Westpac have their latest note out on the country’s financial account:

The COVID-19 pandemic sent shock waves through Australia’s financial account in the first half. The September quarter has since seen a return to more normal conditions.

From the data for the nine months to September, it is evident that foreign investors’ appetite for Australian assets has remained resilient throughout. This is particularly true of direct investment which still saw a solid inflow of capital through the worst of the pandemic.

Australia’s success in containing the virus and the coming deployment of vaccines across the globe should support continued robust growth in financial investment in Australia in coming quarters across direct and portfolio investment types.

Australian investors will also continue to increase their exposure to the global economy by investing more capital offshore. As the majority of this investment is in equities, this suggests a further increase in investment income could be seen in coming quarters, further reducing our net income deficit from its current historic low.

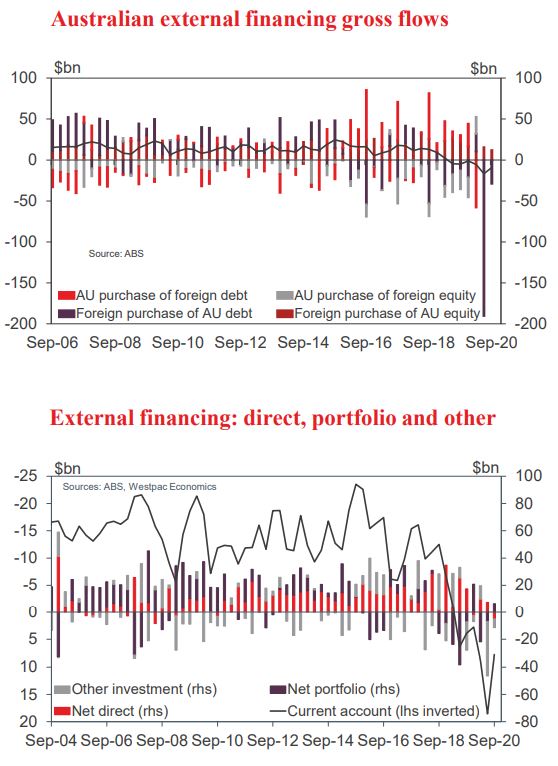

The financial account is reported on an unadjusted basis, so a measure of volatility is certain every quarter. In Q2 2020 however, COVID-19 sent shock waves through Australia’s and the world’s financial accounts. The Q3 data confirm this was a one off and also that initial estimates overstated some aspects of the shock. Most significantly, direct investment inflows were revised up for Q2 and, conditions considered, they showed solid momentum in Q3. Taken together and annualised, the Q2/ Q3 gross inflows were a little less than 40% of the average seen over the

proceeding five years ($25bn versus the $64bn annual average to Q1 2020).

While net direct investment recorded an outflow in Q3 2020, this came as a result of Australian firms increasing their offshore investment. For this investment flow, the year to September 2020 has been unusual, with the outflow from Australian firms to foreign subsidiaries more than three times the average of the prior five year period ($25bn compared to $8.4bn). With the outlook for vaccines and hence the global economy having improving materially since September, direct investment flows should strengthen into 2021 as firms look to expand capacity and deploy capital in pursuit of return as the global economy rebounds.

Portfolio flows have historically proven much more fickle than direct investment, being the result of often singular, in-themoment investment decisions in liquid assets such as equities and bonds. Unsurprisingly, the $6.8bn net portfolio outflow of Q2 was essentially reversed in Q3 by a $6.5bn inflow. Looking at the portfolio investment gross flow detail, having pulled $46bn and $24bn from Australia in Q1 and Q2 respectively, foreign investors invested $55bn in Q3. Australian investors’ reset in Q3 was more aggressive still, a $48bn outflow more than reversing the $24bn and $18bn repatriations of Q1 and Q2 2020.

