Citi with the note.

Over the past two years, the global economy has seen high inflation and tightening monetary policy, while global growth has remained at or just below trend. We judge that the economy is approaching a transition point. The previous features of performance have not yet fully played through—but they are looking long in the tooth. And we’re seeing evidence of a new regime characterized by gradual disinflation and decelerating growth.

In line with this narrative, we see particular vulnerability for the global economy during the first half of next year, as DM growth is expected to post an outright contraction. Accordingly, DM central banks now look to be reaching the peaks of their tightening cycles and, next year, are likely to shift policy toward easing as evidence of slower growth and softer inflation becomes clear. Several major EM central banks have already started to ease policy.

Global growth this year is likely to come in at 2.3%, nearly ½ percentage point higher than we projected at the end of last year. But we continue to anticipate that this upside surprise will give way to weaker performance next year. We now see global growth in 2024 falling to just 1.7%, more than a percentage point below our projections late last year. The first half of next year looks likely to be particularly weak.

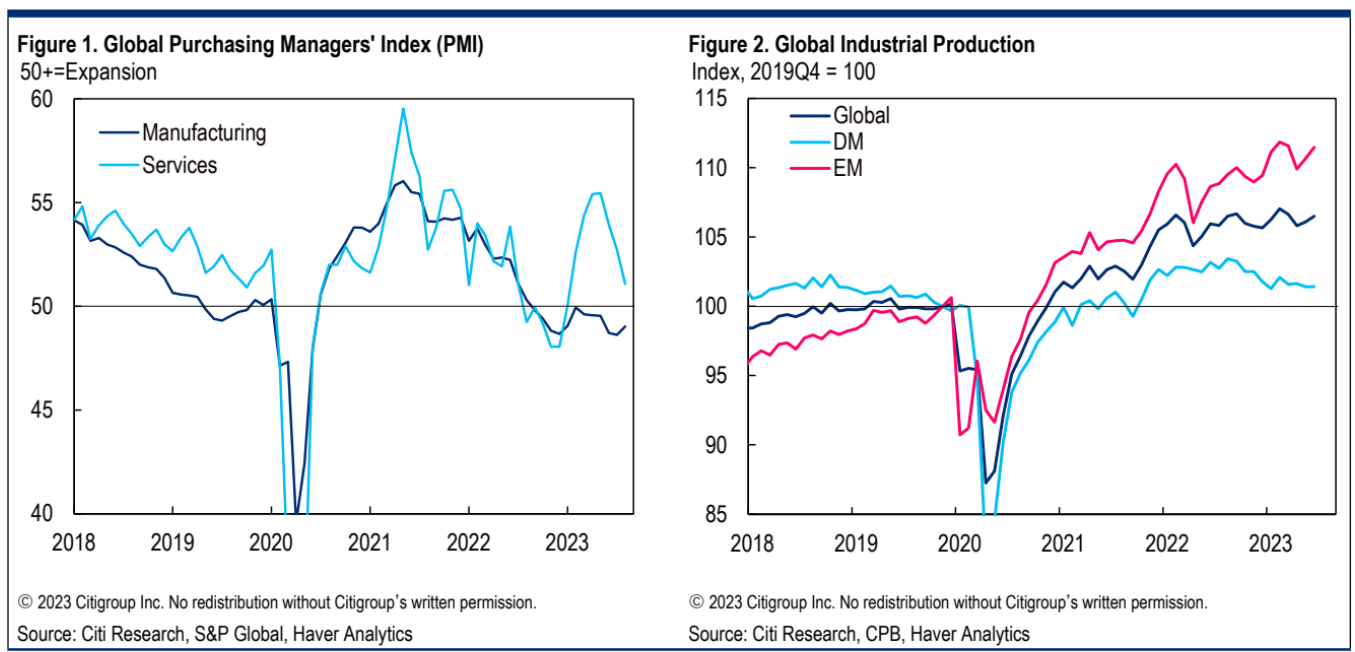

The global manufacturing PMI has languished below 50 through the past year. This weakness is echoed in global industrial production, which has essentially stagnated. Notably, over the past few months, the services PMI has retreated sharply as well, suggesting that red-hot services spending is cooling. The weakness in global manufacturing may be starting to undercut economic sentiment more broadly.

The divergence this year of growth cycles in the United States, the euro area, and China has been another key theme. US performance has been surprisingly solid, while growth rates in the euro area and China have disappointed, albeit in different ways. Going forward, we see a realignment of these cycles in favor of soft performance. We continue to believe that a US recession will be necessary to cool inflation, and we’ve sharply marked down our projections for euro-area growth.

We see global inflation gradually declining as tight central bank policies restrain spending and growth moderates. Labor markets should start to loosen and services inflation should eventually yield. We see inflation drifting down toward central bank targets by the end of next year. The recent run-up in oil prices, which we expect to be short-lived, represents a key challenge.

Our forecast continues to grapple with the risk of a global recession. Notably, during the first half of next year, the global economy is projected to expand at only a 1% rate. Excluding China, global growth is seen to turn slightly negative. This performance looks increasingly like a “broad-based” downturn. Even so, global growth surprised on the upside this year, and we recognize that we may be surprised yet again.

Looks right to me.