Roy Morgan has released its latest mortgage stress survey, which was taken before this month’s 0.25% hike in the official cash rate (OCR) by the Reserve Bank of Australia (RBA).

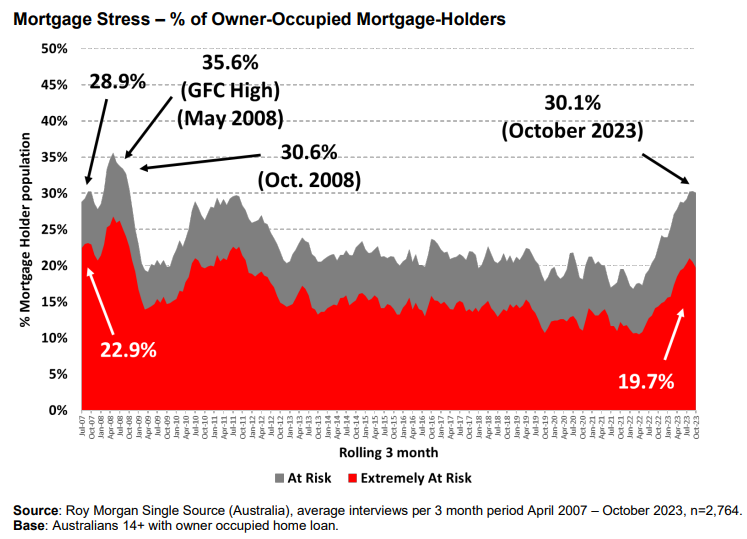

It shows that mortgage stress nationally eased slightly, with 1,514,000 mortgage holders (30.1%) “at risk” of mortgage stress in the three months to October:

“The figure for October represented a slight decrease on a month earlier as mortgage stress eased due to a combination of several factors including increased household incomes, increased employment and reduced amounts borrowed and outstanding”, noted Roy Morgan.

“However, despite the slight easing in mortgage stress this was only the third time in the history of the index that over 1.5 million mortgage holders were considered ‘At Risk’.”

“The number of Australians ‘At Risk’ of mortgage stress has increased by 707,000 since May 2022 when the RBA began a cycle of interest rate increases. Official interest rates are now at 4.35%, the highest interest rates have been since December 2011, over a decade ago”.

“The number of mortgage holders considered ‘Extremely At Risk’, is now numbered at 967,000 (19.7% of mortgage holders) which is significantly above the long-term average over the last 10 years of 14.1%”.

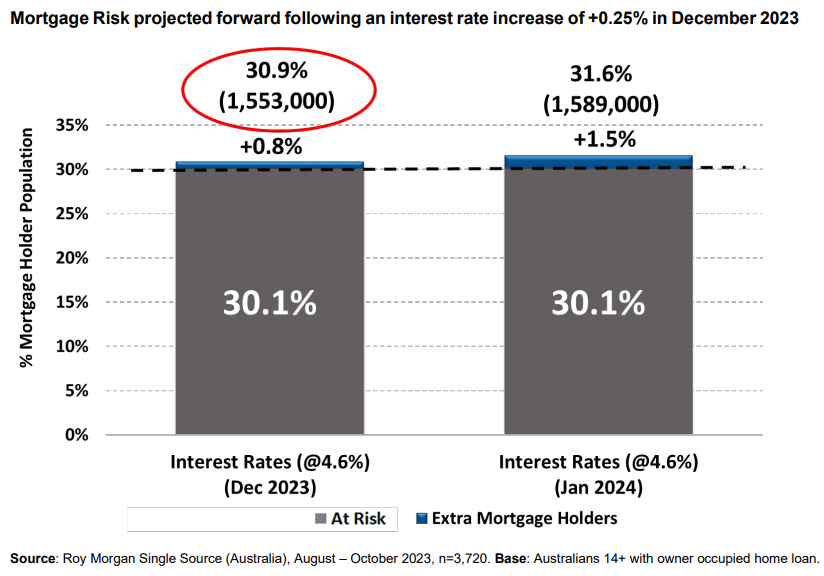

Roy Morgan estimates that 1,553,000 (30.9%) of households would fall into mortgage stress if the RBA hikes the OCR again in December:

Roy Morgan measures ‘mortgage stress’ in two ways:

- Mortgage holders are considered ‘At Risk’ if their mortgage repayments are greater than a certain percentage of household income – depending on income and spending.

- Mortgage holders are considered ‘Extremely at Risk’ if even the ‘interest only’ is over a certain proportion of household income.

It is important to note that Roy Morgan uses “a conservative model, essentially assuming all other factors remain the same”.

Since having a job is the key determinant of whether a household can pay their mortgage, mortgage stress would rise materially if Australia’s unemployment rate increased significantly.

“The greatest impact on an individual, or household’s, ability to pay their mortgage is not interest rates, it’s if they lose their job or main source of income”, Roy Morgan says.

