The Official Cash Rate (OCR) forecast of ANZ economists has been revised downwards, and they no longer expect the Reserve Bank of New Zealand to lift the OCR above its current level of 5.50% at its February meeting.

ANZ’s chief economist, Sharon Zollner, said that it appeared “much less likely” that the inflation rate for the December quarter would be unexpectedly high.

Last week also marked the debut of new monthly price indices, which account for 45% of the consumer price index and indicated that the upcoming quarterly inflation figure might be lower than expected.

This follows the September release of labour market and inflation figures that were both below expectations.

The below note from ANZ Economics explains the reasons behind the bank’s downgraded inflation and OCR forecast.

On track, but a long way from the finish line:

We’re changing our OCR forecast. Our central forecast no longer includes a resumption of hiking, though we still see this as a significant risk.

We have pushed out our expectation for cuts by one quarter (to February 2025), leaving our terminal forecast 25bp lower at 4.75%, which is still considered a contractionary level.

We expect the RBNZ to hold the OCR unchanged at 5.5% at its MPS on 29 November, and publish an OCR track that is very similar to August (with a peak of 5.59% but potentially later cuts).

We don’t expect the RBNZ’s medium-term forecasts for either activity or non-tradable inflation to change significantly (though we’d note ours are higher), with the overall theme continuing to be “so far so good”.

Recent data has been a little mixed but overall has gone the RBNZ’s way (particularly key labour market data), and it is universally expected that the OCR will not change at this meeting.

However, the RBNZ faces a comms challenge, given the market is itching to price cuts more aggressively. We therefore expect a firm tone to the Policy Assessment.

Our call for a hike in February was underpinned by an expectation of a Q3 non-tradable inflation surprise that now looks much less likely to eventuate.

We seriously considered pushing the hike out, rather than dropping it, as we still see the inflation-fighting job taking longer than the RBNZ expects, and we still see a solid chance that a 5.5% OCR will not prove sufficient.

However, we no longer see that chance as being over 50%, which means a higher OCR belongs in the risk basket rather than our central forecast.

Cuts remain a distant prospect, in our view; indeed, we’ve pushed out our estimate of when they will occur by one quarter.

What’s new?

Let’s run through the data that has come out since the August MPS.

Q2 GDP: Considerably stronger than expected, but the population is growing quickly, so the RBNZ will put a chunk of it into their estimate of potential growth rather than the output gap. Still, it’ll be a positive for the OCR track.

This data was already out at the time of the October Monetary Policy Review, when the Record of Meeting noted “The rebound in June quarter GDP data was larger than anticipated, partly reflecting the effects of population growth from high net immigration and momentum in household spending. However, demand growth in the economy continues to ease broadly as expected.”

Note the RBNZ is also likely to revise up its estimate of Q3 GDP, but this is largely due to population growth and therefore doesn’t necessarily imply much for estimates of capacity stretch, which is what matters for inflation.

Q3 labour market data: This is the biggie – and it’s new news. As outlined in our Review, on balance the data suggests the labour market is turning a little more quickly than we or the RBNZ expected.

The huge surge in labour supply via net migration is having a big impact, but labour demand is easing too.

We would caution that there is of course a flip side to migration, namely the boost to demand (we’re watching rents closely) but there’s a tight link between wages and non-tradable inflation, and this side of the coin at least is disinflationary. It’s not simple to estimate how much the data will affect the RBNZ’s labour market and output gap forecasts, but it very likely more than cancels out the Q2 GDP surprise in terms of the published OCR track.

Q3 tradable inflation: Weaker than expected. This type of inflation washes through quickly, but it’s all helpful.

The exchange rate: The trade-weighted index has spent most of its time since the August MPS sitting well below the RBNZ August flat-line assumption of 71, ie more inflationary.

But it’s currently well off its lows and heading north, so here and now it’s not clear that the RBNZ’s forward assumption will be very different.

Q4 monthly inflation indicators: It’s only one month, but the October reads of the new monthly price indexes were low enough for us to revise down our Q4 CPI forecast from 0.9% q/q to 0.6% q/q, and our non-tradable inflation forecast from 1.1% q/q to 0.9% q/q.

