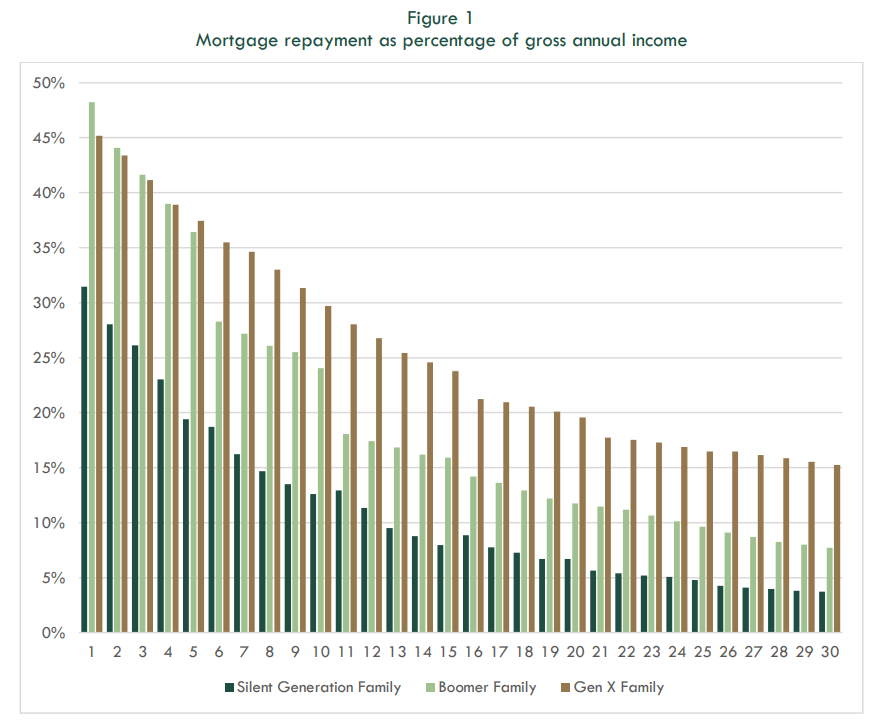

Think Tank Per Capita has released a new discussion paper entitled “Generation Stressed”, which shows that Australian households have experienced “a significant increase in the lifetime expenditure on the median mortgage” over the generations, specifically:

“For a Silent Generation family buying in 1970, the average repayment cost over the course of the mortgage was 11.2% of their gross income”.

“For a Baby Boomer family buying a home in 1985, the average repayment cost over the life of the mortgage came out at 19.5% of gross income”.

“For a Generation X family though, who bought in 2000 and have approximately nine years left to go on their mortgage, we estimate they will spend 25.5% of their gross income on servicing mortgage debt”.

“That is a 130% increase in the lifetime cost of owning a home over 30 years”.

The next chart summarises the results:

Younger generations paying more of their lifetime’s earnings in housing.

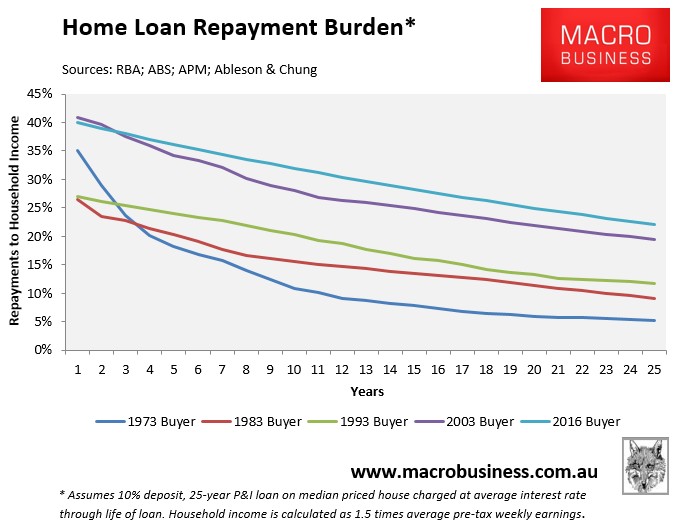

Moreover, younger generations are remaining indebted for longer due to low inflation and wage growth, which means debts are no longer inflated away:

Advertisement

The household debt of the Silent Generation family was worth around 3.7 years of median full-time male annual earnings in the first year of the mortgage, but after five years over half of the debt had been inflated away to just 1.8 times annual earnings.

Thirty years later, the initial mortgage debt taken on by the Generation X family equated to 5.6 times annual earnings, and was still at 4.1 times after five years.

We estimate the Gen X family is paying $1425 per month on their mortgage in 2021. If they were on the same repayment trajectory as the Boomer family their monthly bill would be $910, while if they were on the Silent Generation trajectory it would be just $440 a month.

For the individual family, this is a huge loss of income – almost $1,000 a month – that would be better directed toward education, health or other living expenses. For the nation, it represents a significant constraint on household consumption, which accounts for more than half of Australia’s economic activity.

Ultimately, we argue that the role of inflation and wage growth needs to be front and centre when looking at changes to mortgage affordability between generations, and that our principal measure of inflation, the Consumer Price Index (CPI), fails to adequately account for the increase in the cost of living for mortgagee households.

The inherent problem with [most common] affordability measures is that they only gauge initial housing payments on new mortgages at the particular moment in time, and not repayments over the full 25 to 30 year loan term…

Today’s home buyer is facing a much more difficult loan repayment schedule than at any other time in living history due largely to the combination of high home prices, low inflation and low income growth:

Advertisement

Basically, when you take out a mortgage in a world of high inflation, your payments are ‘front-end loaded’ and reduce quickly over time.

But in the current world of low inflation and low wage growth, repayments consume a large proportion of your wage at the start and they’ll keep doing so for decades.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.