With risk appetite continuing to firm in Q4, large two-way flows of capital are anticipated again in Q4 and early-2021. Other investment (loans and deposits) has been a significant negative for Australia’s funding mix in 2020. While the immediate effect of COVID-19 on other investment flows in Q1 saw a net inflow of almost $10bn, come Q2 this flow reversed four fold,

-$40bn. Another outflow of $6bn was then seen in Q3. Over the three quarters, the running down of deposit balances was responsible for $16bn of the net $36bn other investment outflow. Loan transactions contributed a further $13bn to the decline in funding.

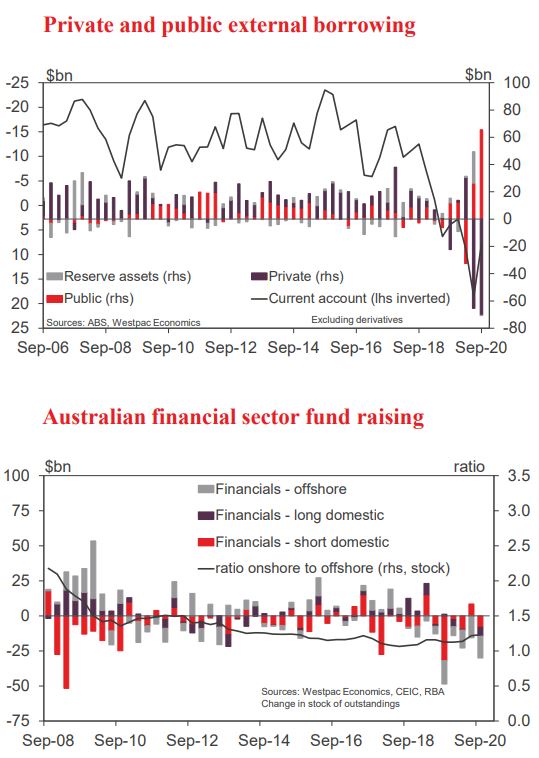

The financial sector. Market uncertainty typically restricts new debt issuance by financials for a time. But, in Q3 2020, even as risk appetite and liquidity has returned, the stock of outstanding financial debt has continued to contract. The RBA’s bond data suggests Australian financials outstanding stock of foreign-issued debt has declined consistently by $15bn per quarter in 2020.

Short and long-term domestically-issued debt on issue has also been reduced, respectively by $9bn and $7bn over the nine months to September.

These outcomes are the result of the combined effect of weak intermediated credit demand both before and during the pandemic; strong growth in bank deposits on precautionary savings and fiscal support; and the availability of bank funding from the RBA at the cash rate through the Term Funding Facility. Ahead, the availability of deposit/TFF funding and modest growth in credit is likely to see financials’ paper on issue continue to trend down, reducing Australia’s stock of private debt liabilities.

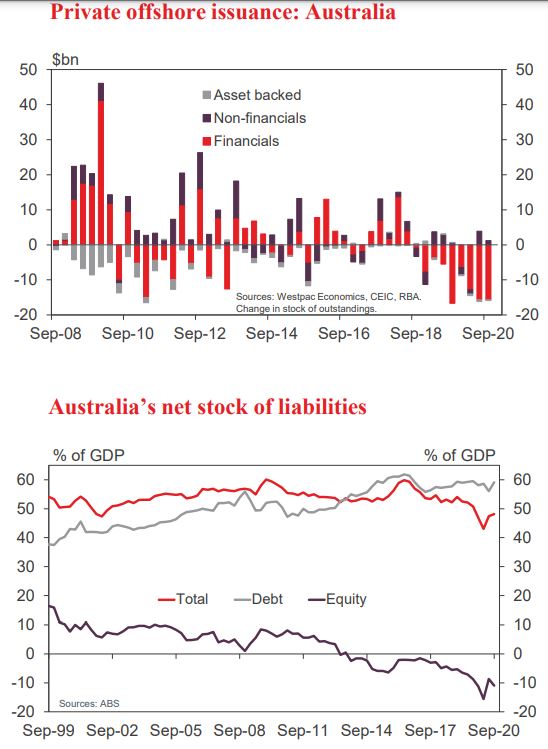

Non-financial corporates and public sector. As above, direct investment into Australia slowed materially in Q2 and Q3 2020 owing to the pandemic. However, as Australia has contained the virus better than most, direct investment inflows seem likely to accelerate quickly as the economy re-opens domestically and then in 2021 to the world. The current pipeline and return profile of mining investment in Australia and our proximity to Asia, where recovery prospects are strongest and most sustainable, also warrants such an expectation.

