And it is going to get worse before it gets worse with US and European slowdowns ahead. Pantheon with the note.

Caixin PMI points to Chinese private sector manufacturing activity stalling in March

Today’s set of PMIs point to a risk of China’s recovery losing momentum, while dismal global demand weighs on growth in north-east Asia. China’s Caixin manufacturing index slipped 1.6pt to 50.0 in March, contrasting with the official PMI reading at 51.9. We think this points to a multi-speed recovery, as the Caixin index is more weighted towards light industries and private sector firms.

Advertisement

The relatively poor performance of the Caixin index is similar to the official PMI’s small and medium-sized firm indexes. The small firm index dropped 0.8pt to 50.4, while the medium-sized index fell 1.7pt to 50.3. By contrast, the large firm index inched down only 0.1pt to 53.6. This makes sense as private sector firms are probably on average are smaller than SOEs.

Advertisement

Demand and supply fell in the Caixin PMI. Overall new orders fell 2.3pt to 50.6, export new orders plunged 3.2pt to 49.0, while output decreased 2.7pt to 50.6. Domestic demand is holding up better than global demand, the same picture as in the official PMI. Price pressures are subsiding. Input prices dropped 1.8pt to 50.0, while output prices edged down 0.3pt to 49.9. China is likely to export disinflation, not inflation, to the world this year.

Chinese policymakers are unlikely to shift their overall policy stance in response to the signs of growth momentum waning in certain sectors of the economy. Firms are still optmistic, with the Caixin future output reading slipping 1.5pt to a still high 60.0, the second-highest reading since April 2021.

Advertisement

Chinese policymakers will probably be monitoring the data in the rest of H1 to assess if strong growth in diverse services sectors is generating enough jobs to support the consumption rebound, and if buoyant infrastructure and manufacturing investment will drive industrial output. If the H1 data suggest a significant slippage in domestic demand, China will be poised to add support in H2.

Advertisement

Korean PMI indicates weakness at home and overseas

Advertisement

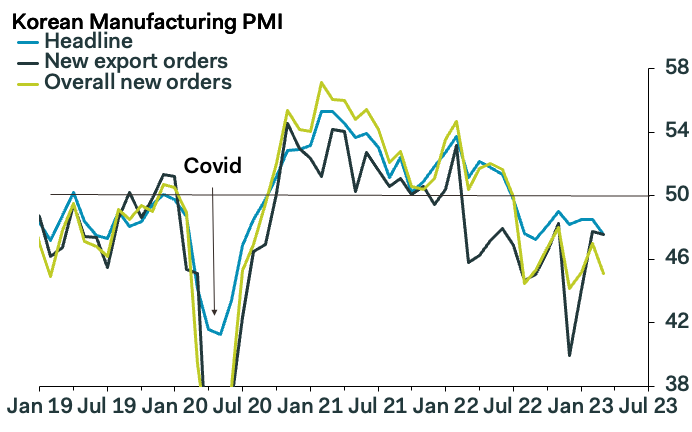

Korea’s headline manufacturing PMI fell 1.0pt to 47.6 in March, the ninth straight month below 50. Supply and demand both slipped, amid signs of weakness at home and abroad. Overall new orders declined 1.9pt to 45.1, new export orders edged down 0.2 pt to 47.6, while output dipped 0.6pt to 47.2.

We see nothing in the Korean data that is likely to shift the BoK’s worries about Korea’s growth output. As a result, the Bank is likely to keep the policy rate on hold for the rest of the year, expecting elevated consumer inflation to slow gradually. The BoK is likely to maintain a downbeat prognosis for the near-term growth outlook in light of the additional stress from the international banking crises.

