Gareth Aird, head of Australian economics at CBA, believes the 2023 Federal Budget does not add to inflationary pressures in the economy.

Accordingly, the CBA has not changed its profile for interest rate profile.

Key Points:

- Our assessment is that the 2023 Commonwealth Budget does not add to inflationary pressures in the economy.

- As such, we have not changed our forecast profile for inflation or our call on the RBA.

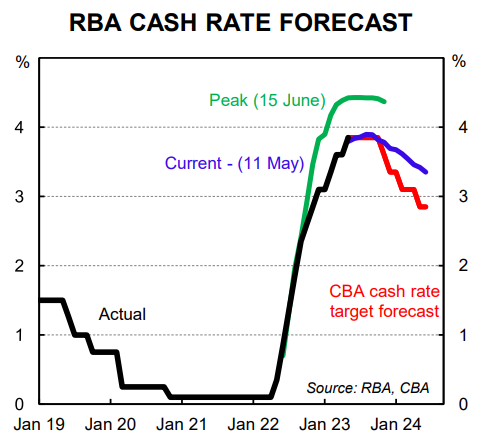

- Our central scenario puts the current 3.85% as the peak in the cash rate, while the near term risk sits with another rate hike.

- Despite the 2023 Budget’s modest and targeted ‘cost of living relief’, the budgets of many home borrowers and renters will be under considerable strain over the coming year.

- We continue to expect 50bp of rate cuts in Q4 23 and a further 75bp of easing in 2024 that would take the cash rate to 2.6% – a more neutral setting.

- The risk to the timing of the commencement of the easing cycle sits with the first cut arriving in Q1 24 rather than late 2023.

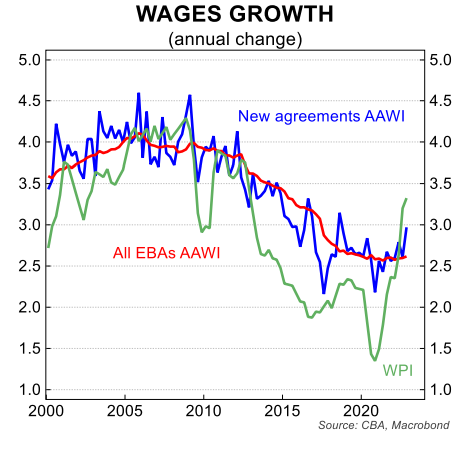

- The upcoming Fair Work Commission (FWC) decision on the national minimum wage will be critical to the outlook for wages growth and by extension inflation and the monetary policy outlook.

Overview

Fiscal policy has the capacity to shape the trajectory of aggregate demand and inflation. The massive fiscal expansion to assist households and businesses through the pandemic in both 2020 and 2021 went a long way to generating the surge in inflation over the past year.

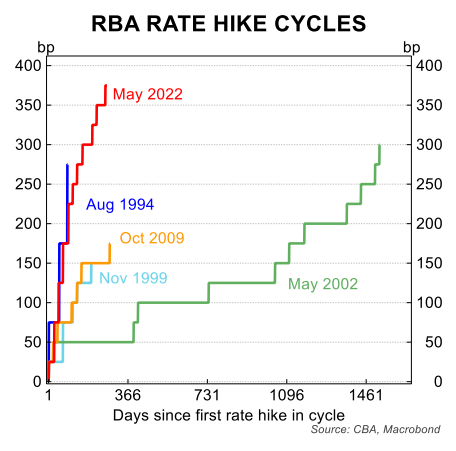

The RBA responded to the spike in inflation by lifting the cash rate by a whopping 375bp since May 2022.

The lagged impact of rate hikes are now slowing the economy and inflation is coming down. Directionally things are evolving in the desired way.

The role of a market economist when assessing the Budget is to look at it through the lens of what it means for the economic outlook.

The Budget almost always contains ‘winners’ and ‘losers’. And policy changes can redistribute income and wealth in the economy.

