Mortgage refinancing is very popular at the present time, but research conducted by brokers and analyst Carlos Cacho at investment firm Jarden suggests that many recent borrowers who took out loans with low deposits at the peak of the housing market may struggle to meet the criteria needed to change banks.

The combination of soaring mortgage rates and falling house prices (negative equity) is impeding borrowers’ ability to refinance because they no longer meet borrower stress tests, thereby trapping them in expensive mortgages that they are struggling to repay.

Falling house prices are also expected to push many loan-to-valuation ratios (LVR) above the 80% threshold at which new borrowers must often pay mortgage insurance.

Carlos Cacho suggests that there could be hundreds of thousands of what it refers to as “mortgage prisoners”, and that the banks could benefit from the growing number of them, as it would mean reduced competition:

Cacho estimated 10 to 15 per cent of outstanding home loans could be stuck with their respective lenders, with first home buyers who bought near the peak in house prices particularly exposed to the risk.

“There’s probably $200 billion to $300 billion of mortgages which are going to face difficulties refinancing,” Cacho said.

“Realistically, most of the people who are going to face difficulties are going to be people who originated their loans in the last two years.

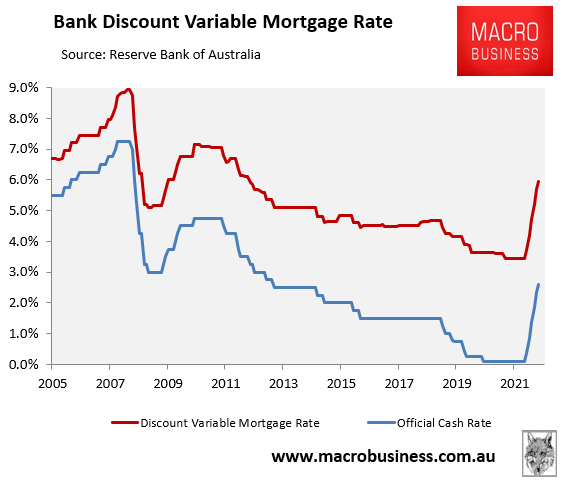

Australian dwelling values has already fallen 5.5% from their peak, whereas Australia’s average discount variable mortgage rate has climb to 5.95%, which is way above the April pre-tightening level of 3.45% and the highest since September 2012:

Variable mortgage rates soar.

Falling house prices and soaring mortgage rates are a toxic combination for those borrowers that extended themselves to enter the housing market last year near the peak. Many of these borrowers will now be in negative equity and won’t be able to refinance because they no longer meet lender serviceability tests. They will effectively be mortgage prisoners.

Whether the situation deteriorates depends on what the Reserve Bank of Australia (RBA) does with interest rates. If it continues to hike, then house prices will fall harder and mortgage serviceability tests will tighten. In turn, more borrowers will become “mortgage prisoners”.

The RBA last week chose to return to normal operations and hiked by only 0.25%. This suggested that it is approaching the end of its rate tightening cycle.

That said, the RBA did state that “the Board expects to increase interest rates further over the period ahead”, suggesting a few more 0.25% hikes could arrive if data permits.

Nevertheless, the hawkish forecasts of Westpac, Morgan Stanley and the bond market now seem unlikely. We instead seem to be approaching the end of the current rate tightening cycle, which limits downside risks to the property market, mortgage holders and the economy.