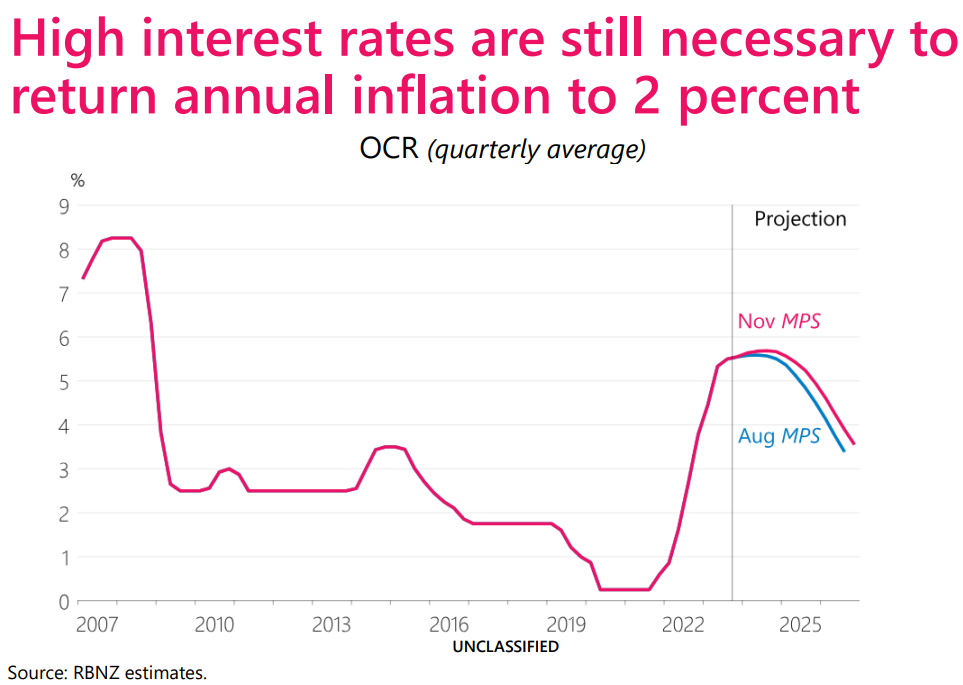

The Reserve Bank of New Zealand held the official cash rate (OCR) steady at 5.5% at Wednesday’s monetary policy meeting.

However, it cautioned that it will need to keep rates restrictive for longer amid persistently strong demand, caused in part by the unexpected record rebound in net overseas migration.