But financial market participants are almost entirely focussed on what the Budget means for the outlook for monetary policy.

On that score the economic backdrop somewhat complicated the Government’s objectives heading into the 2023 Budget. Inflation is higher than desired and monetary policy in our view sits in a deeply restrictive territory.

This combination is slowing the economy and squeezing household budgets.

The Government wants to help households, particularly those on low incomes. But the challenge for the Government presently is to assist households in the short run with ‘cost of living pressures’, while not adding to inflationary pressures in the economy.

Medium term structural fiscal reform was largely left for another day.

The current situation facing households was summarised neatly in RBA Governor Lowe’s Statement accompanying the May Board meeting. The Governor noted that, “while some households have substantial savings buffers, others are experiencing a painful squeeze on their finances” (our emphasis in bold).

The Government does not want to do anything that would cause interest rates to rise by more than otherwise as this would add additional stress to home borrower finances.

For many home borrowers the capacity to find additional money to meet higher mortgage repayments is limited.

From a political perspective rate hikes are unpopular. Indeed behind closed doors we suspect the Government would welcome interest rates coming down next year from what we deem is currently a deeply restrictive policy stance.

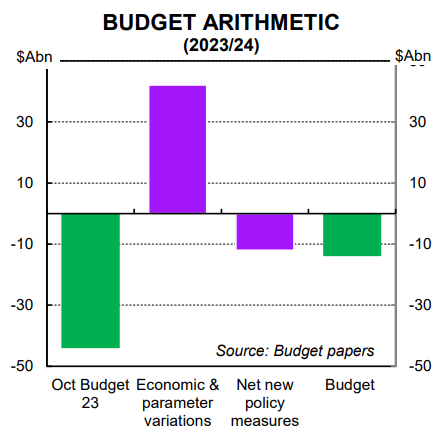

The Budget wasn’t inflationary

Personal income tax cuts and/or increased spending will generally be viewed as inflationary (i.e. they stimulate demand). Conversely an increase in personal income tax rates or a reduction in expenditure will be considered disinflationary.

The assessment of whether a budget is inflationary or not becomes more nuanced if some policies that provide financial assistance to households also limit the direct and measured impact on the CPI. That is what happened in the 2023 Budget.

Energy relief to households was a key policy in the 2023 Budget to provide cost of living relief to households. Reducing the cost of health care and medicines was another policy in the same vein.

According to the Government, retail electricity price increases in 2023/24 will be ~25ppts lower and retail gas price increases around 16ppts less than expected prior to the Government’s interventions.

Prices for both electricity and gas will still rise in the CPI. But the increase will be less as a result of the policies.

The Government’s Energy Price Relief Plan is expected to subtract 0.75ppts from headline inflation in 2023/24. Medicare bulk billing incentives along with childcare subsidies will also put downward pressure directly on measured inflation.

It can be argued that these packages free up some consumer cash flow to spend on other goods and services. And therefore the second round impacts of the package are inflationary. But we don’t subscribe to that view.

Inflation expectations are a driver of inflation over the medium term. And inflation expectation can be heavily influenced by actual inflation.

Lowering measured inflation in the short run at a time when there remains lingering concerns around inflation psychology makes a lot of sense. It is both smart politics and smart economics.

Many wage agreements and price outcomes are set with the level of actual inflation in mind. If measured inflation recedes more quickly it can dampen down the consumer and business expectation of entrenching price rises – a welcome outcome.

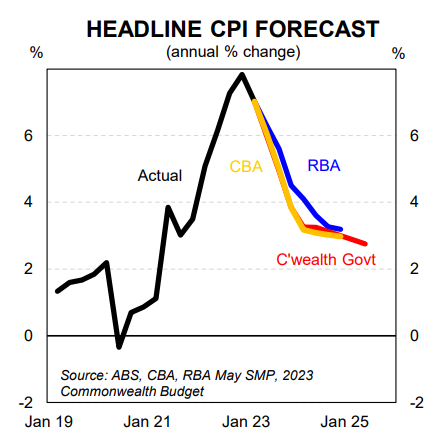

On that score we note the Government expects inflation to recede more quickly than the RBA’s latest forecasts in the May Statement on Monetary Policy.

