It began with Evergrande, and it is returning with Evergrande:

The crisis at China Evergrande Group deepened Monday after the company’s mainland unit said it failed to repay an onshore bond, adding a new layer of uncertainty to the developer’s future as a restructuring plan with its offshore creditors teeters.

The builder at the center of China’s property developer crisis said its Hengda Real Estate Group Co. subsidiary defaulted on 4 billion yuan ($547 million) in principal plus interest due Sept. 25. In March, Hengda missed an interest payment on the 5.8% yuan bond issued in 2020, and said it would “actively” negotiate with bondholders to find a solution, a promise it reiterated in Monday’s statement.

Evergrande is running out of time to get what would be one of the nation’s biggest-ever restructurings back on track after setbacks in recent days have raised the risk of a potential liquidation. The company has scrapped key creditor meetings at the last minute, saying it must revisit its restructuring plan, faced the detention of money management unit staff, and been unable to meet regulator qualifications to issue new bonds.

That last item is a major blow to its planned restructuring of at least $30 billion of offshore debt that would have creditors swap defaulted notes for new securities. Evergrande’s shares plunged as much as 25% Monday.

Meanwhile, Caixin reported Monday that Xia Haijun, an ex-chief executive officer of Evergrande, and Pan Darong, a former chief financial officer, have been detained by Chinese authorities.

This looks like the endgame for China’s greatest ponzi scheme. Will the government step in with a restructuring of its own?

The last time Evergrande was in dire straits like this was about a year ago when its stalled projects helped shunt iron ore lower.

Advertisement

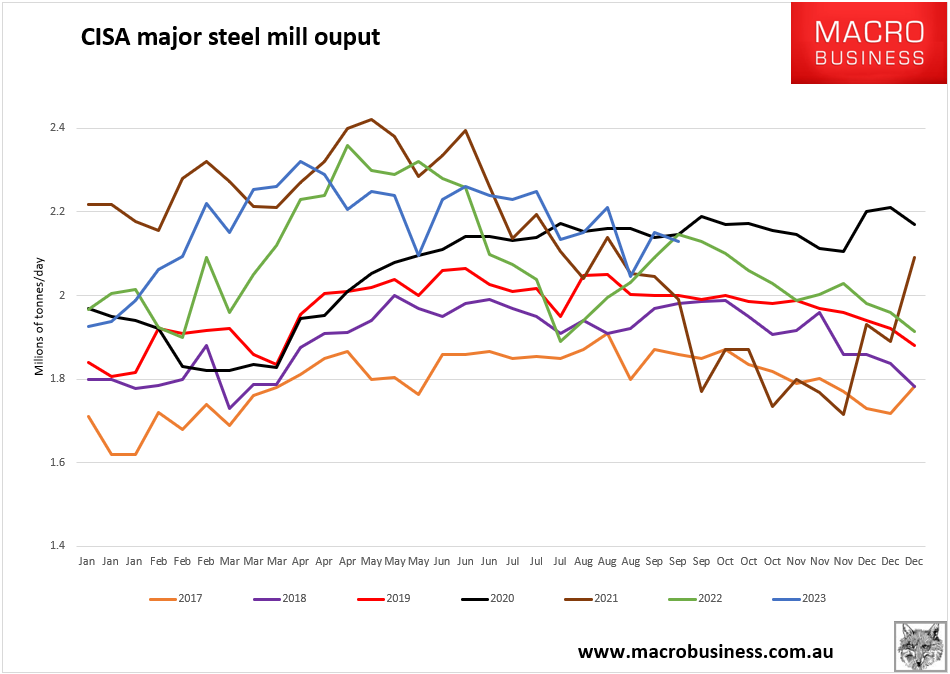

Output caps accompanied that underlying demand weakness so steel production fell sharply through the end of the year. We appear poised for repeat as CISA output data fades:

Iron ore is overbought, and much of it is speculators. There are some loose hands to shake out here:

