Chinese real estate stocks are close to losing all the gains notched during last year’s massive reopening rally as troubles mount for the debt-laden sector.

A Bloomberg Intelligence gauge of real estate stocks trading on the mainland and in Hong Kong is less than 3% away from piercing below its end-October trough, which was the lowest since 2011. The gauge had surged 88% in less than six weeks back then as China’s move to dismantle Covid controls and a gamut of supportive measures for the property sector raised hopes for a revival.

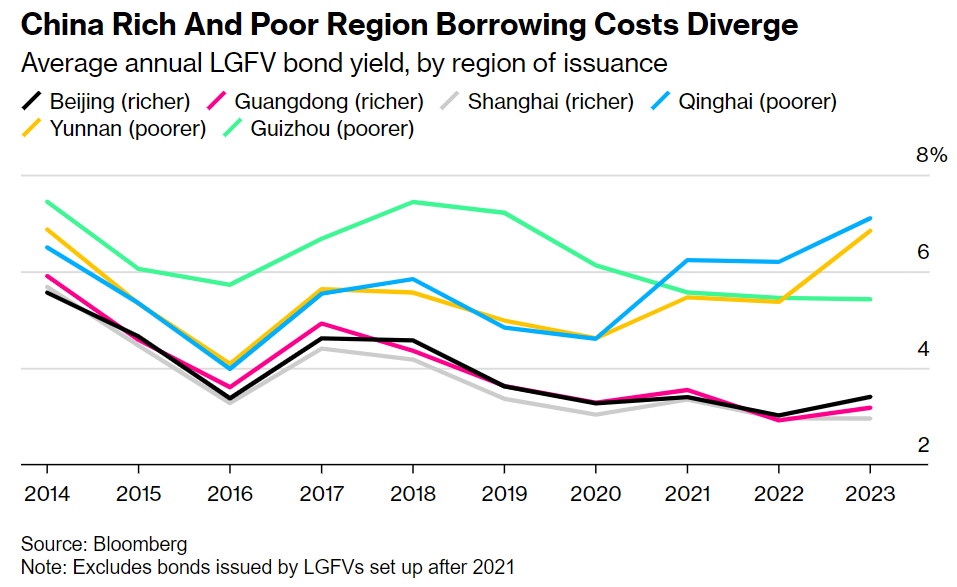

China is attempting to defuse risks from its $9 trillion pile of off balance-sheet local government debt, without resorting to major bailouts.

That path forward is a treacherous one for President Xi Jinping’s government. To thread the needle, the provinces and cities whose borrowing drove the world’s largest infrastructure boom will need to roll back their spending and restructure debt — all without drastically dragging down economic growth. If they fail, it could thrust the world’s second-biggest economy into a prolonged malaise.

At the center of this dilemma are local government financing vehicles, companies set up across China to borrow on behalf of provinces and cities but not explicitly in their name. Xi’s government has sought to turn these firms into profitable businesses so they’d no longer need government money to pay the interest on their debts.

But interviews with employees at six such firms in separate provinces suggest the effort isn’t working in poorer inland regions.

Several companies haven’t been able to generate enough income to pay interest on loans. Banks are unwilling to lend, investors are shunning their bonds, bonuses are being cut and it’s becoming harder to find viable investment projects, the employees said, asking not to be identified due to the sensitivity of discussing government finances publicly.

If the central government avoids a bailout, the burden of repayment will fall increasingly on local governments or on banks tasked with lowering interest rates and extending maturities on the debt. Both options will limit the capacity of local governments and banks to support economic growth.

It’s a worry for investors, as well, since any default on LGFVs $2 trillion of bonds — which account for nearly half the country’s onshore corporate debt market — would destabilize China’s $60 trillion financial system, producing global shockwaves.

“The most important variable impacting China’s economic growth over the next two years will be the success or failure of local government debt restructuring,” said Logan Wright, director of China markets research at Rhodium Group. “A collapse in local government investment would be comparable to the economic impact of the crisis in the property market.”

The Communist Party’s Politburo hinted in July at steps to resolve the debt risks, and Beijing now appears to be following through. It’s allowing Chinese provinces to raise about 1 trillion yuan ($137 billion) from bond sales, which can be used to pay-off LGFV debt, according to people familiar with the matter.

While that’s a fraction of all LGFV debt — the International Monetary Fund estimates a total of 66 trillion yuan this year — the move has increased market confidence in the companies’ bonds. Beijing is also considering using the central bank to provide liquidity to the most-strained LGFVs, local media Caixin reported.

But these fixes were not Beijing’s first choice. It set in motion a plan before the pandemic to inject state-owned assets into the companies and permit them to enter new business areas to generate enough cash to service debt on their own. This was known as the “market-oriented transformation” model.

An example from a mountainous district in southwest Chongqing shows how that plan is falling short. A local government-owned company there borrowed billions of yuan to build roads, water pipes, factory buildings, and affordable housing. It transformed a former mining area into a development zone for factories, which converts coal into chemicals.

Economic output in the zone increased fourfold in just over a decade. Like other LGFVs, the infrastructure built was provided for free or very cheaply to the public and businesses as part of their responsibility to promote “public welfare” and economic growth.

To make the LGFV more financially self-sufficient, the local government in Chongqing gave the company a license to sell coal to factories. But profit from that business wasn’t enough to cover the company’s interest payments. As a result, the most recent reports show the company’s short-term debt is six times its cash on hand.

“We are indeed talking about transformation,” said an employee who works at the company in Chongqing. “But to be honest, so far we have not found out any good path to transformation yet.”

