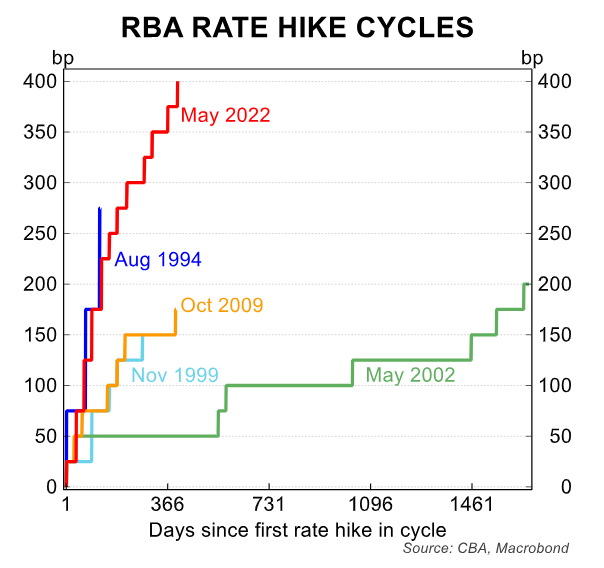

The Reserve Bank of Australia (RBA) has lifted the official cash rate by 4.0% in only 13 calendar months, which is the steepest and largest monetary tightening in history:

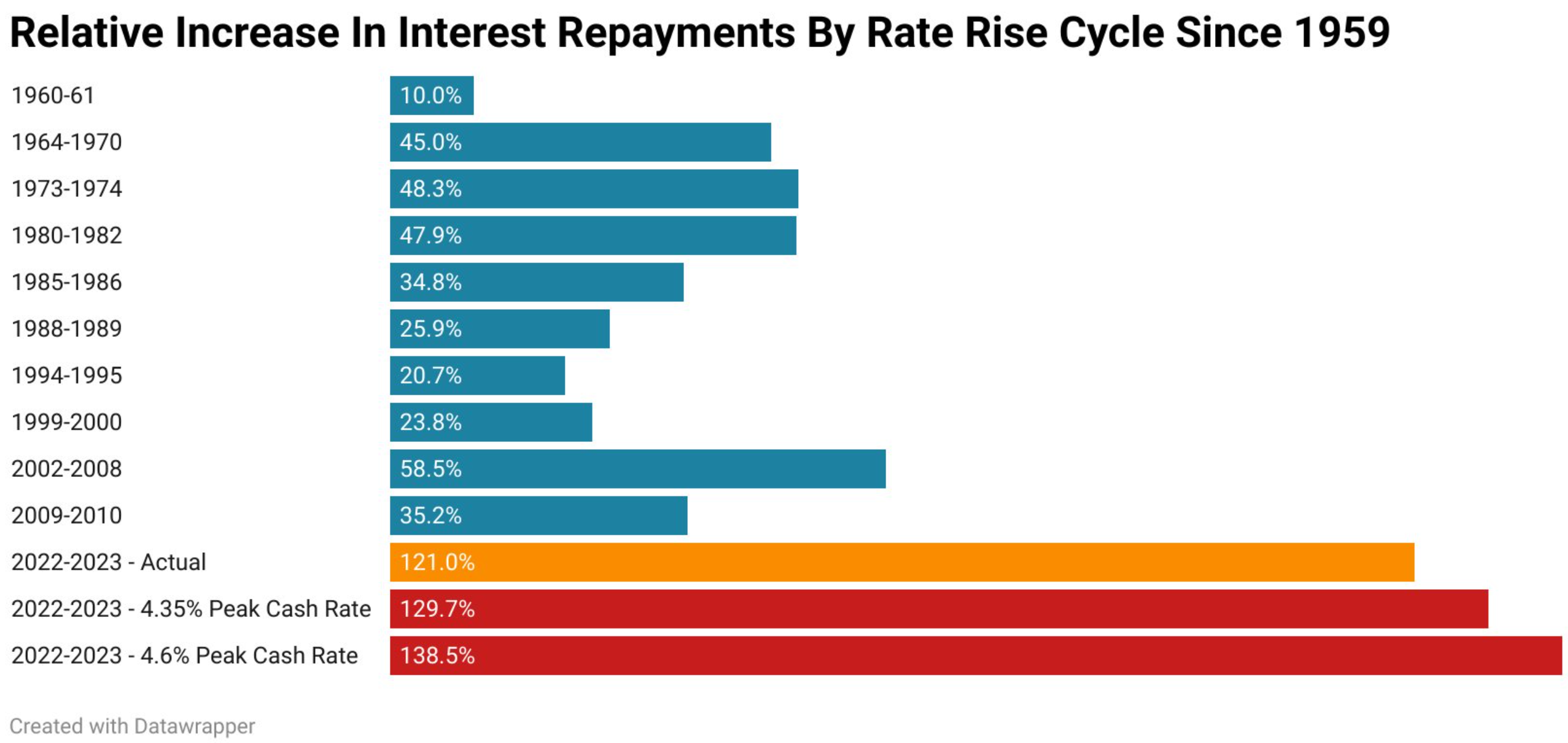

This has lifted mortgage interest repayments an unprecedented 121%, which will grow to 138.5% if the RBA hikes rates a further two times:

Source: Tarric Brooker

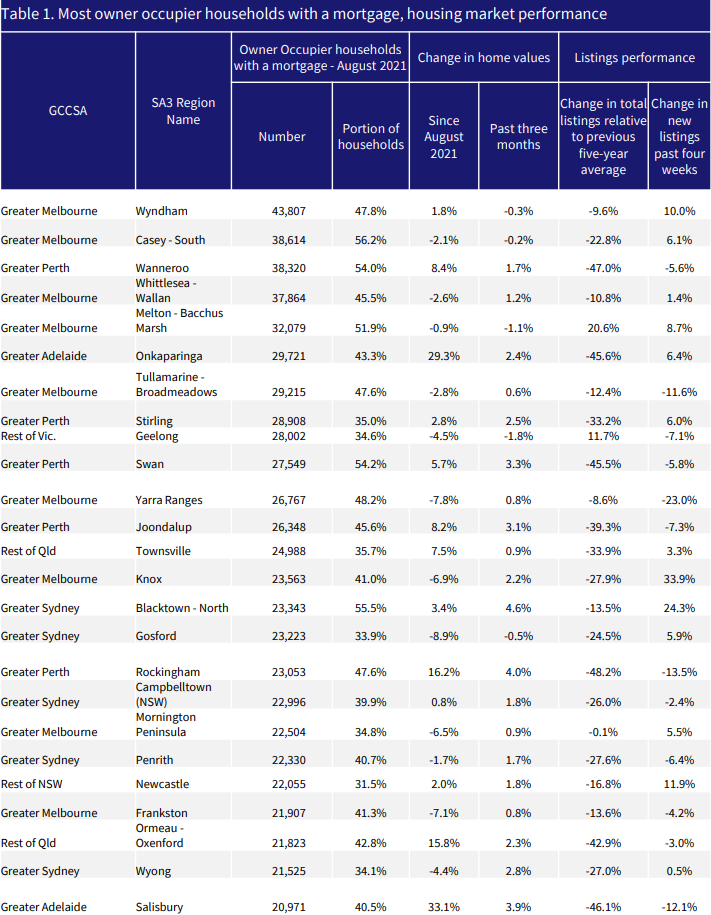

New Research from Eliza Owen at CoreLogic shows that the outer-suburban mortgage belts are most exposed by the RBA’s aggressive interest rate hikes.

“The number of mortgaged, owner occupier households are generally highest in outer regions of major cities, particularly Melbourne”, Owen notes.

“Of these 25 regions, nine are in Melbourne, five are in Perth and Sydney and two are in Adelaide. The remaining four are large regional centres, including Ormeau-Oxenford on the Gold Coast, Geelong, Newcastle and Townsville”.

“For markets in the capital city regions, there is an average distance to the city centre of about 34 km”.

You can view the table of the top 25 suburbs with the highest number of mortgaged households here.

Owen points out that average home values in these mortgage belts have risen by 3.1% since the 2021 Census, compared to national housing market growth of just 1.0% in the same period.

However, there is a large range in capital growth performance from 40.5% in Salisbury, to -8.9% in Gosford.

“Capital growth trends across these markets are an important consideration in the financial stability of the Australian housing market”, Owen notes.

“This is because in the event of a ‘forced sale’, growth in home values allows a seller to come away with some capital gain, or allows a mortgagee in possession to recuperate the entirety of debt on a property”.

“At this stage, most markets with a high volume of owner occupier mortgages do not exhibit capital growth trends that are alarmingly out of step with the national housing market. Indeed, some markets have had extraordinary capital gains since the onset of the pandemic, and since the Census snapshot”.

“However, it is noticeable that new listings volumes are climbing in some of these markets, where the national trend is seeing a seasonal slowdown. This could make it more difficult for recent buyers to make a capital gain if they are struggling to meet mortgage repayments”, Owen warns.

The financial pain is set to worsen across these mortgage belt suburbs.

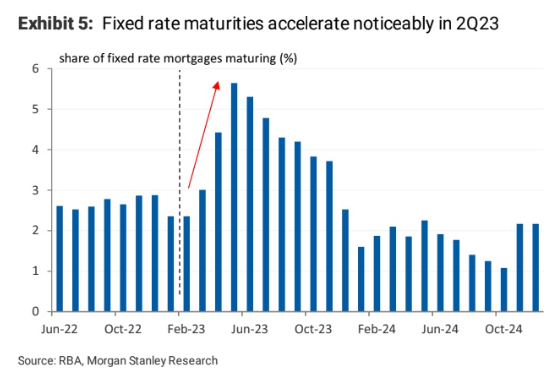

In addition to further interest rate hikes from the RBA, the bulk of cheap fixed-rate home loans taken out through the pandemic are expiring over the remainder of this year, which will expose more households to a spike in repayments:

We don’t know when the ‘tipping point’ for Australian mortgage holders will occur, if it hasn’t already.

But the RBA is playing with fire by continuing to lift rates at a time when monetary conditions are already tightening due to the fixed-rate mortgage cliff.

One upside is that most of these mortgage belt suburbs are popular among new migrants.

So, with net overseas migration running at record levels, home values will likely be supported.

Therefore, at least if mortgage holders are forced to sell, they won’t be in negative equity and will be able to walk away relatively cleanly.

{kind=link}