ratio is at a record high.

More households are paying more income tax. This is helping monetary policy through removing cash from the household sector.

On the payments side, there has been only minimal changes in 2023/24. Payments are $A4.3bn higher in 2023/24.

The largest shifts in payments have occurred in 2025/26 and 2026/2, but as we note earlier the overall deficit profile has shifted smaller over the next four years.

However while there has only been minimal payment shifts, the size of government spending and investment remains large, with the government share of the economy at close to record highs.

The improvements in the underlying balance have also flowed into the headline budget estimates –as detailed in the table below.

For 2023/24 the headline deficit is now estimated at -$A6.6bn, well below the May Budget estimate of -$A19.7bn. The headline deficit estimates are now also lower out to 2026/27 –with the improvement over the four years totalling $A36.1bn.

As a result, the net debt profile has also shifted lower. For 2023/24, net debt is expected to reach $A491.0bn (18.4% of GDP), well down on the estimate at the time of the May 2023 budget of $A574.9bn (22.3%) of GDP.

The net debt profile is also lower over the forecast horizon and is expected to reach $A623.9bn (20.8% of GDP) in 2026/27, below the May 2023 budget estimate of $A702.9bn (24.1% of GD).

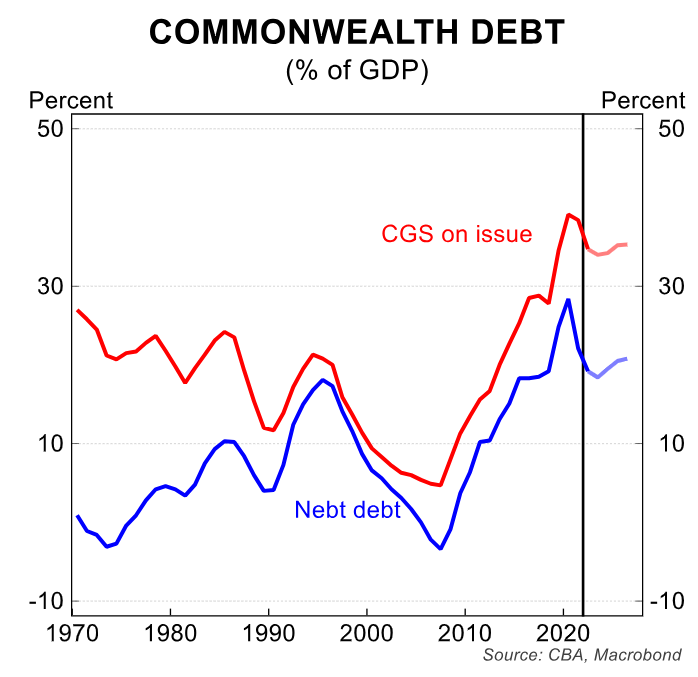

Gross debt is also expected to be lower in 2023/24 and through the out years.

For 2023/24 gross debt is forecast to be $A14bn lower at $A909bn (34.0% of GDP). This will help reduce the borrowing task for the Australian Office of Financial Management (AOFM).

A lower debt profile also reduces net interest payments, although not by much.

For 2023/24 net interest payments are now forecast at $A12.7bn, compared to $A13.4bn as at the May budget.

Over the 12 years to 2033/34 interest payments are now expected to be $A31bn lower, given the lower debt profile.

Interest payments, as well as aged care, health and the NDIS are seeing the largest lifts in growth.

New policy announcements:

There have been some minor new policy announcements contained in the MYEFO.

New spending has largely been driven by lifting funding for prior policies including the closure of the pandemic event visa, the continued response to COVID-19, the response to red fire ants, resolving visa backlogs and other events.

Other new policies include funding for new and amended listings on the Pharmaceutical Benefits Scheme ($A3.5bn over four years) and further funding towards lifting housing supply.

An additional $A3bn of funding for the New Home Bonus was included and $A2bn towards Social Housing Accelerator.

