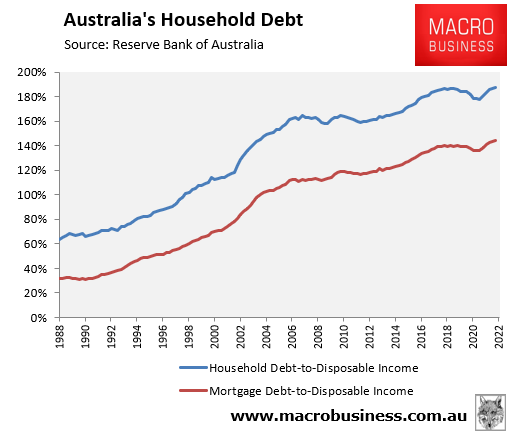

The Reserve Bank of Australia (RBA) on Friday released household debt statistics for the June quarter, which revealed that aggregate mortgage debt hit an all-time high 144.1% of aggregate household disposable, with total household debt also rising to a record high 187.5% of disposable income:

Australian household and mortgage debt hit fresh all-time highs in Q2.

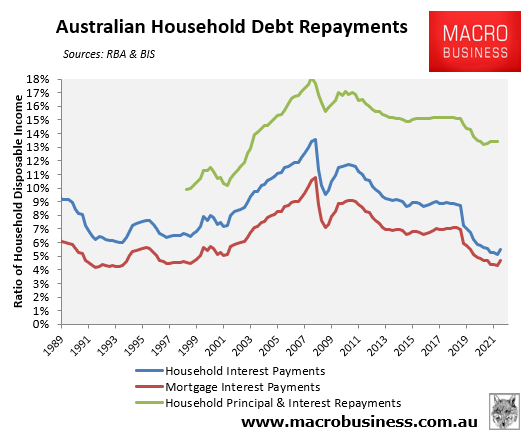

With interest rate rising by 0.25% in May and a further 0.5% in June, the share of household income going towards mortgage and household debt has risen to 4.7% and 5.5% respectively, whereas total principal and interest debt repayments (calculated by the Bank for International Settlements to March 2022) has also lifted to 13.4%:

Household debt repayments start to lift in response to rate hikes.

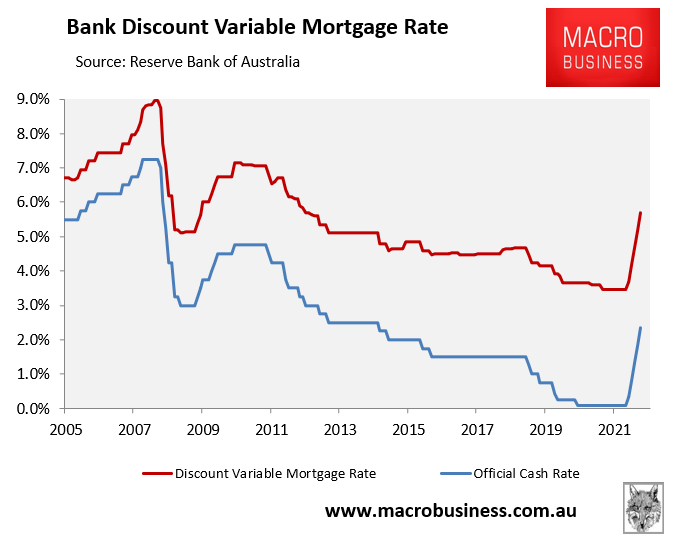

The above data obviously lags well behind the RBA’s rate. The mortgage and household debt data from the RBA is only current to the June quarter when the official cash rate (OCR) was 0.85%, whereas the BIS’ principal and interest debt repayments data is only current to the March quarter when the OCR was a record low 0.1% and Australia’s discount variable mortgage rate was a record low 3.45%.

Since then, the RBA has lifted the OCR to 2.35%, in turn driving the average discount variable mortgage rate to 5.70%. This is the sharpest rate of increase in Australia’s history and has delivered the highest mortgage rate in a decade:

Sharpest mortgage rate increase on record.

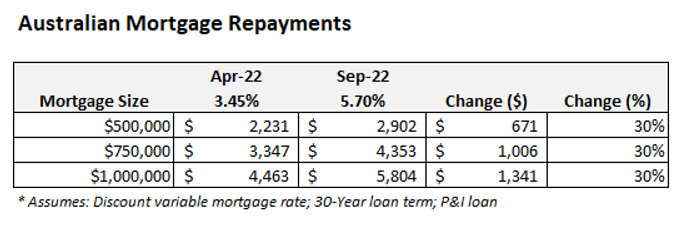

There has already been a significant impact on mortgage holders, with average mortgage repayments soaring by 30% from April’s pre-tightening level:

Variable mortgage repayments have already risen 30%.

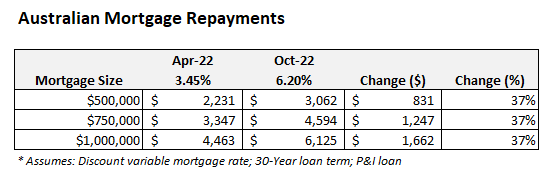

Most forecasters expect the RBA to hike the OCR another 0.5% at this afternoon’s monetary policy meeting, which would lift the average discount variable mortgage rate to 6.20% and raise monthly repayments to 37% from their pre-tightening level:

A 0.5% rate hike today would lift mortgage repayments by another 7%.

Whether the RBA continues to hike aggressively remains to be seen. However, Australian households’ world-leading debt loads, combined with their high exposure to variable mortgage rates, leaves them and the broader economy badly exposed.

For these two reasons, Australian households will be hit much harder than other nations from the global rise in interest rates.