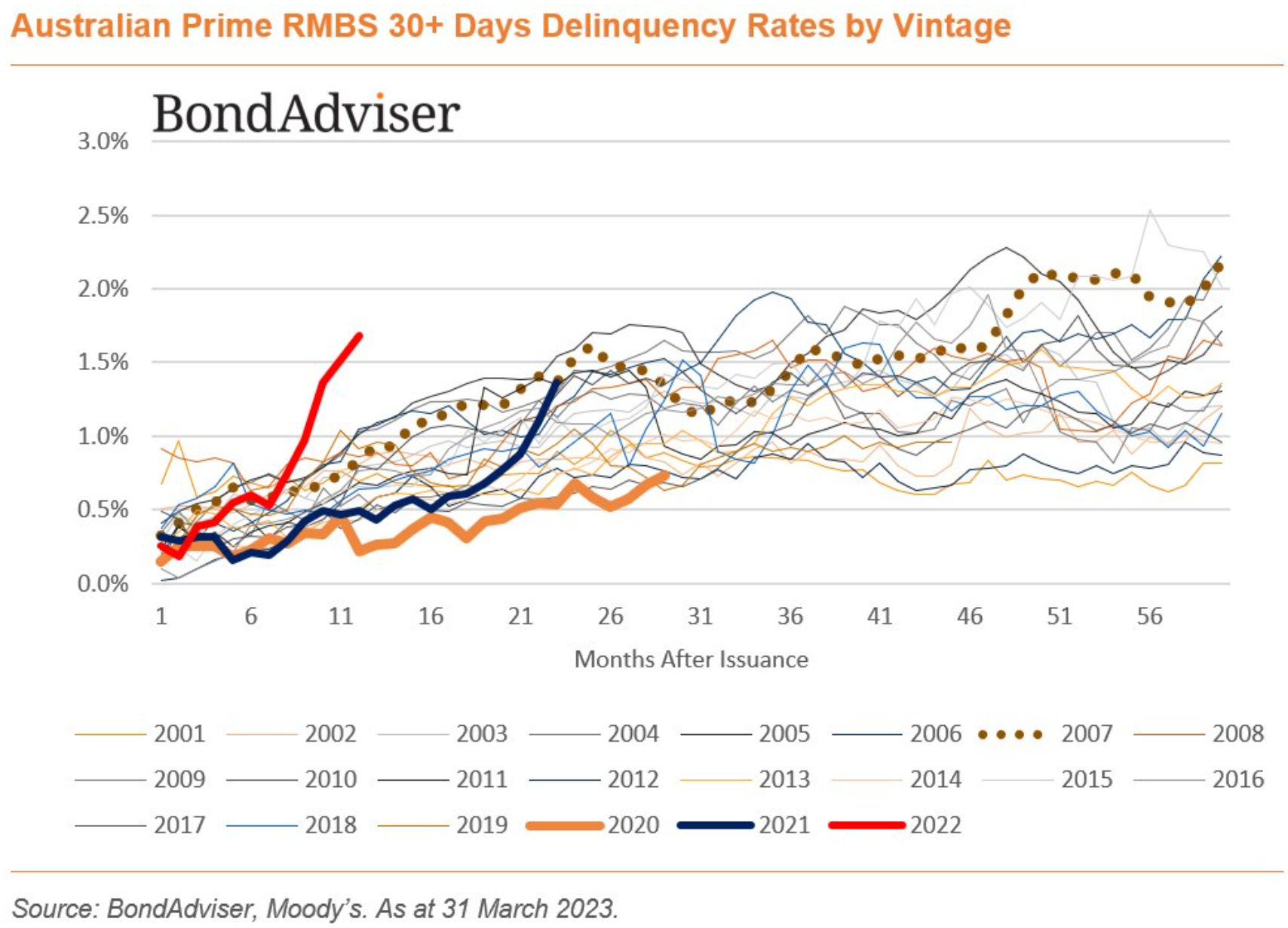

Earlier this month, Moody’s reported that 30-plus day arrears on 2022 vintage prime residential mortgage-backed securities (RMBS) had rocketed (red line below), with 2021 vintage mortgages also rising sharply (blue line below):

