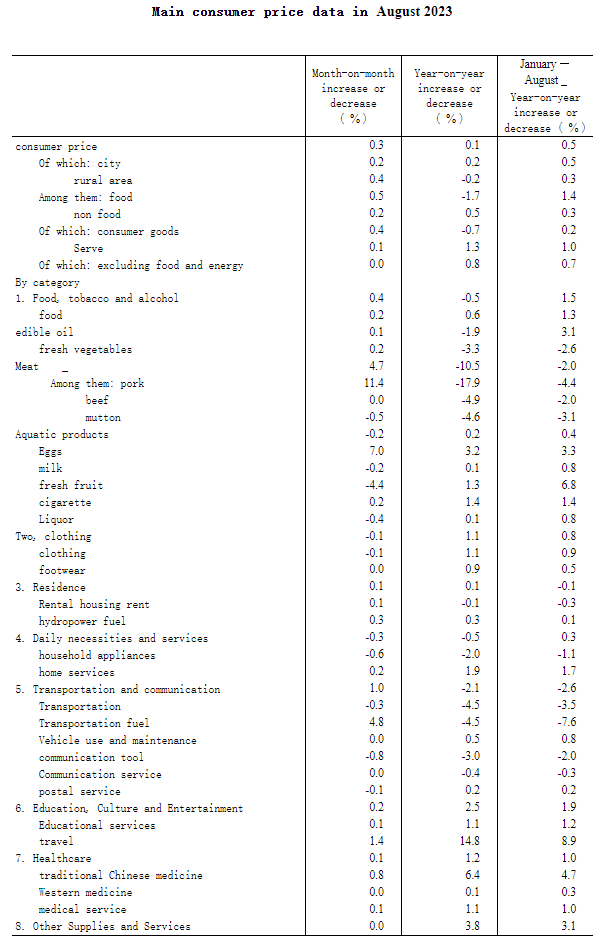

Over the weekend, China released its inflation numbers for August. They managed to climb into the positive but it was fa from convincing, driven by only pork and oil.

CPI was all pork and petrol:

