The legislated stage-three personal income tax cuts are estimated to have a nominal cost to the federal budget of about $18 billion a year when they take effect in mid-2024.

However, the Australian National University’s research suggests the tax package’s real cost to the budget will be around $6 billion a year, when factors such as inflation and ‘bracket creep’ are taken into account.

The stage-three cuts are estimated to cost $250 million over a decade, but ANU economist Ben Phillips says this is “overblown” as it does not take into account bracket creep or the impact of the first two tranches of tax cuts.

“[The cost] doesn’t take into account bracket creep and it’s a bit selective to just look at stage three because it doesn’t take into account stage one and two”, said Philips who is a member of the government’s Economic Inclusion Advisory Committee which recommended bigger increases in welfare payments.

“Obviously high-income earners are paying a lot more tax, but it is slightly regressive and does slightly increase inequality”.

“But I don’t think there is $250 billion of surplus funds that the treasurer can dip his hand into and spend”.

The stage three income tax cuts are expected to temporarily reduce real tax per capita to $15,926 in 2024-25, which is greater than pre-COVID levels, before gradually rising back to $26,000 in 2025-26.

Australia has a relatively low overall tax take by OECD standards, but a very high reliance on personal income taxes.

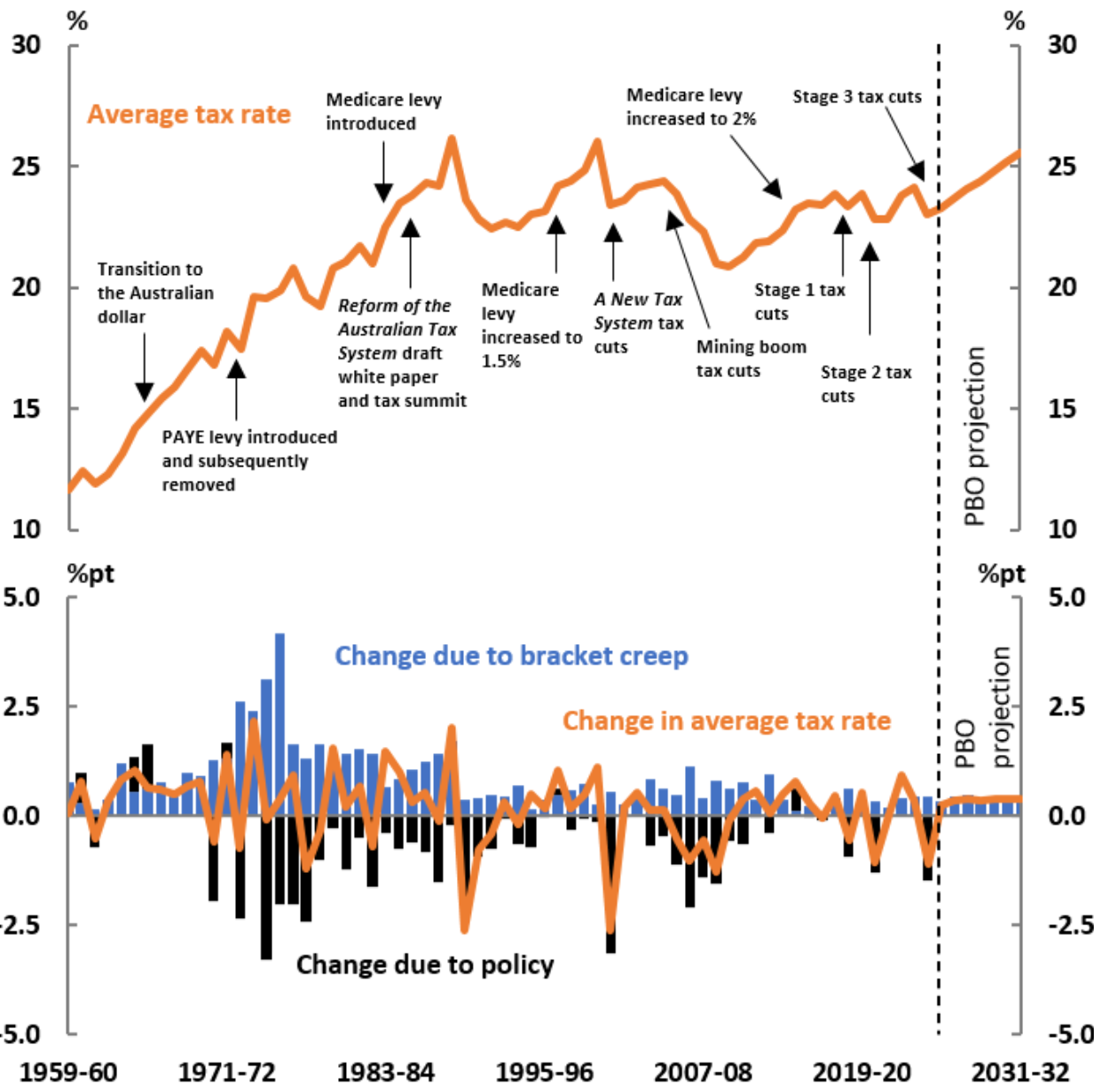

Indeed, Australia’s average tax rate on income will increase to an incredibly high level even if the Stage 3 tax cuts do take place:

Personally, I would prefer to see income tax brackets indexed to inflation to stop ‘bracket creep’, while at the same time embarking on comprehensive tax reform that:

- replaces less efficient and inequitable sources of tax with land/resource taxes, as well as raises and/or expands the GST; and

- closes costly and inequitable tax loopholes.

Relying on never-ending increases in personal income tax through bracket creep, as the labour force shrinks through population ageing and the share of retirees climbs, is neither efficient, equitable, nor sustainable in the long run.