Additional funding of $A3bn was put aside for new investment in critical minerals projects and an additional $A6.8bn to support delivery of current infrastructure projects after the review.

Economic forecasts:

The economic forecasts in the MYEFO provide an update into the Government’s expectations for the economy over coming years relative to the numbers put out in the May Budget.

There was not too much in the way of updates to the Treasury’s outlook for the real economy from half a year ago.

Treasury revised up expected GDP growth this financial year a touch, largely because of ABS revisions to the historical data and stronger-than-anticipated business investment and services exports.

At 1¾% average annual growth, that figure is in line with the RBA’s latest estimates from the November Statement on Monetary Policy.

However, the expected drivers of economic growth have shifted more meaningfully.

The forecast for private final demand growth was nudged down ¼%pt, led by a large 1 percentage point reduction in expected household consumption growth, to just ½% expected over 2023/24.

But this was more than offset by stronger expected public final demand (+1%pt) and a stronger contribution from net exports (+½%pt). Higher-than-anticipated flows of international students will add to near-term strength in exports growth.

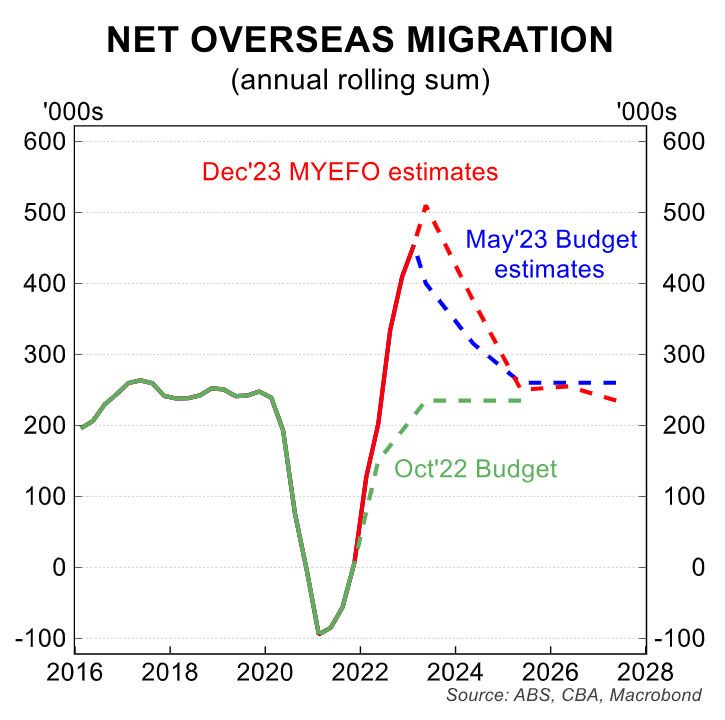

Net overseas migration assumptions have been increased in the near term.

Over the year to June 2023, net overseas migration rose by an expected 510k (May Budget estimate: 400k).

Over the year to June 2024, net migration is expected to ease to 375k (Budget: 315k) and for 2024/25 to be 250k (Budget: 260k).

The near-term upgrades reflect much stronger-than-anticipated outcomes so far. The downgrades in 2024/25 incorporate the government’s reforms to the migration system, announced earlier this week.