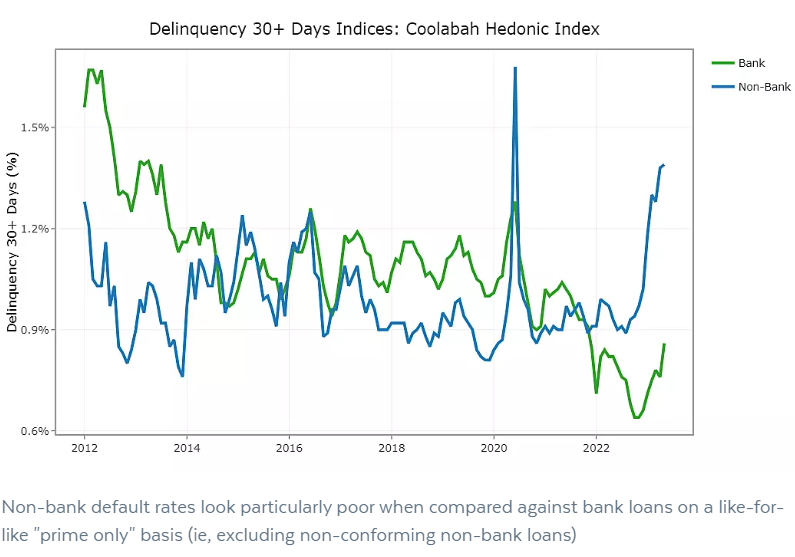

The team at Coolabah Capital shows similar trends.

They track delinquencies of 30 days or more on all Australian house loans made by both banks and unregulated non-banks, which are then securitised.

They then eliminate statistical biases from these data further using a unique hedonic regression technology which they pioneered in 2018.

Coolabah’s Chris Joye explains that “non-bank home loan delinquencies (blue line) have increased sharply from their lows in 2022”, whereas “bank delinquencies (green line) have risen only quite modestly”:

Source: Coolabah Capital

Joye also shows that “non-bank 30+ days arrears rates for prime loans have rocketed through the roof in the last six months (blue line) and are running at 3-5x the arrears rates that regulated banks report on their prime products”:

Coolabah Capital

Meanwhile, Lendi Group chief operating officer, Sebastian Watkins, has warned that a concerning numbers of households could find themselves in major financial stress if the RBA continues to lift interest rates.

With the RBA widely tipped to lift the official cash rate at least twice more to a peak of 4.6%, Lendi has expressed concern that two in five borrowers who have taken out a mortgage since 2021 could see their household budgets stretched to the limit if the banks pass on the two rate hikes in full.

The nation’s mortgage outlook is already “extremely worrying”, but will “get worse if the RBA continues to hike rates”, says Watkins.

“We could see alarming numbers of households in considerable financial stress”.

The lowest variable mortgage rate found in the market by Lendi was at 5.44%, and according to its study of home loan application data, two more rate hikes would imply that roughly 40% of borrowers who took out loans during or after 2021 would overshoot their monthly budget.

“This data accounts for the borrower’s wage and cost of lifestyle at the time of settlement, it paints an extremely grim picture of the strain rising rates is putting on Australians”, warned Watkins.

“It is likely many of these borrowers will be forced to make significant lifestyle alterations or need to consider selling assets to free up cash and service their mortgage payments”.

