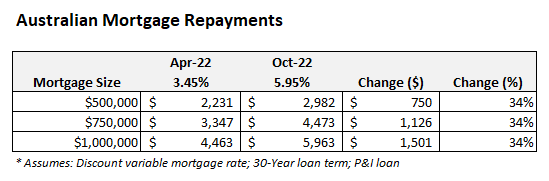

Tuesday’s 0.25% official cash rate (OCR) increase from the Reserve Bank of Australia (RBA) will lift the average discount variable mortgage rate to 5.95%, up massively from the 3.45% that presided before the first rate hike in early May.

In turn, average monthly mortgage repayments will jump 34% above their pre-tightening level. For a borrower with a $500,000 mortgage, this will represent a $750 increase in monthly mortgage repayments:

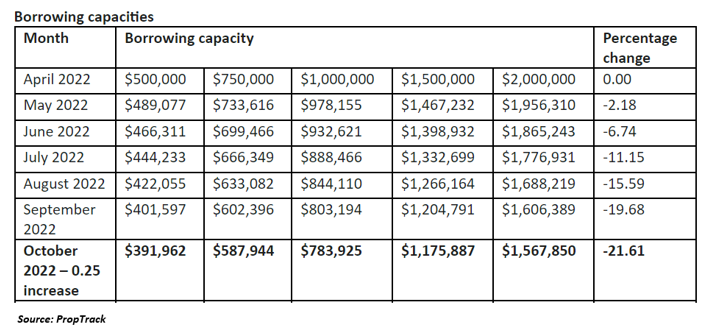

The RBA’s latest OCR increase will push house prices lower by further limiting borrowing capacity and shrinking the amount prospective home buyers can pay.

According to PropTrack, a prospective home buyer will be able to borrow 21.6% less after Tuesday’s 0.25% OCR increase. So, if a household was permitted to borrow $500,000 in April before the RBA’s first rate increase, they will now only be permitted to borrow around $392,000.

This reduction in borrowing capacity is the primary reason why house prices are falling and will continue to do so if the RBA continues to hike rates.

The process also works in reverse. Once the RBA starts cutting rates next year to ward off recession, borrowing capacity will rise, pushing house prices higher. We will be off to the races again.

In the meantime, the sharp rise in mortgage repayments and falling house prices is a bitter pill to swallow for home buyers that borrowed large sums to enter the market over the pandemic under Fear of Missing Out.

Many of these borrowers now face the prospect of negative equity, especially if they purchased in Sydney where house prices have fallen hardest (down 9% from peak).