The latter is close to the RBNZ’s August MPS forecast of 0.8%, so it’s not obvious whether the data will make the RBNZ change its forecast. The surprise in this data was mostly in volatile CPI components, rather than inflation trends.

However, it’s now a lot less likely that the RBNZ will be revising their starting point for non-tradable inflation higher.

Roughly as expected by the RBNZ (or no news): Q3 non-tradable inflation, the housing market (though we suspect they are seeing upside risk to their forecast), capacity indicators, inflation expectations, mixed business indicators (expectations/intentions are more optimistic, but measures of the here and now are weak, especially the PMI), weak retail spending, supply chain normalisation, oil prices (USD83 currently, USD88 quarter average thus far vs RBNZ August USD85 Q4 assumption), fiscal policy (we assume the RBNZ will run with the PREFU status quo in the absence of firm news), and the terms of trade.

Known unknown: the neutral OCR assumption. This drove the upward revision to the OCR track in August. However, there’s no obvious reason to revisit the assumption at this point.

All up, either a fall or a lift in the OCR track could be justified by the data flow, depending on judgements. That brings into focus strategic considerations.

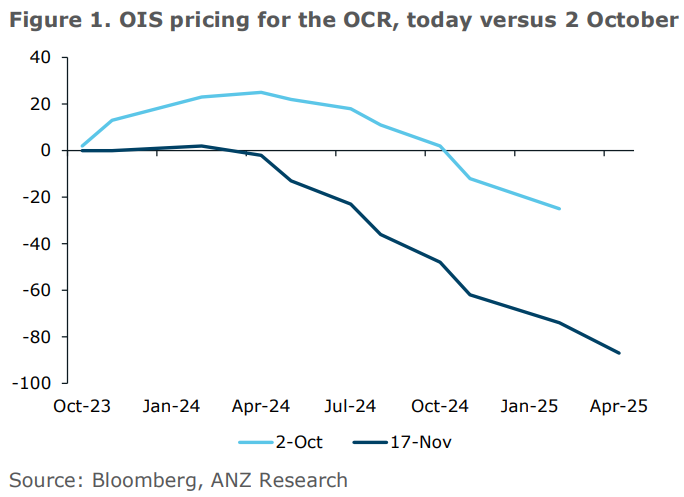

Led by global factors, markets are volatile, but are itching to price in more aggressive OCR cuts. This could see monetary conditions ease over the summer even as the OCR stays put.

This kind of dynamic is quite typical when central banks are perceived to be late-cycle. OIS pricing has already dropped significantly in recent weeks, partly reflecting the local data flow, but also partly reflecting expectations about the US Federal Reserve.

If the RBNZ gives an inch, the risk is therefore that the market takes a mile; in particular, publishing a lower OCR track could cause an unintended and unhelpful easing of monetary conditions.

If the OCR track is raised, on the other hand, the market is likely to raise a sceptical eyebrow.

By far the most straightforward approach, which we think the RBNZ is very likely to take, would be to keep the OCR peak unchanged from August (5.59%), and stress that there is a long way to go yet, and the next move could be in either direction, depending on how the data rolls.

That would also buy them valuable optionality – and is a very common line amongst central banks globally, many of whom are facing variations of the same challenge.

In order to help maintain monetary conditions at a suitably contractionary level over the long summer break the RBNZ may well also push out the timing of expected rate cuts in order to underscore the “don’t get ahead of yourselves” message (but we would note that they are already a long way off: in the August forecasts the OCR only drops below 5.5% in early 025).

Or, taking it up a notch, the RBNZ could explicitly warn that any ‘premature’ easing of monetary conditions might/would warrant an OCR response. Such a line is more likely to be included if the yield curve continues to fall going into the meeting.

Raising the forecast OCR peak would be an even more pointed shot across the bows, while of course the nuclear option would be actually raising the OCR. But we think the market is right to put negligible odds on that, given the recent data flow and the (relatively) relaxed tone of the October Monetary Policy Review.

