Westpac with the note. I agree. The Chinese rebound is consumer not construction-led. Moreover, unlike Westpac, I see infrastructure investment also falling.

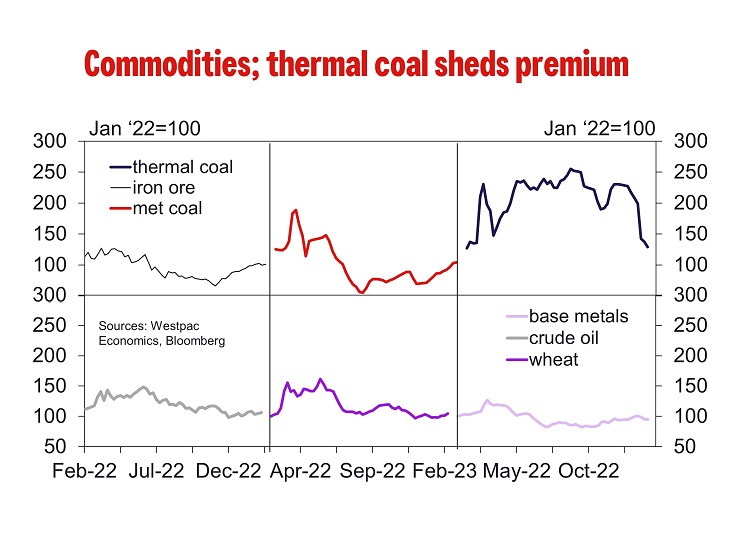

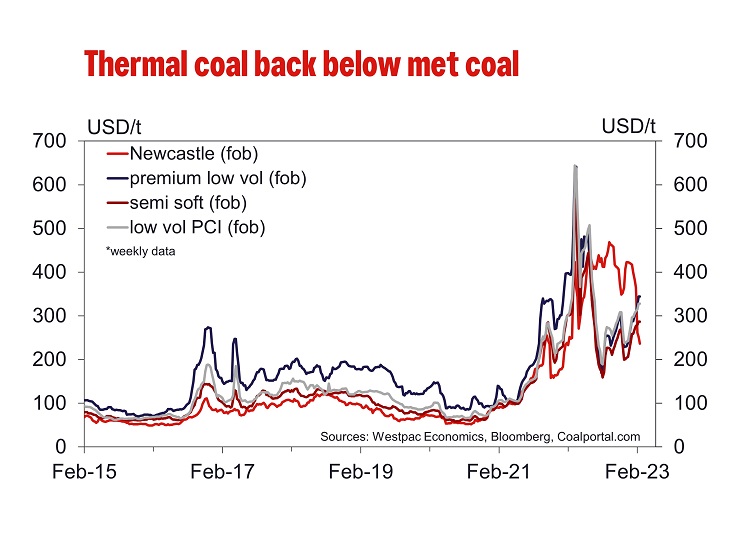

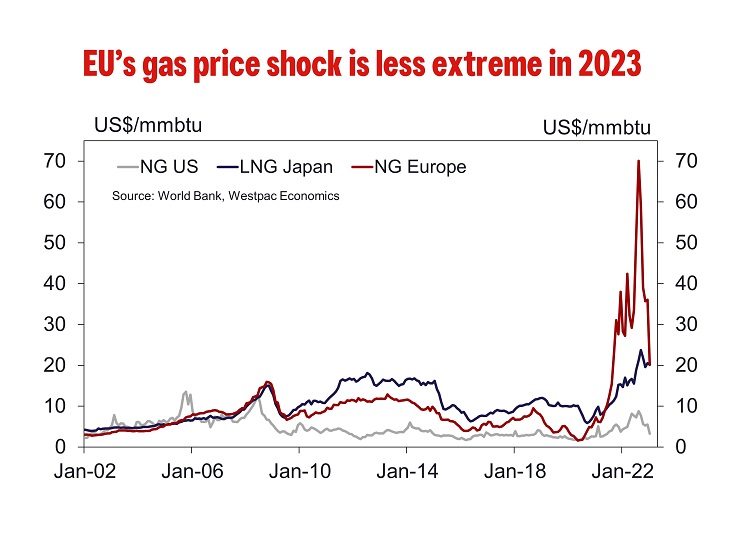

Since our last Commodities Update in mid-December commodities have continued their volatile ride. Since December 14th, iron ore rallied 13% to US$125/t which is less than half of what happened to met coal, which surged almost 50% to US$344/t while thermal coal, which was in a very unusual position of trading at a premium to met coal, collapsed 43% to US$240/t. Meanwhile, with Russia announcing a cut in production, crude oil had a last minute rally to US$85/bbl, an 8% lift since our last report. Gas prices have been easing around the world due to a mild winter reducing demand in the northern hemisphere with LNG landed in Japan easing 4% to US$18.80/mmbtu while gold has lifted 4% to US$1,879/oz. As a group, base metals have been flat but individual metals more mixed; copper rallying 5% to US$8,875/t, aluminium flat and the rest moderating (nickel -4% to US$27,852/oz, zinc -6% to US$3,085/t and lead -5% to US$2,089/t).