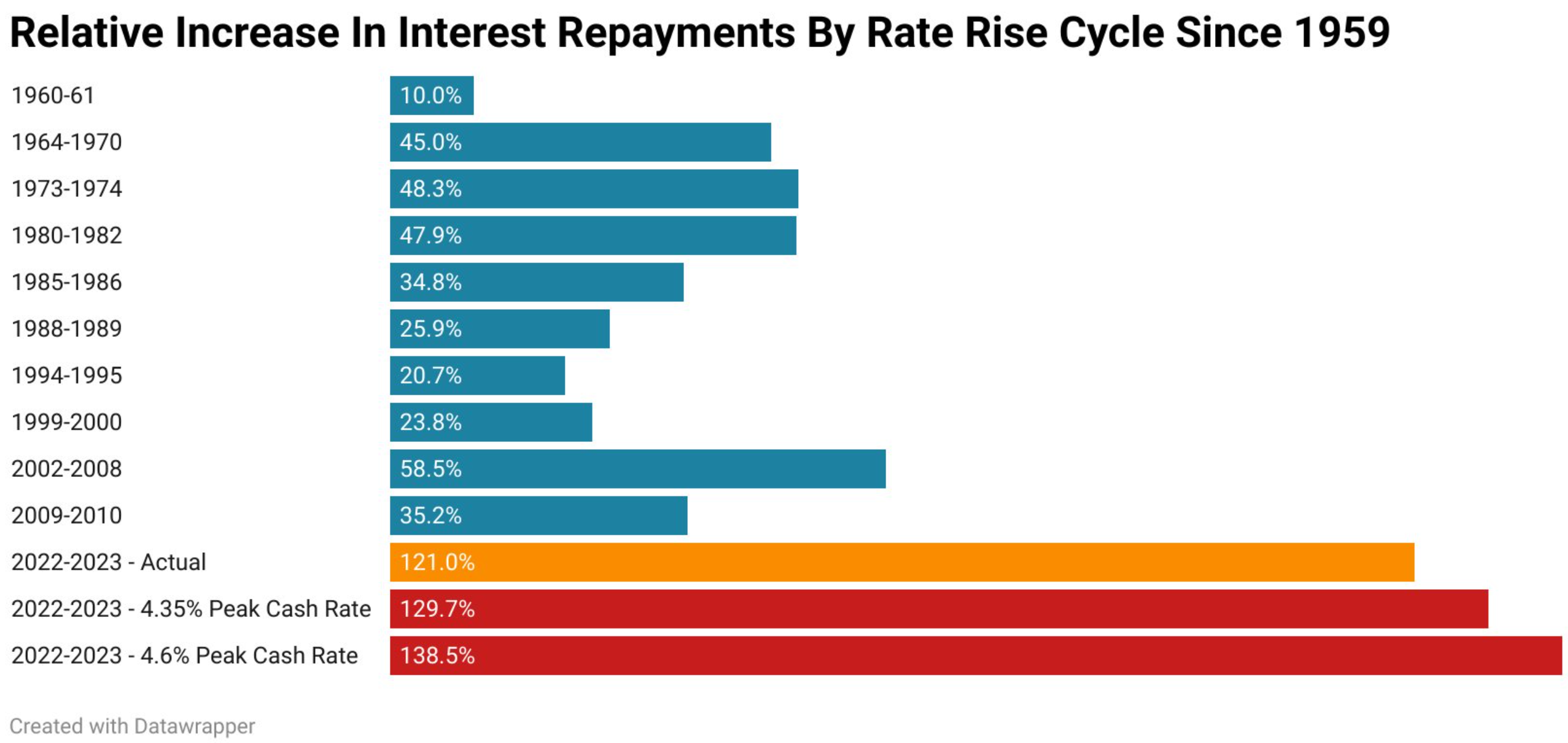

Independent Economist Tarric Brooker posted the below chart earlier this month illustrating the relative lift in interest repayments by rate tightening cycles since 1959:

Source: Tarric Brooker

Mortgage interest repayments have soared by 121% so far this cycle, dwarfing the second-highest 58.5% increase registered over the 2002 to 2008 cycle.

Worse, if the RBA was to hike two more times, then mortgage interest repayments will rise to 128.5%.

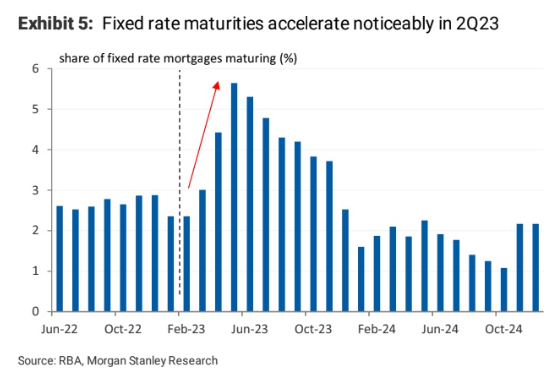

Remember, there are still nearly 500,000 fixed rate mortgages that will reset to variable over the remainder of this year:

These borrowers will reset from mortgage rates of around 2% to variable rates approaching 7% (higher if the RBA continues to hike).

As noted by Chris Joye, “this default cycle is only just beginning and likely to get a lot worse as the RBA continues to lift its cash rate”.

That is is putting it kindly.