ASB economists are tipping that New Zealand mortgage rates will “peak higher and earlier” than previously thought as the Reserve Bank of New Zealand (RBNZ) hikes the Official Cash Rate (OCR) to counter rising inflation.

ASB now forecasts the RBNZ will follow-up with 50 basis-point OCR hikes in May (to 2.0%), followed by a sequence of 25bp hikes to a 3.25% OCR peak in early 2023. This, in turn, will lift mortgage rates “to around 5-6% over the longer term”:

The RBNZ are clearly worried about the near-term inflation outlook and the risk that inflation expectations stray from the inflation target. The policy assessment acknowledged that the RBNZ has revised up their inflation outlook, with annual consumer price inflation expected to peak “around 7% in the first half of 2022”…

The RBNZ face a tricky balancing act. Either they tighten too aggressively and create a “sharper than needed slowdown in economic activity” or they do not act quick enough and face the longer run costs of entrenched high inflation and inflation expectations…

3.25% is considerably above the neutral OCR of 2% that is consistent with the economy sustaining steady momentum…

[This] means mortgage rates will peak higher and earlier (2022/2023) than our previous forecasts, before easing to around 5-6% over the longer term.

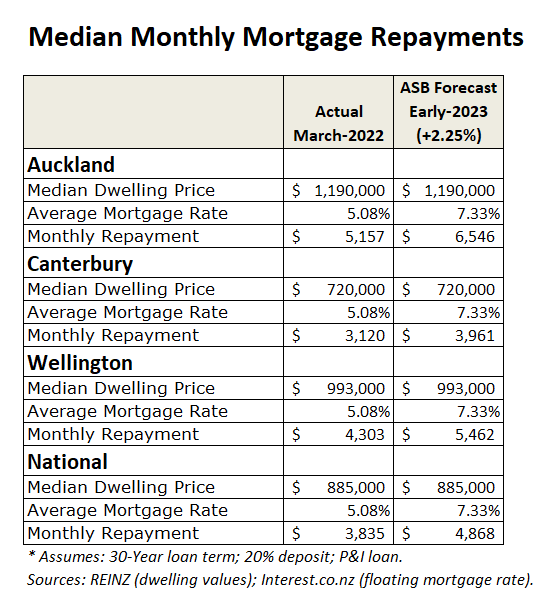

If ASB’s 3.25% OCR forecasts come to fruition and are passed onto New Zealand mortgage holders, then the average floating mortgage rate would rise to 7.33%.

The next table summarises the impact of the ASB’s forecast by comparing monthly mortgage repayments on the median priced New Zealand home at the end of March 2022 (when the OCR was 1.0%) with the projected increase outlined by ASB (to 3.25%) assuming steady home values:

ASB’s interest rate forecasts would see the monthly mortgage repayment on the median priced New Zealand home rise by $1,033 (27%).

Mortgage repayments would climb even further in Auckland (by $1,389 a month) and Wellington (by $1,159 a month) due to their higher median dwelling values.

Not surprisingly then, there are fears up to half of New Zealand first home buyers could suffer financial distress if mortgage rates rise above 6%, let alone above 7% as forecast above:

The [RBNZ’s] own research, released to the Herald under the Official Information Act, reckons as many as half (49 per cent) of the people who bought their first home last year during the market peak could face “serviceability stress” if interest rates hit 6 per cent.

This would hammer the tens of thousands of buyers who took on debt at historically low interest rates who will now find themselves re-fixing their mortgages at much higher rates…

A Reserve Bank paper from September last year warned these people could face “serviceability stress”…

[First home buyer] Liam said he was “a bit worried” about borrowing costs increasing when his fixed term ends next year.

He estimates his annual borrowing costs could jump by an additional $25,000 once he comes off his fixed term…

[Mortgage broker] Bruce Patten said that wherever rates landed there would be pain.

“There will be people who have to sell and sell down.”

Recent leveraged first home buyers are about to get a harsh dose of interest rate reality.

If the RBNZ lifts rates as aggressively and ASB is predicting, then highly geared mortgage holders are cruising for a bruising.

New Zealand house prices would likely experience sharp falls and many recent buyers will likely be thrown into negative equity.