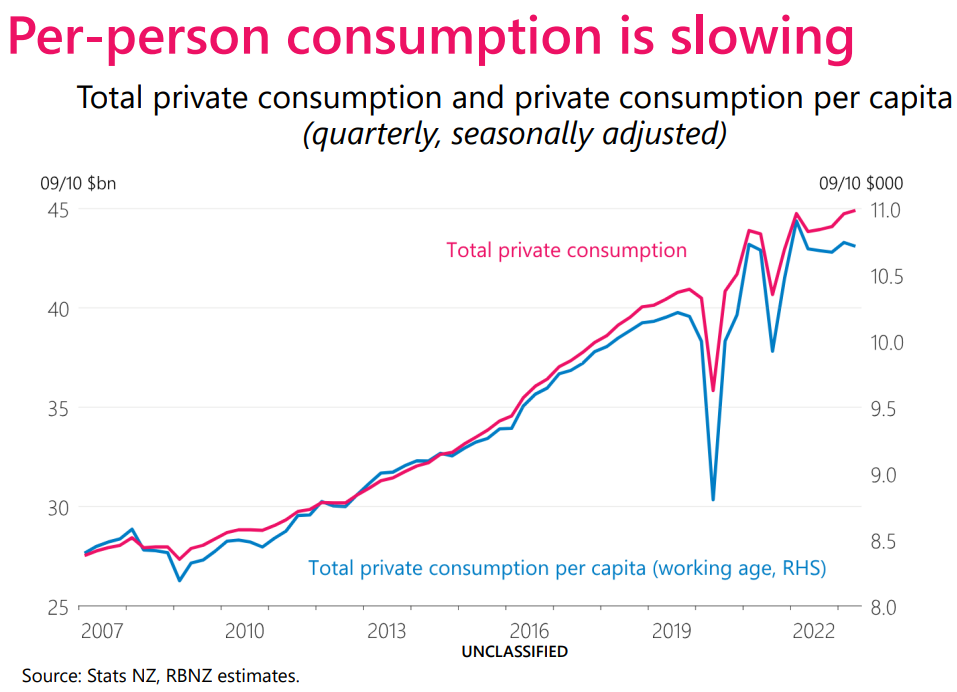

The Reserve Bank noted that “demand growth has eased, but by less than anticipated over the first half of 2023 in part due to strong population growth. The OCR will need to stay restrictive, so demand growth remains subdued, and inflation returns to the 1% to 3% target range”.