Commodities received some support from a depreciating US dollar but more recently, stronger than expected economic activity, while positive for near term demand, has increased fears of tighter than expected financial conditions resulting in slower growth that would accelerate an unfolding disinflationary trend. The sudden shock ending of China’s COVID-zero policies left commodities in limbo until positive anecdotes regarding consumer demand around Lunar New Year started to put out a more positive tone. Chinese pig iron and crude steel production slowed as we neared year-end but sentiment improved as we cleared Lunar New Year.

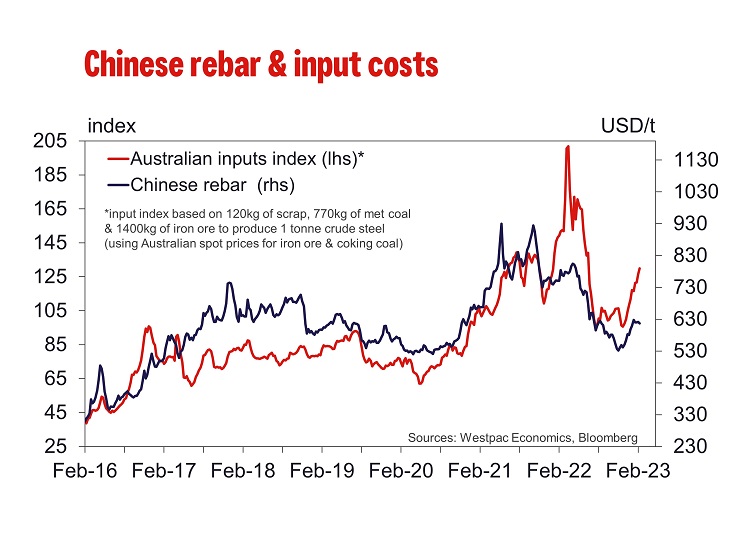

We have a gradual easing in the iron ore profile through 2023 to US$100/t by year-end, up from the US$90/t in our December publication. Chinese demand is expected to be broadly flat with the weakness in China’s property market offset by a pick-up in infrastructure. Meanwhile, there is still an expectation that supply is set to lift from Australia and India, with steel scrap also becoming increasingly easy to source. Chinese data for December supports our long-held view that China’s economy is well-positioned to not only rebound from COVID-zero, but also to grow strongly into the medium-term. We expect it to average growth of 5% or more through 2022 to 2024 and likely beyond. Therefore, the key risk to our cautious view is a stronger than expected recovery in China and in the Chinese property market in particular. There was some improvement in new home sales and the secondary market before the Lunar New Year but, for now, it remains consistent with our cautious view. We also note that Chinese re-bar spreads to iron ore are still depressed while ore inventories at Chinese ports have started to lift. In addition demand for ore from the rest of the world remains weak while iron ore shipments from Australia have been solid so far this year (albeit with some softening in shipments from South Africa and Brazil).

WoodMac recently published its annual review of iron ore projects reporting that the number of active projects had increased from 85 in 2021 to 115 in 2022. Our review of WoodMac’s data suggests there is the potential for around 300mt of additional iron ore supply to come online over the next 5 years with a bit more than 100mt from the majors, 35mt from the smaller Australian miners, 40mt from the Brazilian junior minors, 110mt from Africa (mainly Simandou) and something around 10mt from the rest. The data set also includes a host of other projects (worth around 940mt) at early the stages of development with financing and other approvals still to come. These projects also tend to be at the higher cost end, are capital intensive and/or geographically challenging.