Corroborating this assertion, gross direct equity investment remained solid over Q2 and Q3 at about two-thirds the scale of preceding five years. The weaker total result for direct investment in Australia instead came as a result of the paying down of priorperiod loans. This suggests foreign investors remain committed to their Australian projects, but have strengthened their financial positions in case downside risks crystallise. The detail of Australian firms foreign direct investment also points to a desire to maintain exposure to growth opportunities. More than 85% of the gross direct investment outflows from Australian firms over the year to September was equity financed. The majority of this flow occurred in Q3 itself.

A similar proportion of cumulative portfolio investment outflows over the year to September were also equity related, and the majority of the outflow was seen in the most recent three months too. Portfolio investment inflows into Australia have in contrast been more balanced between equity and debt, with roughly twothirds of the inflow related to equity and one-third debt.

The international investment position (IIP). While Australia’s international investment position deteriorated in Q3, our net liabilities increasing to 48% of GDP in September 2020 from a low of 43% in March, the current level is still a material improvement from 51% a year ago and the peak of 60% seen in mid-2016.

Our stock of debt liabilities has decreased by 3ppts of GDP since the peak, explaining only a fraction of the total improvement. The majority of the gain instead stems from the increase in our net equity assets from 2% of GDP to 11% currently, the result of continued strong growth in Australian super balances and a greater proportion of our wealth being invested offshore.

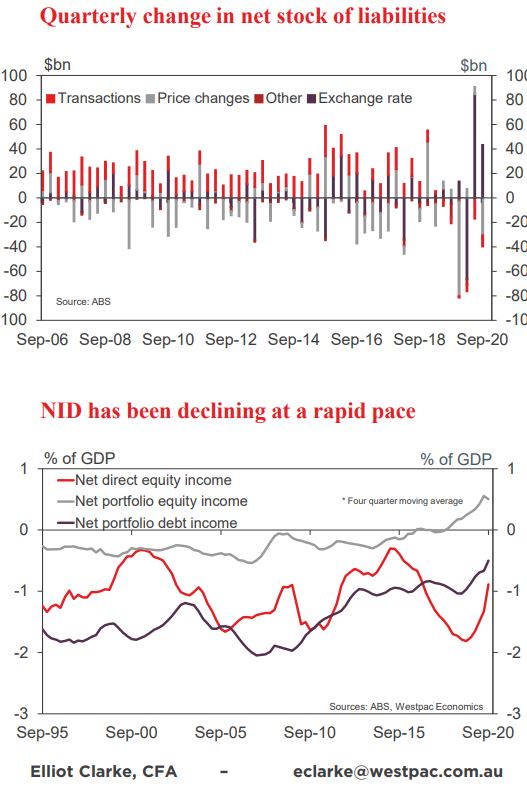

This significant shift in our financial assets and liabilities has combined with declining interest rates globally to materially reduce our net primary income deficit (NID), the sum of recurring income flows associated with our investment position.

Currently it is at a record low of just 0.7% of GDP, 3.8ppts below the 4.5% peak of Q4 2006. Over this period, the net cost of our debt liabilities has been reduced from around 2.0% of GDP to 0.5%. The net return from our portfolio equity investments has meanwhile increased from -0.4% to 0.6% to offset dividends paid to direct investors which are currently of a similar scale having

declined from 1.5% of GDP back in 2006.