Our new OCR forecast:

As discussed above, given softer-than-expected October monthly price data we have revised our Q4 inflation forecasts down, including the key non-tradable component.

This is the most important data to be released between now and the February MPS, and our forecast for a hike as soon as February was based on our expectation of a large upward surprise for the RBNZ that now looks much less likely to eventuate.

Accordingly, a February hike would now require developments that we are not expecting (though one certainly can’t rule them out), such as a sharp rebound in the housing market or capacity indicators.

However, we don’t find it difficult to envisage scenarios where the RBNZ hikes again next year. Getting inflation down from 7.3% to, say, 4% is relatively easy, but that last 2% could be very hard going indeed, and we do see the task taking longer than the RBNZ expects.

The ducks are currently lined up but have a long way to march in formation yet. But this is a slow-burn story, not a near-term one. And data suggests labour demand has turned three months sooner than we anticipated.

That means our conviction that further hikes will be needed has dropped below 50%, so the hike needs to be transferred out of our central forecasts and into the risk basket.

The top of the risk basket, to be clear! We won’t hesitate to put a hike back in our forecasts if we think it’s needed, and nor will the Reserve Bank. They will certainly not close that door in this Monetary Policy Statement.

The recent data has seen our conviction dip under that 50% odds line for another hike, but it’s an incremental change in view: it’s not as if we think the size of the task at hand has suddenly massively shrunk.

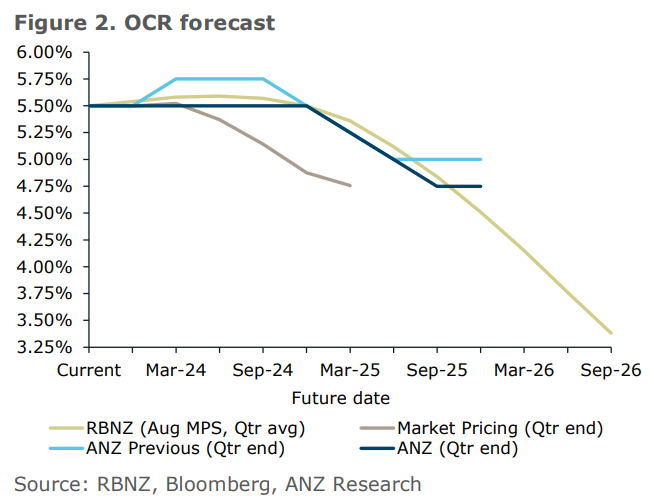

Our updated forecast pushes out cuts by one quarter compared to our previous view in order to maintain a similar OCR level as before over 2025.

Of course, 2025 is a very long way away, and anyone’s forecasts should be taken with a large grain of salt, but for those interested in the details, we have pencilled in 25bp cuts for February, May, and August. That’s one cut per MPS, as opposed to consecutive meetings, consistent with our view that domestic inflation will prove stickier than anticipated and that the RBNZ will want to feel its way carefully through the easing cycle.

That compares to our previous call for cuts in November 2024, February 2025 and May 2025 (figure 2). Our terminal OCR forecast is now 25bp lower than previously at 4.75%, which is still considered contractionary territory.

Our views are not aligned with market pricing that has 23bp of cuts priced in by July and another 25bp (for 48bp in total) by October.

At the end of the day, inflation is still roughly twice where it should be. Non-tradable inflation will fall – is falling – but not off a cliff, because the economy isn’t going off a cliff.

It’s slowing, certainly, and there’s real pain out there in pockets, but that’s what a ‘soft’ landing feels like – it’s still a descent, after all, from what was an unsustainable flight path.

There are of course developments that could see cuts much sooner than we are forecasting; there are always risks on both sides. But if the OCR does move in the next six months, in our view it’s still likelier to be up than down.

To cut rates, inflation needs to be a lot closer to target, and the RBNZ needs to be confident it’ll get there and stay there.

Given how the market will rush to price more cuts, the RBNZ would need to be comfortable with a sharply lower yield curve overall, not just a lower cash rate. And we’re a very long way from that point as things stand.