Health Services Union executive Gerard Hayes recently pushed for the introduction of a Medicare-style aged-care levy.

Hayes argued that the proposed 0.65% charge would guarantee that senior Australians receive enough care and that workers in the field are properly compensated.

The aged care royal commission also suggested an income tax levy and changes to personal income tax levels.

The commission recommended a minimum levy of 1%, which would rise with age and with taxable income.

Earlier this week, The SMH’s Money columnist, Noel Whittaker, called for an increase in the GST to pay for aged care. He also pushed back against forcing wealthier older Australians from drawing down their superannuation nest eggs:

“For years, the anti-superannuation lobby has focused on the fact that the majority of retirees die with substantial money in superannuation”.

“They see this as proof that they should never have been allowed to accumulate that much money in the first place”.

“Suddenly, there’s been a change of attitude, and now there are suggestions that superannuation should now be earmarked for their aged care”.

“We are stuck with a situation where it’s impractical to tax existing taxpayers to fund the aged care of senior citizens, and special taxes on superannuation would never work because people would opt out of the system”.

“The only solution available is to raise the GST to 15% with no exemptions. This would not only catch every Australian irrespective of age but would also raise a fortune from the cash economy”.

“Finally, every Australian would be paying their fair share of tax”.

While Whittaker’s GST suggestion is better than an income tax levy, since older retirees would also pay, it would still place too greater financial strain on younger Australians.

Let’s get real. For decades, successive Australian governments have stacked policy against the young in favour of the old.

Governments have handed generous tax breaks to the aged. Older individuals can earn high incomes that are largely tax-free, whereas young people on the same income must pay up.

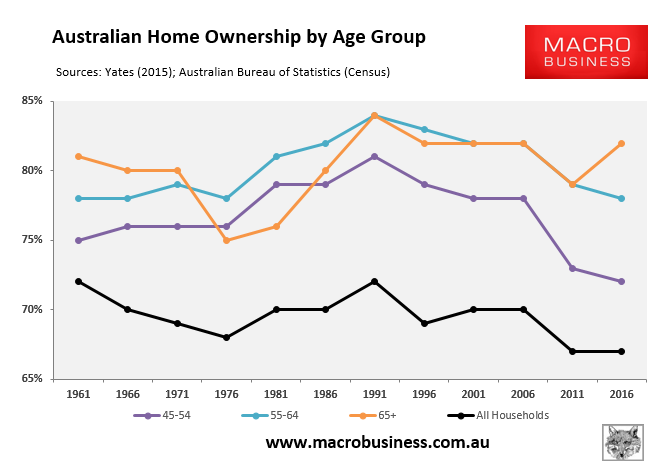

Baby boomers have the highest home ownership rate in Australia and were lucky to have gotten into the market while houses were still reasonably priced. They then enjoyed the rapid appreciation of home values, while younger Australians have been priced out.

Many baby boomers have also been able to purchase an investment property or two.

This means many are sitting on vast sums of wealth, while their children and grandchildren struggle to pay their mortgages or rent.

Most decent jobs 40 to 50 years ago didn’t require higher education. Yet, most boomers that did go to university enjoyed free education, while fees for younger Australians have become a major financial roadblock early in life.

Finally, as noted in The Conversation, “taxpayers already pay the lion’s share of all aged-care funding”.

“This imbalance is even more extreme for home-care packages, where consumer contributions comprise only 2.2% of total funding”.

“This means the average home-care client who receives about $25,000 worth of services each year only pays $550 a year or about $1.50 per day”.

Ross Gittins said it best in June when he wrote: “If Labor doesn’t summon the courage to ask those Baby Boomers who’ve done OK to help pay directly for the cost of their highly privileged lives’ last stage, it will just prove what a rotten world Albo and the rest of us have left our offspring”.

If these seniors require additional finances to pay for their aged care, they can apply for a ‘reverse mortgage’ through the government’s generous Pension Loans Scheme.

Australia has already found itself in the peculiar predicament of older generations enjoying unprecedented rises in wealth while their reliance on the Aged Pension has increased rapidly and is expected to continue.

Meanwhile, relatively poorer younger Australians are heavily subsidising the retirements of many wealthy retirees, whose most valuable asset (primary dwelling) is mainly excluded from their ability to support their own retirements.

This scenario makes no sense from the standpoint of either budgetary or intergenerational justice.

Implementing an aged care levy or raising the GST would exacerbate these intergenerational imbalances.