Last week’s federal budget contained various measures aimed at enticing first home buyers (FHBs) into the housing market.

In particular, the Home Guarantee Scheme was more than doubled to 50,000 places, thus enabling single parents to buy a home with a deposit as low as 2% and FHBs to purchase a home with a 5% deposit.

Sally Tindall, research director at RateCity, has warned that FHBs risk sliding into negative equity and facing spiraling mortgage repayments if Reserve Bank of Australia (RBA) lifts interest rates:

“The concern is [the government] is providing people with a way to spend an incredibly large amount of money on a property at overheated prices,” said Sally Tindall…

“Regulators are saying hold off while the government is saying jump in”…

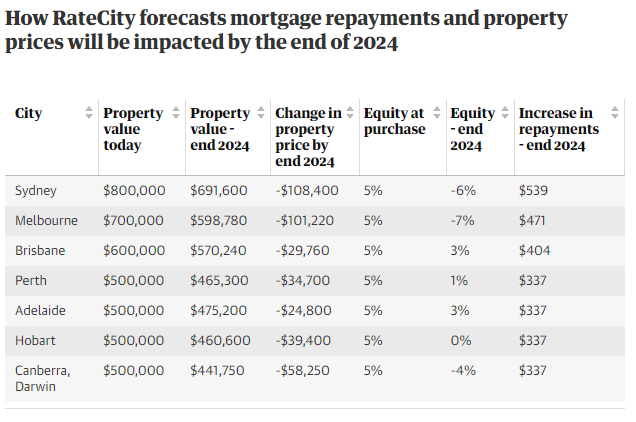

For people in Sydney who buy a home under the scheme this year, with a 5% deposit at the capped $800,000 price, their mortgage repayments will rise by about $539 a month by the end of 2024, according to RateCity. The house’s equity could also drop by 6% at the same time, meaning they would owe the bank more than the house was worth…

These calculations are based on Westpac’s cash rate and property price forecasts to 2024.

Advertisement

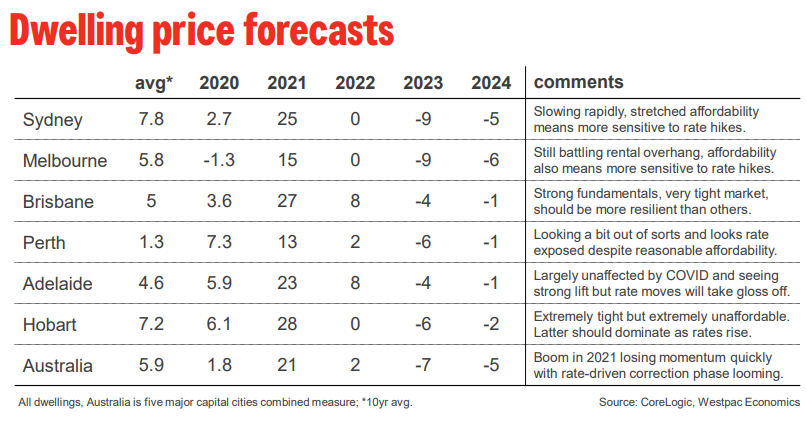

Westpac’s forecasts aren’t even that bearish. The bank forecasts a “terminal peak [in the RBA cash rate] of 1.75% by end 2023”, alongside a moderate 12% decline in national dwelling values over 2023 and 2024:

Westpac forecasts two year house price correction.

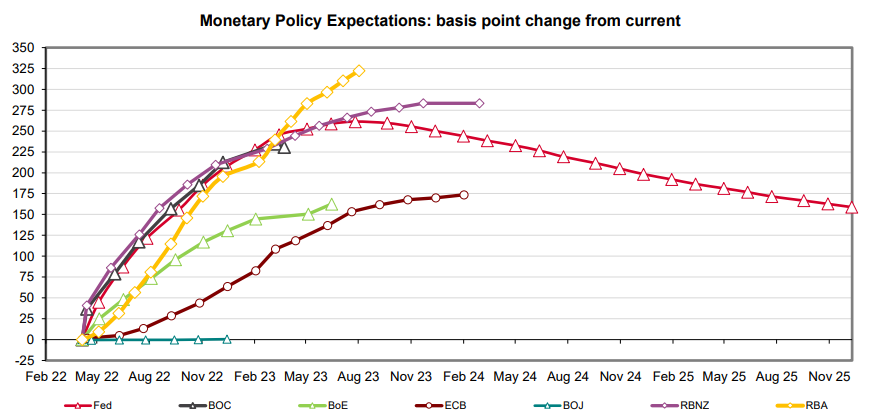

The latest futures market forecast has the RBA hiking the official cash rate (OCR) by 3.25% by August next year (yellow line below) – equivalent to thirteen 0.25% rate hikes in only sixteen months:

Advertisement

Fancy 13 interest rate hikes in only 16 months?

If the RBA followed through with the market’s forecast, then the average discount variable mortgage rate would lift to 6.85% from 3.60% currently, with the median monthly mortgage repayment rising a whopping 44%.

Using the Sydney example cited above by Sally Tindall, monthly mortgage repayments on an $800,000 Sydney home would rise by $1,284 under the market’s interest rate scenario.

Advertisement

FHBs better hope the futures market is wrong on interest rates. Otherwise, they are facing a crushing rise in mortgage repayments, alongside deep negative equity as house prices collapse.

Providing government-sponsored mortgages to people with 2% to 5% deposits is a bad idea at the best of times. It is even worse when the market is topping-out and interest rates are about to rise.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.