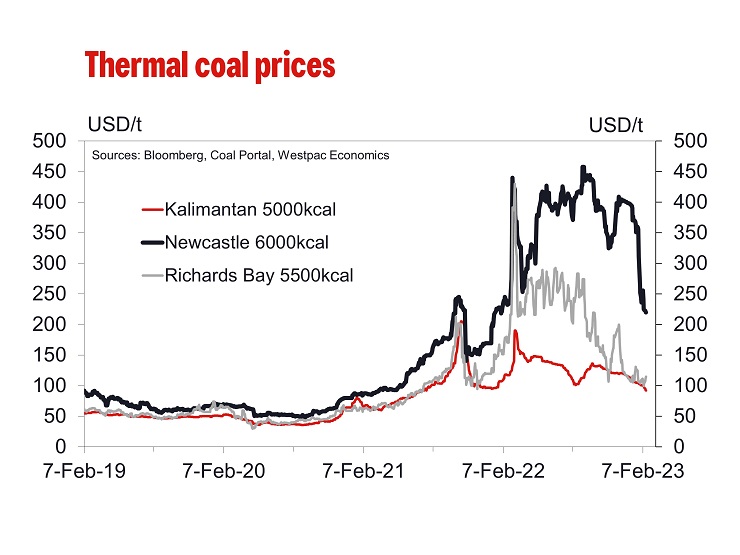

Falling European gas prices put significant pressure on thermal coal prices even though coal supply remains disrupted. Newcastle 6000kcal prices fell significantly with spot down to around US$250/t compared to around $400/t in December. The rapid correction in thermal coal prices was driven by a milder than expected northern hemisphere winter resulting in lower natural gas prices and soft demand in the Atlantic coal market. Despite earlier fears, European gas inventories remain high at around 70% of capacity. Globally, coal shipments are up 12% year to date so far this year but high-CV coal producing regions are still struggling; Australia down 10%, Colombia -30% and South Africa -11%. The additional supply is coming from Indonesia (+59% year to date) and North America (+33% year to date). This should see the premium for Newcastle coal to other grades/suppliers continue to narrow towards the end of the northern hemisphere winter. However, we still expect thermal coal prices to remain elevated compared to history over the next two years due to ongoing supply constraints; thermal coal holding at US$200/t at end-2023 and US$175 at end-2024.

Contrast the collapse of thermal coal with the rally in met coal. Prices are up almost 50% from mid December amid improving sentiment from China, although the increase in PCI and semi soft coals were a bit less at around +40% as falling thermal coal would have been a bit of a drag on the lower grades of met coal. Wet and stormy conditions continue to feature along the Australian east coast, particularly in Queensland, presenting an ongoing near-term supply risk. We are forecasting met coal prices to hold around US$300/t through 2023 ending the year at US$280/t due to support from rising demand from China. Australia’s first coal shipment after more than two years of an unofficial ban reached China’s southern Guangdong Province in early February. While supply remains disrupted, the return of the Chinese market is a clear upside risk for met coal.

In the US, gas prices remain stuck at under US$3/mmbtu, a clear signal for producers to dial back drilling new wells and for power producers to maximise natural gas burn at the expense of coal. Prices reflect a mild winter along with an explosion at the Freeport LNG Terminal that has seen a loss of export demand. Crude oil prices had been under pressure in December as demand risk emerged but just as demand appeared to firm a bit in early 2023, Russia announced that it would cut oil production by 500k bpd, around 5% of output, in March which was positioned as a response to the West’s imposed price caps on Russian oil and oil products.

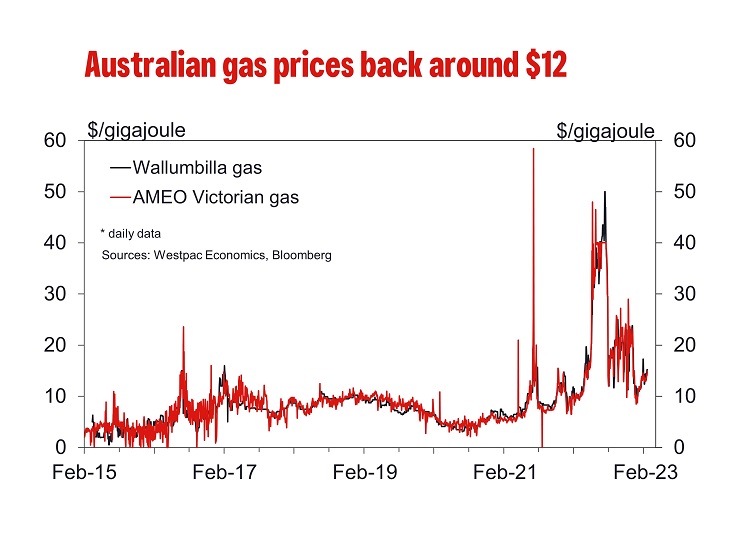

Along with weaker global prices, the Australian governent’s imposition of a price cap on Australian domestic gas of $12/gigajoule has seen local gas prices collapse to under $15/gigajoule and trade around a $12 floor. This has had a very real impact on our thinking for the evolution of Australian inflation through 2023 and into 2024 while reducing some, but not all of the fear, of the cost squeeze Australian industry is facing.