China has thousands of these LGFVs spread out across the country, businesses that were set up to develop local economies. Last year alone, they pumped more than 5 trillion yuan into the economy, according to a tally from Rhodium Group.

The companies rely on local governments for income, in the form of payments for infrastructure and pure subsidies. They also borrow from banks and by selling bonds, which are generally seen as carrying an implicit government guarantee of repayment.

That was fine so long as banks were willing to roll over the company’s debt when it was due, and so long as the economy was growing fast enough that the local government made enough revenue to pay subsidies to the company.

But that funding model is now under unprecedented strain. Firstly, a record amount of LGFV debt is maturing. Secondly, local governments, especially in poorer areas, are seeing revenues drop due to a two-year slump in home sales.

And thirdly, banks and investors have become less convinced Beijing will bail out some LGFVs if they go bust, pushing up the interest rates on bonds and loans, and making it harder for weaker companies to access financing.

Advertisement

The incremental stimulus approach is only making this worse. Then again, what choice does China have? If it accelerates restructuring then it will crash growth and create the very outcome it seeking to avoid.

An explosive crisis is probably still the risk case. Thought the further property falls, the closer it creeps. And there is the distinct danger that some cadre, perhaps all, are going hide the bad news as long as possible from the God King. Until something breaks.

The best case is periodic eruptions of debt stress in an endless bog of forced mergers, recapitalisation, extend and pretend. It is pure Japanification that will take down the good as they support the bad.

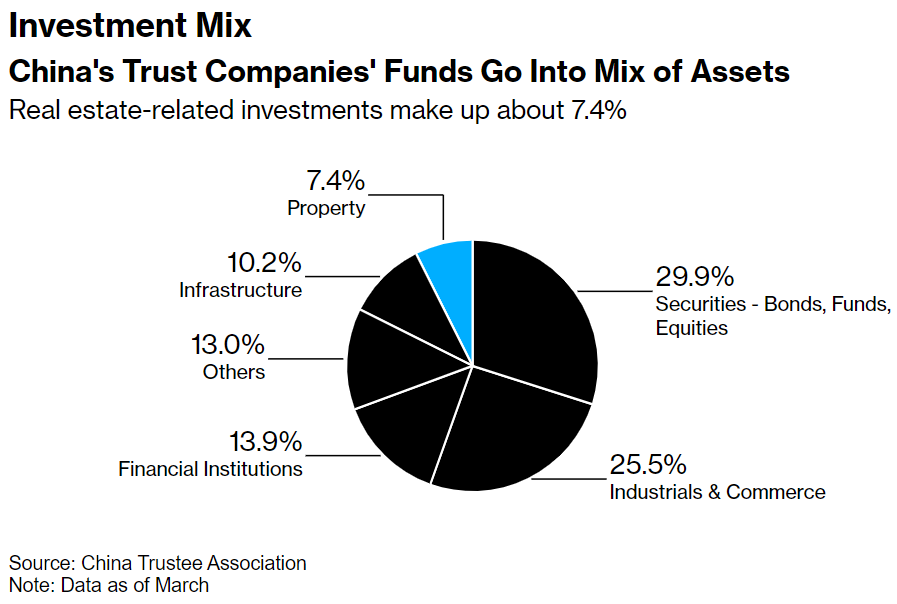

China’s $2.9 trillion trust industry is emerging as yet another threat to the world’s second largest economy.

After being restructured at least six times since its inception in 1979, the sector is facing another round of losses that Goldman Sachs Group Inc. analysts say may swell to the equivalent of $38 billion. Private wealth giant Zhongzhi Enterprise Group Co. and its affiliate Zhongrong International Trust Co. have halted payments on scores of high-yield investment products since last month, even sparking rare protests in Beijing.

Zhongzhi’s size — it manages more than 1 trillion yuan ($137 billion) — and its interconnectedness with wealthy investors, struggling developers and other financial institutions has spurred concern that troubles are beginning to cascade in the broader financial industry.

“There’s going to be a dangerous dance going on between the shadow banks and the banks themselves,” Andrew Collier, managing director of Orient Capital Research, said in a Bloomberg TV interview. “And that’s going to play out in the second half of this year and it’s going to be very messy.”

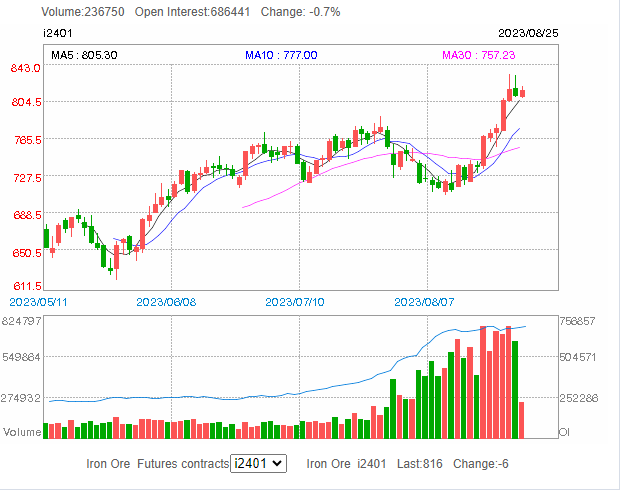

Meanwhile, the iron ore short squeeze appears to have flamed out:

“Even if China were to step up incremental policy support meaningfully now, there would still be a time lag for their effects to manifest,” Citi analysts said in a note.

Any pullback in iron ore prices may be limited, however, in the absence of clear and fresh directives from Chinese authorities to limit steel output this year under a policy aimed at curbing carbon emissions.

“The market is expected to continue to play games before the implementation of the production restriction policy,” Zhongzhou Futures analysts said in a not.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.