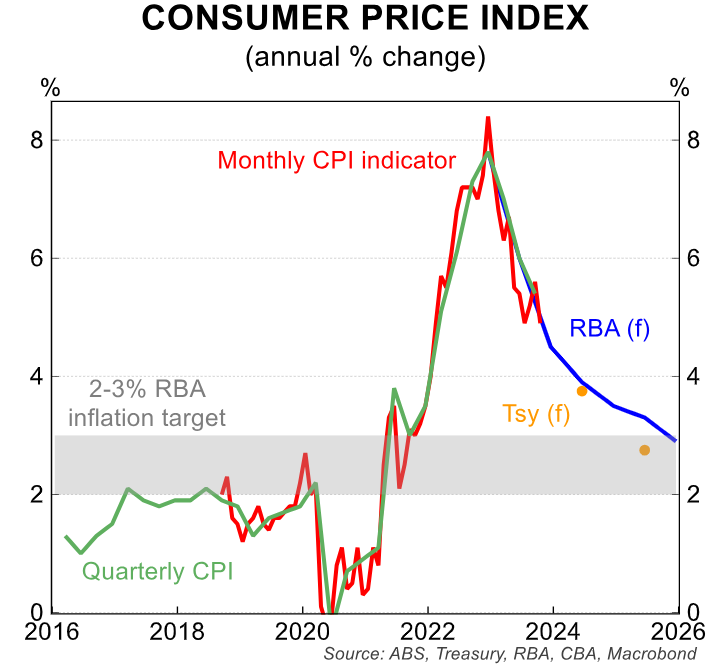

On the prices side, the Government noted that the Q3 23 CPI figure was in line with Budget expectations. Q2 24headline CPI is now expected to come in at 3¾%/yr, a ½%pt upgrade from the Budget (3¼%/yr).

The Government notes that the recent rise in global oil prices was the key driver of the upward revision.

Despite the upward revision, the forecast is a shade below the RBA’s expectation for a 3.9%/yr out turn in Q2 24. But there is a fairly sizeable gap between the two official forecasters for 2024/25.

The Government now expects inflation to return to the RBA’s inflation target by Q2 25, forecasting a 2.75%/yr outcome. In contrast, the RBA sees inflation at 3.3%/yr in Q2 25, and does not see inflation back within the target band until Q4 25 (2.9%/yr) –see below chart.

The Government’s forecasts for wages growth and the unemployment rate in MYEFO were unchanged from the Budget.

Overall, we think the Government’s forecasts for real GDP look broadly fine. They are a tad more optimistic than our forecasts, which is for GDP growth of 1.4% in 2023/24 and 1.9% in 2024/25.

On inflation, our profile for inflation is more similar to the Government’s than the RBA’s. Our point forecast for headline inflation in Q2 24 is 3.6%/yr and for Q2 25 is 2.9%/yr.

It is also worth noting that the MYEFO continues to forecast the iron ore price falling to $US60/t as at June 2024. This is well below the current spot price of $US128/t and also well below our own forecast of $US90/t.

As we noted in our MYEFO preview note, if the iron ore price remains around the current spot price for the rest of 2023/24, this would imply ~$A2bn extra revenue into the budget, pushing the budget into surplus.

Indeed, as also noted in our MYEFO preview, we consider that there remains upside potential the final budget outcome for 2023/24.

We anticipate that the 2023/24 budget is likely to be in surplus by ~$A20bn (0.75% of GDP), based on our more optimistic commodity price forecasts and the strength of the revenue flow into the budget up to October 2023.

This final budget outcome won’t be known, however, until early in the second half of 2024.

Implications for monetary policy:

With the 2023/24 final budget outcome expected to be close to the 2022/23 budget outcome of ~$A20bn, fiscal policy is likely to be a neutral for the monetary policy outlook.

The government is banking the overwhelming majority of the benefits of the economic parameter changes and, if this continues to be the case, fiscal policy will remain a neutral on the economy.

The MYEFO has not changed our base case view that the RBA rate hike cycle is at an end and that monetary policy easing can get underway from September 2024 onwards.

Budget outlook in the out years:

Beyond 2026/27, budget pressures continue to exist as spending pressures grow on the budget.

The deficit is now projected to be 0.3% of GDP in 2033/34, compared to just 0.1% of GDP projected in the 2023/24 May budget.

Fiscal discipline or new revenue sources will be important over time in Australia.

Payments are expected to rise from 25.8% in 2026/27 to 26.6% in 2033/34, slightly larger than the 26.4% expected in the May budget.

This increase largely has been driven by decisions around the NDIS, Medicare and to extend the GST No Worse Off Guarantee.