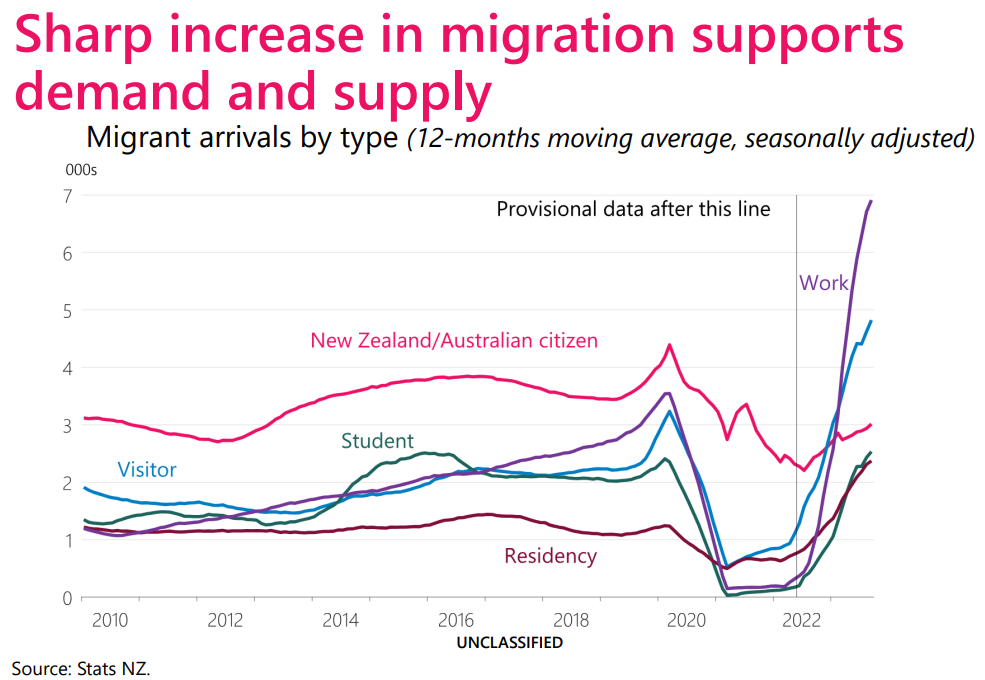

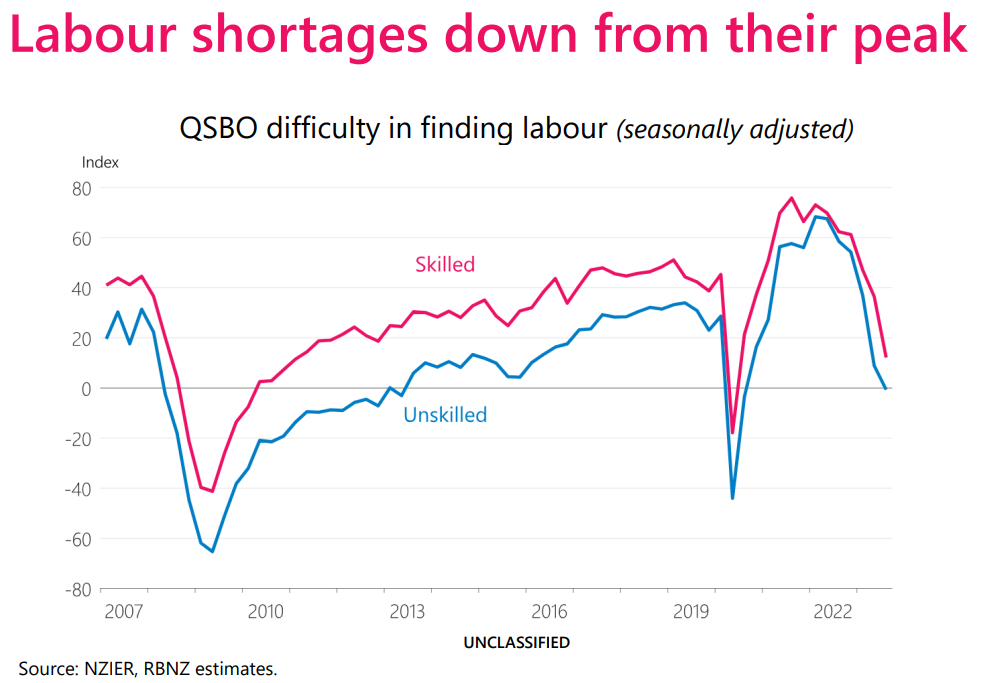

“Members noted that net immigration has been higher than previously assumed. This has increased the supply of workers into a tight labour market”.

“Wage growth has eased from recent peaks. Demand for labour is softening, with job advertisements now below pre-COVID-19 levels. At the same time, strong inward migration is increasing the population and adding to labour supply”.

“While population growth has eased supply constraints, the effects on aggregate demand are becoming apparent. This is increasing the risk of inflation remaining above target”.

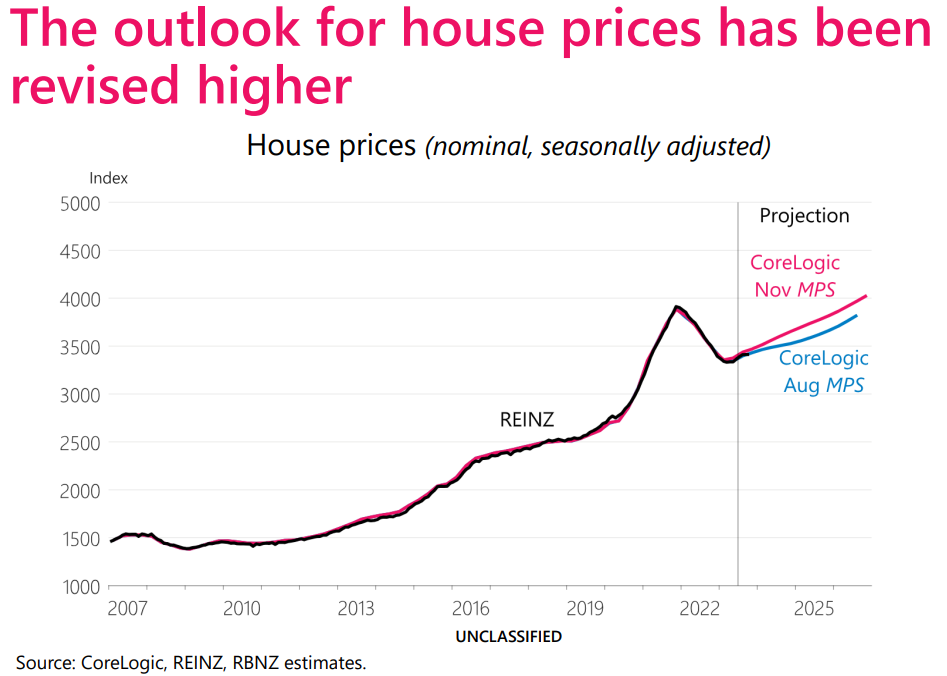

“Strong population growth has contributed to an increase in housing rents. Rent increases, and any increases in construction costs in response to greater housing requirements, affect inflation directly, as rental prices and construction costs are accounted for in the consumer price index”.

“House prices have stabilised after earlier declines, with strong population growth and increased nominal disposable incomes offsetting the effect of higher debt servicing costs”.

“House price increases affect inflationary pressures indirectly, via higher household wealth and an associated increase in consumption”.

So like in Australia, record levels of immigration is juicing demand-inflation while tempering wage-inflation.

It is a lose-lose situation for workers whose real wages will continue to fall while their essential rent and mortgage costs are driven higher.