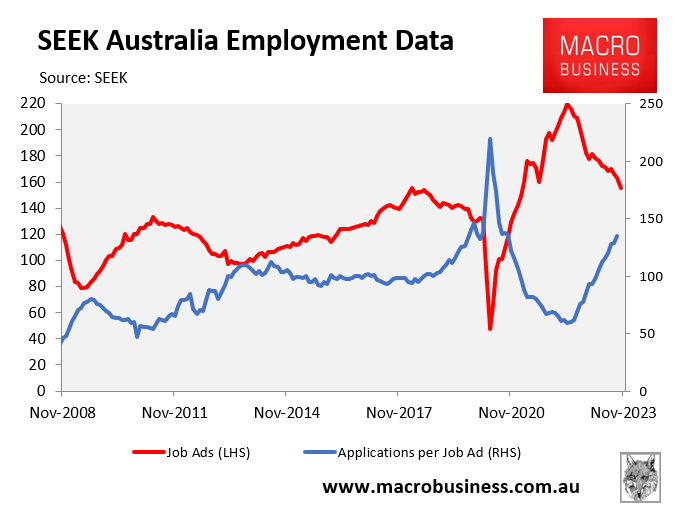

The latest SEEK data showed that labour demand (as measured by job ads) has fallen significantly at the same time as labour supply is growing at a record pace via net overseas migration.

In turn, the number of applicants per job ad has soared well above pre-pandemic levels:

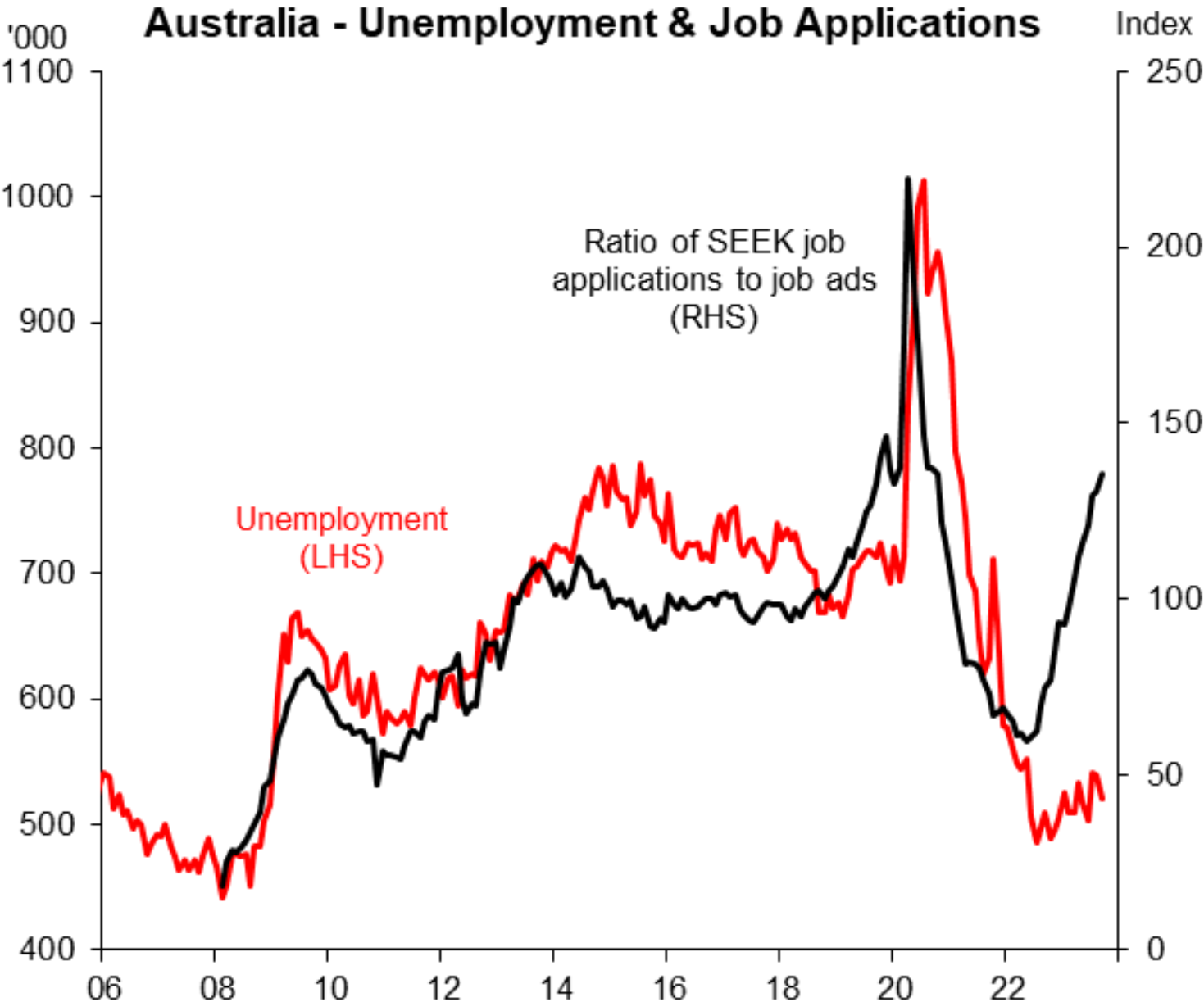

This signals that rising unemployment is on the horizon, as illustrated by the next chart from Justin Fabo at Macquarie Group:

Record labour supply growth in a slowing economy is a recipe for higher unemployment.

In turn, we could see mortgage stress rise sharply in 2024, even if the RBA keeps the OCR on hold.