Headline inflation is forecast to be 6.0%/yr in Q2 23 and 3.25% in Q2 24. In contrast the RBA forecast headline inflation to be 6.3% in Q2 23 and 3.6% in Q2 24.

Our profile for inflation is closer to the Government’s than the RBA’s (see below chart). Our point forecast for headline inflation in Q2 24 is 3.1%. The Government does not publish underlying inflation forecasts.

The other important consideration when judging the potential impact of the Budget on inflation is that the economy is anticipated to continue to slow.

The ‘official forecasting family’ of the Commonwealth Treasury and the RBA both expect below trend growth over the next two years and by extension a lift in the unemployment rate.

We agree. But we forecast economic growth to slow a little more quickly and for the unemployment rate to lift at a slightly faster pace.

In short, the lagged impact of the already delivered rate rises will see below-trend growth and an increase in the unemployment rate.

The Budget is simply providing some targeted relief to low income households to assist with the cost of living. But it’s not enough to shift the overall picture of a slowing economy.

As a result, we believe the direct short term benefit of lowering the measured rate of inflation offsets the notion that these subsidies will see second round inflationary impacts.

The outlook for the RBA

No change to our economic forecasts as a result of the 2023 Budget means no change to our RBA call.

Markets will continue to price the near term chance of another rate rise given the RBA retains a tightening bias and inflation is elevated. Therefore the risk in the near term sits with another rate increase.

But we expect the need for further tightening to dissipate from here. The economy will slow as the lagged impact of the already delivered rate rises further weighs on consumer spending and by extension inflation.

The RBA’s rapid rate hikes over the past year will have a big impact on the demand for goods and services in the economy and by extension price changes in H2 23 and 2024.

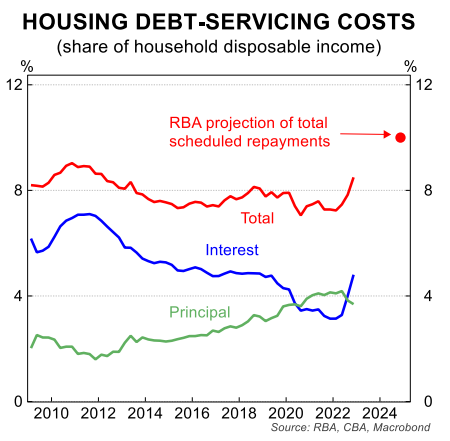

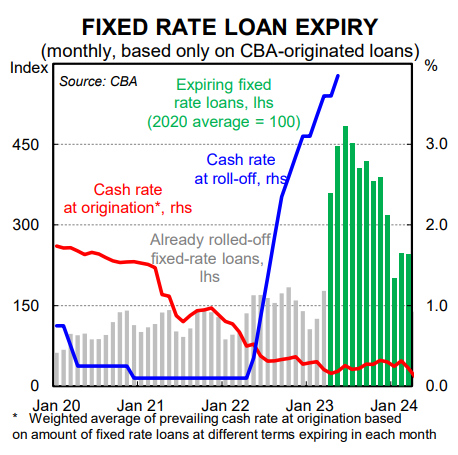

In addition, there is still organic tightening to come in the pipeline as the big fixed rate home loan rollover continues in 2023 and 2024.

The CBA fixed rate rollover steps up significantly from here. And there is generally a lag of a few months before home borrower cash flow is impacted by the step change of rolling off a fixed rate loan onto a higher floating rate mortgage.

The additional interest cost will be charged immediately. But the higher required repayment, which impacts home borrower cash flow, will not be upwardly adjusted for a few months. So the lagged impact of the fixed rate rollover will really bite in H2 23 and 2024.

The step change from ultra-low fixed rate home loans to significantly higher floating or fixed rate loans will drain the cash flows of many home borrowers and spending decisions will shift.

