By Stephen Halmarick, CBA Chief Economist:

Key Points:

- The US FOMC has, as widely expected, resumed tightening and increased the Fed Funds target rate by 25bp to a 5.25%-5.5% range.

- Fed Chair Powell has signalled further tightening may be necessary, but that the Fed would be ‘data dependent.’

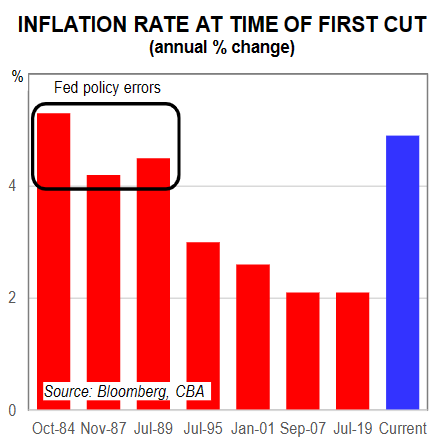

- We expect the Fed’s tightening cycle is now at an end. US economic growth is expected to slow significantly into 2024, with the FOMC expected to turn to a monetary policy easing cycle in early 2024.

Monetary policy decision:

The US Federal Open Market Committee (FOMC) voted to raise the Fed Funds rate by a further 25bp to 5.25%-5.5%.

The decision was unanimous. In a short statement announcing the rate hike, the FOMC noted that “recent indicators suggest that economic activity has been expanding at a moderate pace. Job gains have been robust in recent months, and the unemployment rate has remained low. Inflation remains elevated.”

They also added that “the US banking system is sound and resilient. Tighter credit conditions for households and businesses are likely to weigh on economic activity, hiring, and inflation. The extent of these effects remains uncertain. The Committee remains highly attentive to inflation risks.”

The FOMC’s forward guidance stated that “the Committee will continue to monitor the implications of incoming information for the economic outlook. The Committee would be prepared to adjust the stance of monetary policy as appropriate if risks emerge that could impede the attainment of the Committee’s goals.”

These comments were very similar to those published in June where the Fed paused their rate hike cycle.

Fed Chair press conference

At his post meeting press conference, Fed Chair Jay Powell stated that “looking ahead, we will continue to take a data dependent approach in determining the extent of additional policy firming that may be appropriate.”

The Chair seemed to be at pains to suggest that no decisions had yet been made about whether interest rates would need to rise in coming FOMC meetings, stating that “we’re going to be going meeting-by-meeting”.

He added that the Fed would be looking for moderate economic growth, improving inflation and for supply and demand to come into better balance, particularly in the labour market.

It was also interesting to note that Chair Powell stated that “what our eyes are telling us is policy has not been restrictive enough for long enough to have its full desired effect” and adding that “we intend to keep policy restrictive until we’re confident that inflation is coming down sustainably to our 2% target.”

Monetary policy outlook

Despite the Fed Chair’s policy guidance that more rates hikes could be needed, we see today’s rate hike from the FOMC as the last in this cycle.

The risk is, however, for further policy tightening as the Fed’s rate projections, ie. the dot plot, from the June meeting imply one further rate hike. Markets today are pricing in approx. a 23% chance, ie. 6bp, of a rate hike at the next FOMC meeting in early September.

As detailed in our recent global economic update note, we expect the US economy to enter a recession in the second half of 2023, partly in response to the FOMC’s restrictive monetary policy setting.

In that note our Head of International & Sustainable Economics, Joe Capurso, stated that “parts of the US economy are weakening in response to tight monetary policy, particularly housing. Housing permits have been decreasing since late 2021. Bank lending has stabilised since several small US banks collapsed in March. Household spending on durable goods has been stable since early 2021. However, household spending on services remains resilient. So too is the labour market. The pace of the expansion in employment costs is inconsistent with inflation returning to the FOMC’s 2%/yr inflation target. A recession is the price of returning inflation to target in our view.”

As the pace of economic growth in the US slows through the remainder of 2023 and inflation continues to moderate, we expect the FOMC to hold the Fed Funds rate steady and then in early 2024 turn its mind to policy easing.

Our base case is for monetary policy easing to get underway in Q124, taking the Fed Funds rate steadily down to 2.5%-2.75% at year-end 2024 and then lower to 2.0%-2.25% by mid-2025.