More are waking up to the reality of a different Chinese recovery. Barclays is the latest.

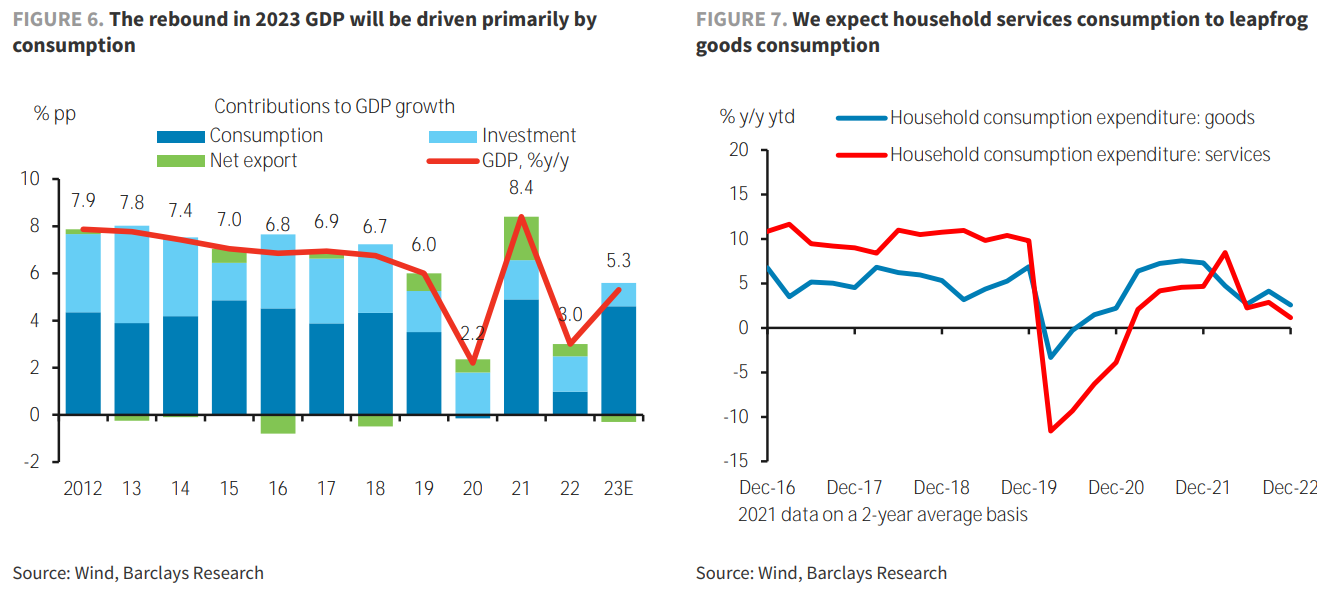

We raised our 2023 growth forecast to 5.3% on a quicker-than-expected revival of services activity. Our three-sector services nowcasting model suggests monthly GDP likely increased to 3% y/y in January. We also raised our full-year 2023 CPI inflation forecast to 2.5%, with inflation likely to exceed 3% in Q4.

Lunar New Year holiday data, the January PMI, and daily travel, transportation and recreation indicators point to a quicker-than-expected revival of services activity at the start of the year (A good start for 2023, 4 February 2023). We raised our Q1 GDP growth forecast to 5% q/q saar from 2.8%, given a stronger-than-expected recovery in services improved sentiment as herd immunity was likely reached in mid-January. Our quarterly profile for the rest of the year is unchanged at 7% q/q saar in Q2 and 4.7% in H2. We expect the pace of recovery to strengthen further in Q2 on improving infrastructure investment and a gradual recovery in the housing market, before normalising in H2.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.