Real household consumption has a material probability of turning negative in coming months. As the economic data “catches up” to the changes underway in the economy, the case for rate cuts will strengthen.

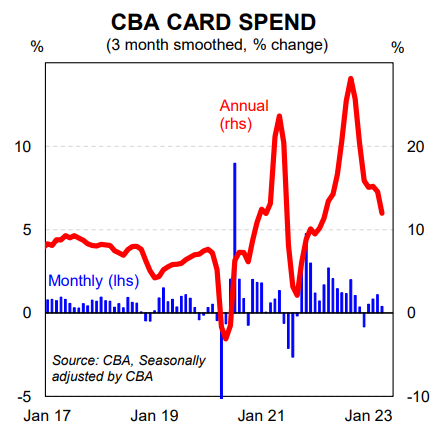

Our internal card spend data has slowed significantly so far in 2023 (latest to April – see below chart). Our data captures nominal spend on CBA credit and debit cards.

It is volatile month to month, even on a seasonally adjusted basis. But the trend is clear. The nominal smoothed monthly change so far in 2023 is tracking at a similar growth rate to pre-pandemic.

But inflation was ~1¾%/yr in the years prior to the pandemic and real household consumption was soft. In addition population growth has recently surged.

An above average number of new migrants that settle in Australia open a CBA bank account (we estimate around ~45% of new long term arrivals into Australia open a CBA bank account).

So real consumption per capita is likely falling at a faster rate than both the RBA and Treasury anticipate.

This supports our view that the unemployment rate will rise more quickly than the RBA anticipates.

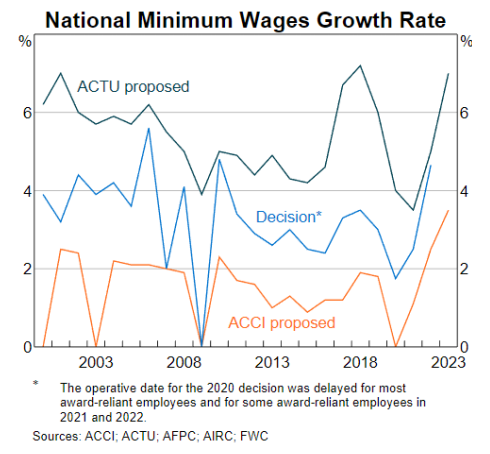

A key risk to our RBA call is the upcoming Fair Work Commission (FWC) decision on the national minimum wage.

Recall that last year workers on awards earning more than $A869 a week received a 4.6% increase but those below $A869 received an increase of $A40 a week, which equated to a pay rise of between 4.6-5.2%.

In the 2023 Budget it was noted that, “the Government has again recommended that the FWC ensures the real wages of Australia’s low-paid workers do not go backwards.”

But there were no specifics on whether the Government was referring to a recommendation to an award wage increase in line with actual inflation or forecast inflation.

Given inflation is coming down we believe that statement in the Budget was left sufficiently vague so that forecast inflation plays a role in the upcoming FWC decision.

Our working assumption is that the FWC hands down a lift in the national minimum wage similar to last year. A bigger increase could see us tweak our RBA call.

We see 3.85% as the peak in the cash rate this cycle. We continue to look for rate cuts in late 2023 as we believe inflation will fall more quickly than the RBA currently anticipates. And that the unemployment rate will lift more sharply.

We do not think the annual rate of inflation needs to return to target before the RBA cuts the cash rate.

Rather we think a six month annualised pace of inflation that is close to target and on a downward trend would be sufficient for the Board to ease policy given inflation is a lagging indicator.

The RBA will not hint at policy easing over the months ahead given they will retain a hiking bias. But central banks pivot quickly when the data makes the case.

Finally we note that money markets have started to support our long held view that an easing cycle could commence in late 2023 (see below chart).

Markets are forward looking and are moving in the direction that is increasingly agreeable with our base case.