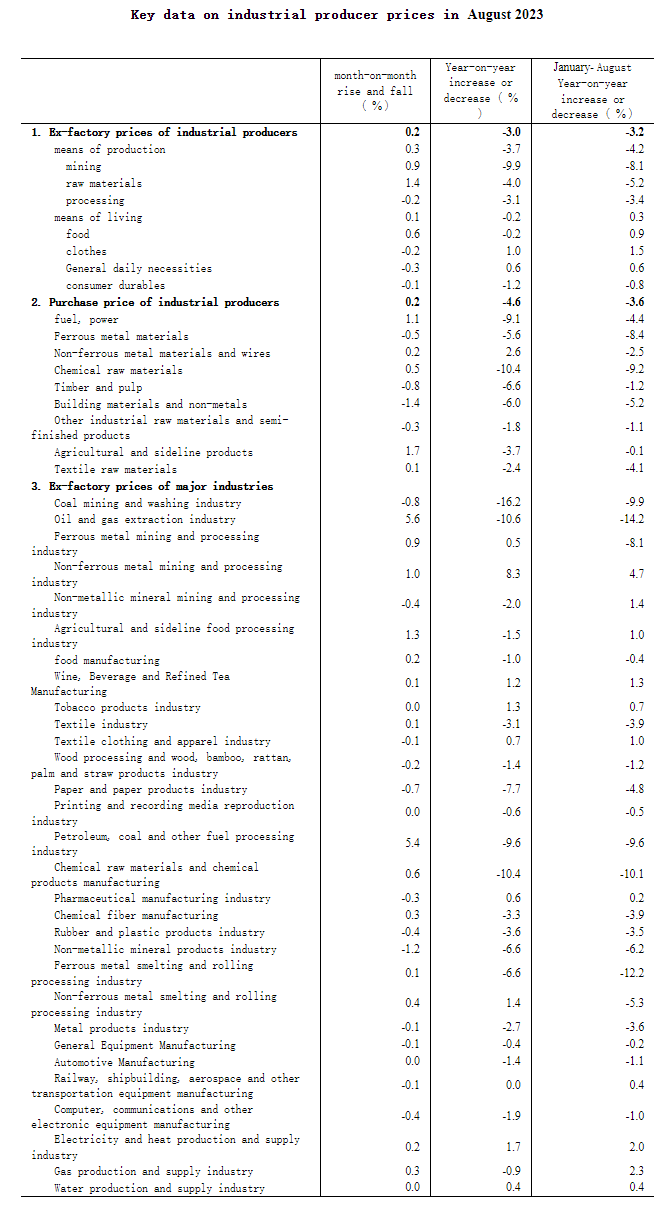

PPI was all oil:

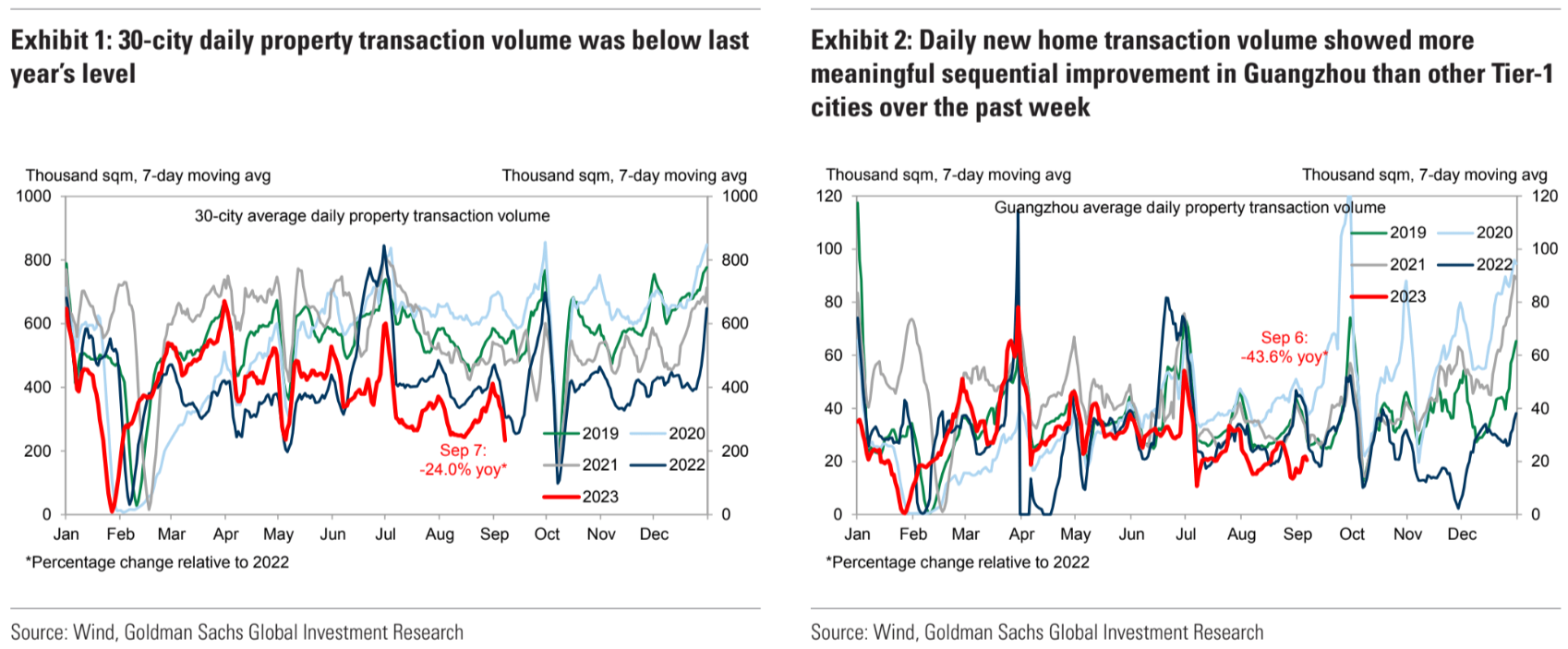

Meanwhile, the driver of weakness, the realty crash, shows no sign of abating despite great media hoopla:

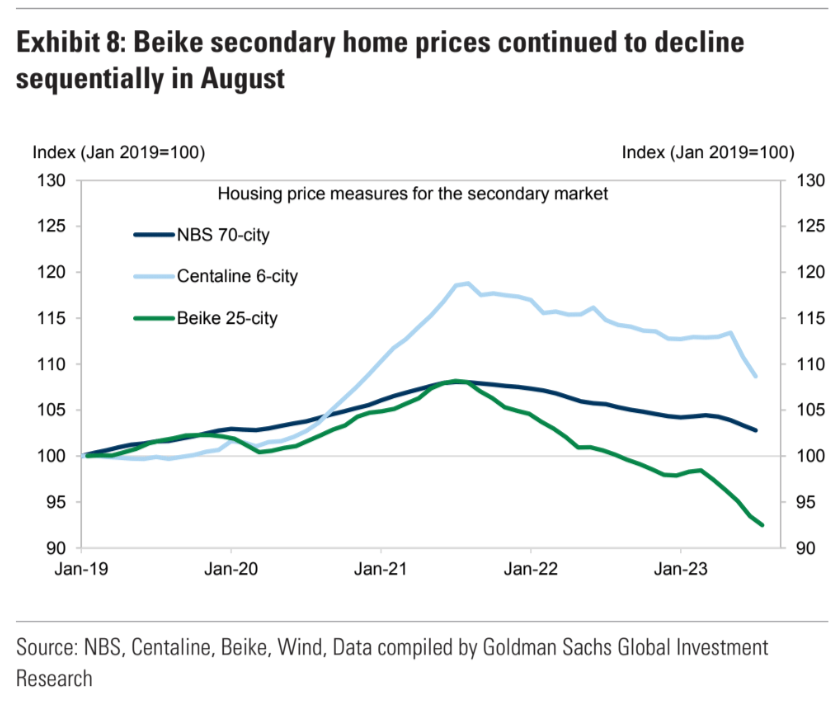

Why would sales improve when prices are crashing?

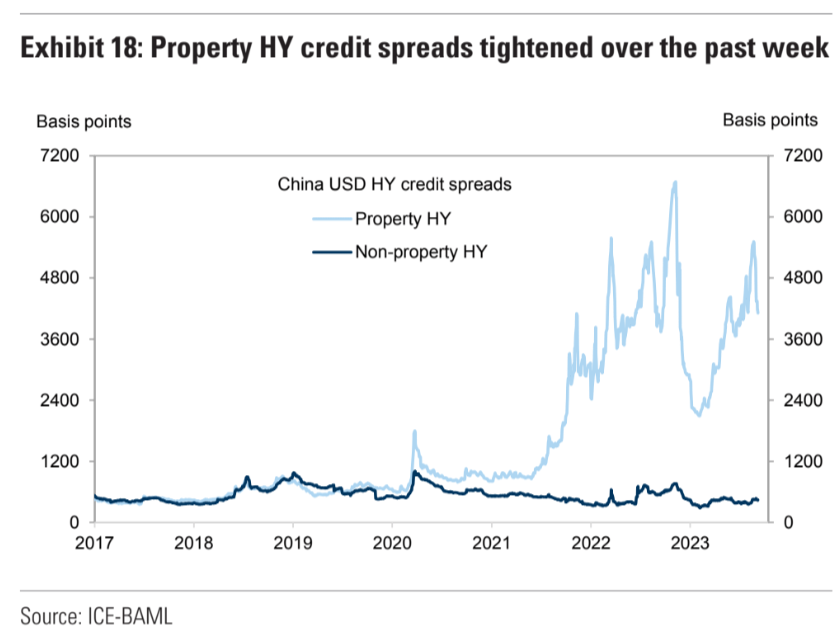

Not that it would matter much if sales did pop. Developers are still locked out of debt markets, despite some improvements via Country Garden:

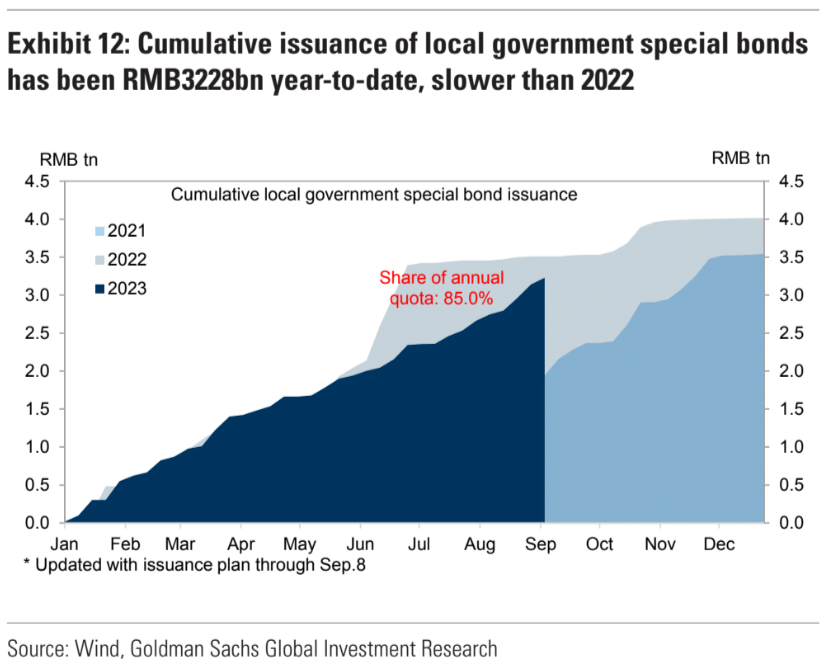

LGFV issuance is pushing towards its quota fill but is still down 5% year on year. One possible stimulus is another special quota but how that would sit alongside Beijing’s dictum to deleverage is not obvious:

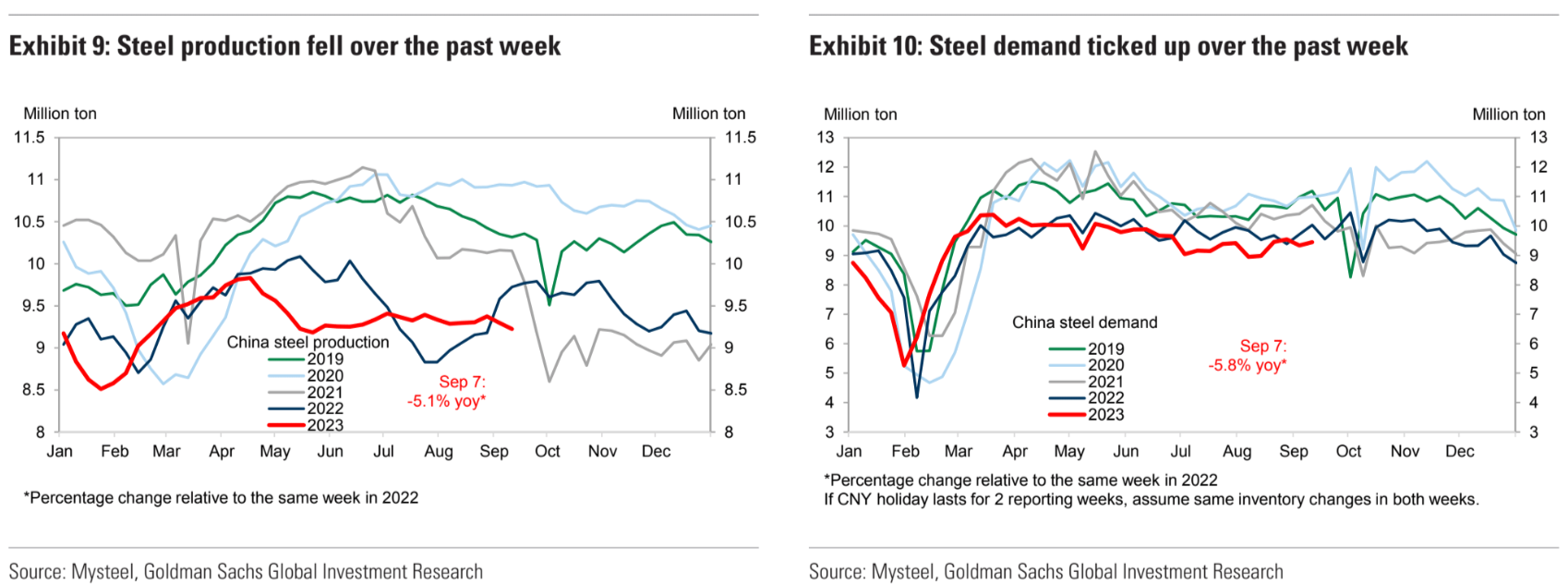

All up, there is nothing here to suggest anything other than more falls in construction steel demand ahead as completions catch down to starts. The latest My Steel numbers suggest much the same:

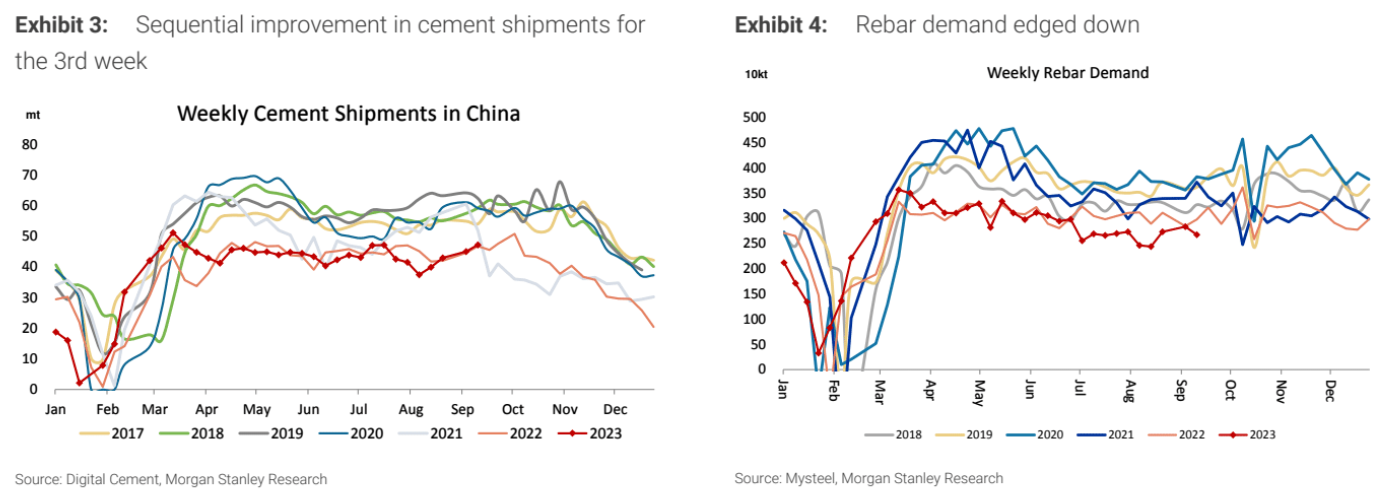

Rebar is especially weak:

There are signs of a weakening market as high-grade spreads tumble amid weak steel margins:

Onwards and downwards for China and iron ore ore.