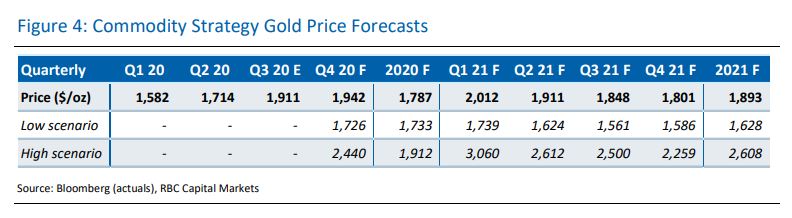

For some time we have been calling out not just the 2020 US presidential election itself as a potential source of uncertainty for gold, but rather that potentially volatile aftermath and uncertainty following it could prove a source of volatility and/or upwards price momentum for gold in our view. In fact, in the most uncertain of scenarios, our high scenario price forecasts could be achieved in Q4 2020 and into Q1 2021 (see Figure 4). The aftermath we are talking about here is not just about who wins (election outcomes and party affiliations themselves have little historical predictive power for gold in our analysis), but rather the idea that one candidate may simply not accept the outcome presents a key of gold-relevant uncertainty in our view. We believe, this makes it materially different from past examples as it is not about a simple concession timeline, but rather, this type of contested election outcome could be a key driver for gold in an already uncertain world given the lack of true precedent.

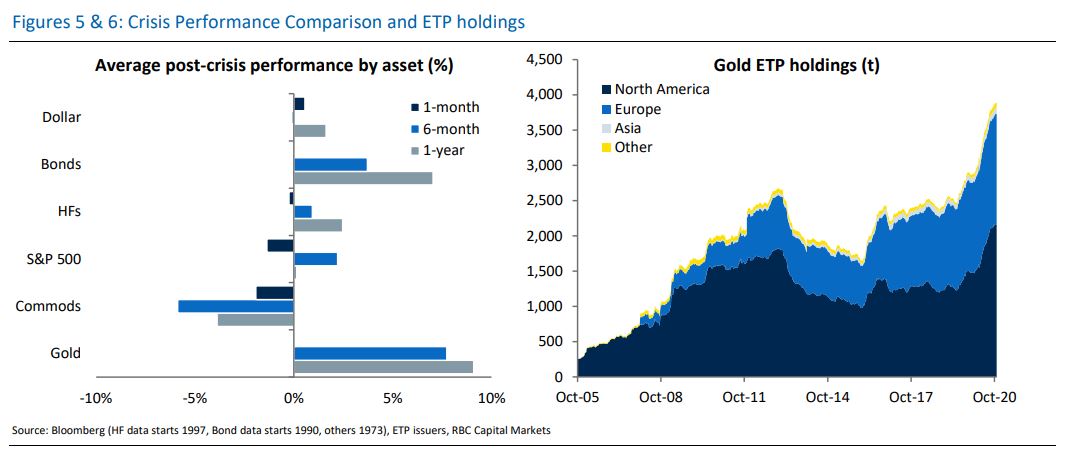

If we are right, and gold does react in such an extreme scenario, it is because this time is different, not just because it is a US presidential election cycle or because of simple seasonality. Gold has moved already this year; 2020 has seen gold prices rise to all-time highs on the back of economic uncertainty, the COVID-19 pandemic, a host of political/geopolitical issues, and a largely gold-positive monetary policy backdrop. We think the record run in ETP holdings this year, having added about 1000 tons to date (see Figure 6), reflects investor appetite in the face of risk and uncertainty, a theme which pervades most markets and beyond. The added uncertainty if the election’s outcome is contested (i.e. if Trump contests a Biden victory and does not accept the outcome), would be a volatility or price positive event for gold in our view.

While much of the market’s attention has been focused on equity market volatility as a result of election turmoil, we think gold in particular will play a unique role here. While gold has a mixed reputation as a hedge against purely political or geopolitical crises, it can and does react in times of extreme panic (see Figure 5). Durable performance most often depends on economic and financial fallout from a given crisis, but in periods of immediate panic, there are few options and gold tends to stand out as a “perceived safe haven,” even if it is imperfect one. It comes down to the lack of other options, particularly in a scenario where we are looking at a US-driven risk, gold’s lack of nationality makes it unique. Gold’s recent consolidation certainly opens up room for it to move more in Q4 and into Q1, particularly on the back of these less-tickerized drivers. Thus, the aftermath of the 2020 US presidential election cycle and the acceptance of its outcome could prove immensely impactful for gold in the more extreme scenarios.

I am still bullish gold for next year but, since the virus has so comprehensively taken off in the US again, the timeframe has been pushed out as DXY remains strong through the second wave risk period.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.