Advertisement

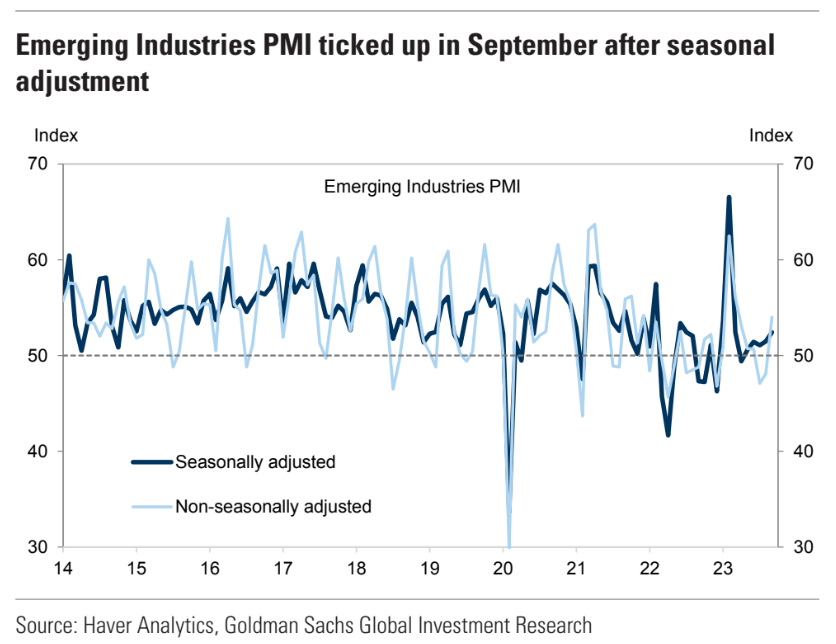

We may get some reprieve from the looming PMIs. Goldman:

September NBS manufacturing PMI expected to go above 50: The“Emerging Industries PMI”, which is typically released around the 20th of the month and has predictive power over the official NBS manufacturing PMI, showed an uptick in the latest release. Combined with residual seasonality, we expect the official NBS manufacturing PMI to rise to 50.2 in September from 49.7 in August. If this materializes, it would be the first above-50 reading since March.

Advertisement

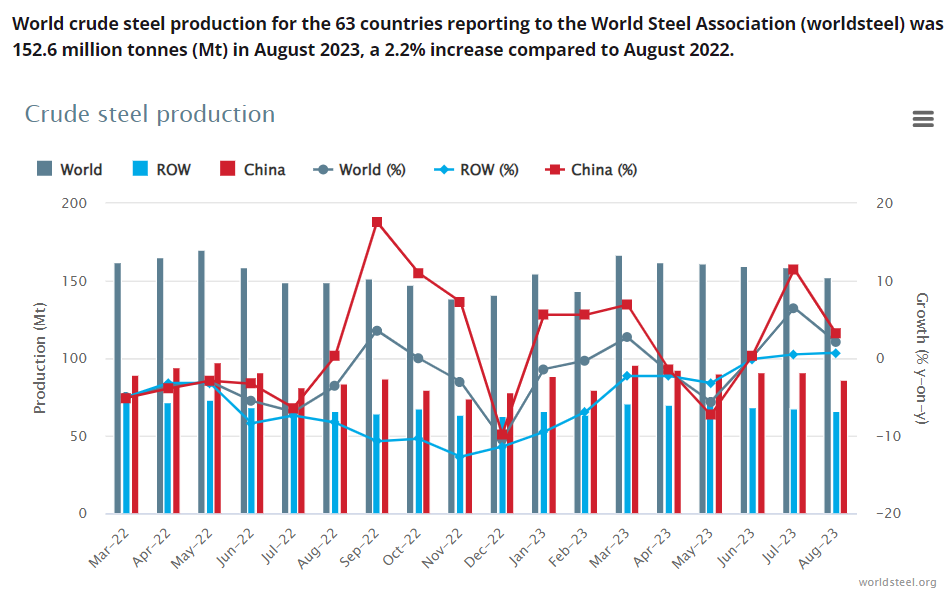

However, a repeat of last year’s global falls in steel output for Q4 remains the base case:

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.