New data presented in CoreLogic’s Pain & Gain report shows that a growing number of Australians who purchased their home during the pandemic are opting to sell at a loss.

CoreLogic notes that “an increasing share of resales taking place in the March quarter have a relatively low hold period of less than two years”.

“The portion of resales with a hold period of less than two years in the March quarter was 8.4%, up from 6.6% in the March quarter of 2022, while the portion of loss-making resales with a hold period of less than two years has also increased to 12.4%, compared to 3.4% in the March quarter of 2022”.

“Such short selling times that involve sellers incurring a loss may be considered unusual, because hold periods typically increase during housing value downturns, as sellers try to avoid making a loss”.

“The implication may be that some sellers are choosing to incur a loss from resale in order to avoid particularly high mortgage payments in the current rate-hiking environment”.

Specifically, 5.5% of homes that were purchased less than a year ago were sold at a loss in the March quarter, compared with just 2% cent for the previous corresponding period.

Likewise, the proportion of homes that were sold at a loss after less than two years has tripled to 12.4%.

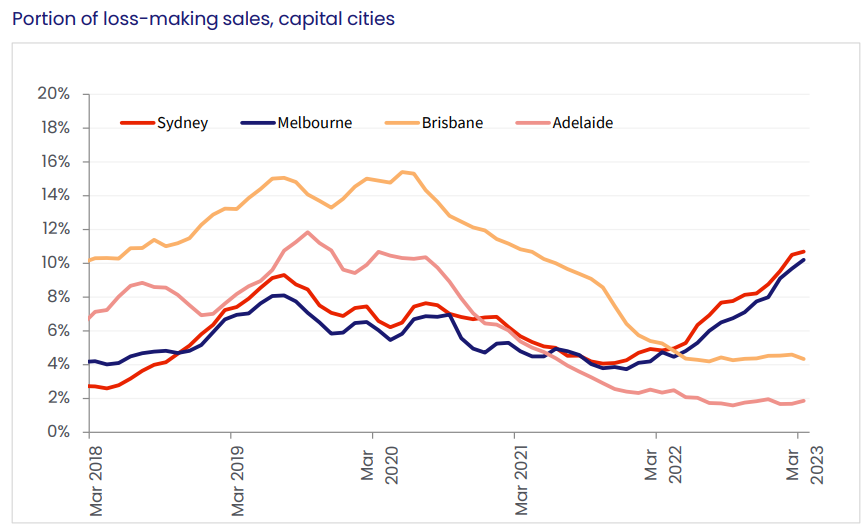

Interestingly, the proportion of loss-making sales has risen most sharply in Sydney and Melbourne:

CoreLogic believes the potential for further interest rises may prompt more people to sell their home for less than they paid for them:

“The data indicates that a higher portion of sellers have chosen to offload their property in a short space of time, despite reduced nominal gains, and a higher chance of making a nominal loss”.

“This could support the broader narrative that rising interest costs are prompting a higher level of sales, particularly through 2023, where mortgage holders rolling off fixed rate terms taken up in 2021 may be facing a sudden ‘sticker shock’ on mortgage repayments”.

“CoreLogic estimates that monthly variable home loan payments on a $500,000 loan have increased around $1,030 for owner occupiers, and $1,050 for investors between April 2022 and June this year”.

“While there is a lot that takes place between falling behind on mortgage repayments and the mortgagee taking possession of the home, some sellers may be looking to offload their property before reaching that stage”.

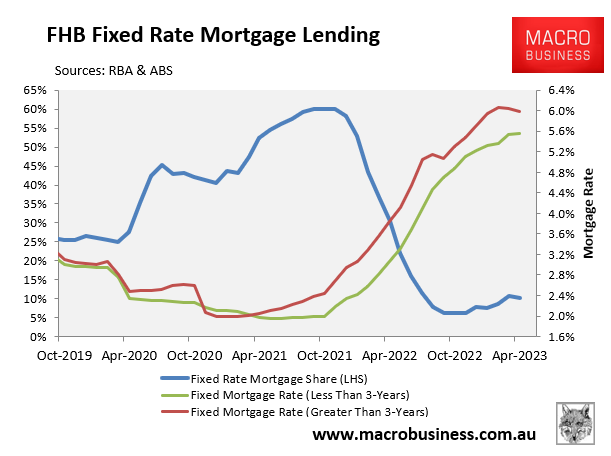

The situation is darkest for the large share of first home buyers that borrowed close to their maximum capacity on a cheap fixed rate of around 2%:

The majority of these fixed mortgages will expire over the remainder of 2023 and will reset to rates that are around three times higher.

Many recent first-time purchasers will then be confronted with the lethal combination of negative equity and negative cash flow.