Advertisement

Japan’s PMI and Tankan survey concur that business conditions are miserable

Advertisement

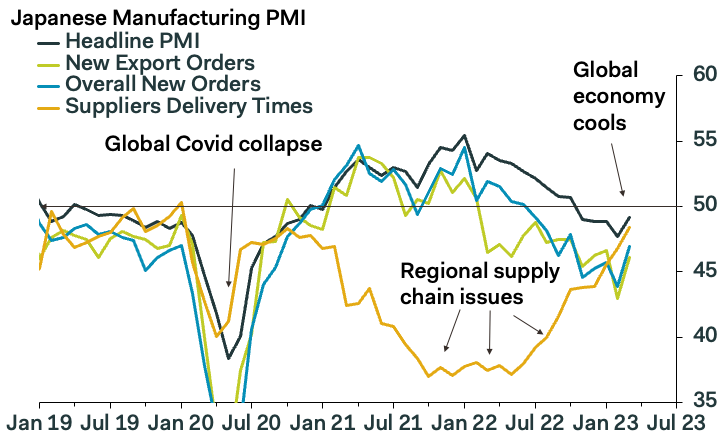

Japan’s headline final manufacturing PMI rose 1.5pt to 49.2, but this was still below 50 for the sixth consecutive month, indicating a decline in activity. The demand and supply readings were again much worse than the headline index, though improving from February. Overall new orders rose 3.0pt to 46.9, new export orders increased 3.1pt to 46.1, while output climbed 3.1pt to 48.4 in March.

Advertisement

Price pressures remain severe for Japanese manufacturers, as a result of higher import costs over the last few years. Input prices dipped 0.6pt to 67.0 in March, while output prices edged up 0.4pt to 57.5.

We think that incoming BoJ governor, Kazuo Ueda, is likely to keep easy monetary policy settings on hold at his first policy meeting on April 28. The manufacturing PMI indicates continued activity decline, while the Tokyo headline CPI edged down 0.2pp to 3.3% y/y in March, on the back of government energy subsidies that took effect in February. The gloomy global outlook probably will drag on Japanese growth, while China’s medium-paced recovery is providing little offset for now.

Advertisement

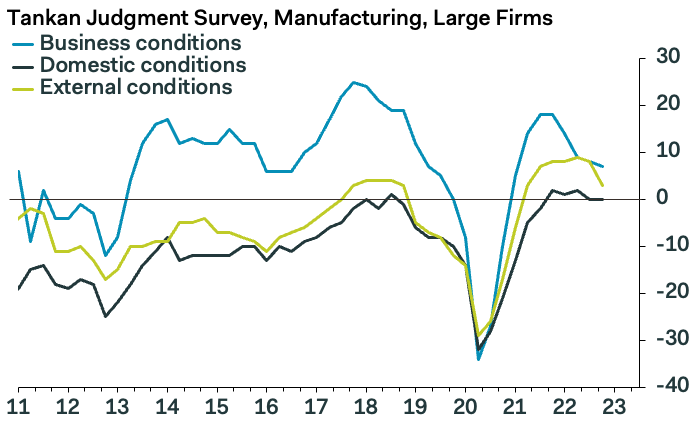

The headline Tankan large-firm business conditions index dived 6pt to 1 in Q1 2023, the lowest reading since Q4 2020. Domestic demand and supply conditions dropped 4pt to -4, while overseas demand and supply conditions fell 3pt to 0.

Advertisement

Large manufacturers are particularly pessimistic about future domestic business conditions, with the Q2 forecast deteriorating 3pts to -5 from the Q1 forecast. Meanwhile, the overseas business conditions Q2 forecast dips 2pt to 0. With the dismal outlook for future business conditions, large manufacturers have curbed their annual projection for fixed investment to 5.8% y/y in Q1 2023, down from 21.1% in Q4 2022 and the lowest reading since Q1 2021.

The Tankan survey highlights Japan’s stagflation and the BoJ’s longer-term policy dilemma. The large manufacturer employment reading was unchanged, at a miserable -14, in Q1, the eighth straight quarter of negative readings. The large non-manufacturing employment reading has been negative since 2011.

Advertisement

But the Tankan survey suggests that elevated inflation expectations are becoming entrenched. The survey reports that firms expect inflation at 2.8% a year from now, only gradually slowing to 2.3% three years from now and 2.1% five years from now. This policy dilemma highlights the need for incoming Governor Ueda to rethink the Bank’s conceptual framework over the longer term. But for this year, the Bank probably will maintain loose policy to support the feeble economy, especially with headline inflation cooling.

Advertisement