Stocks are advancing across the region here in Asia although mainland Chinese stocks are struggling to make ground, as positive sentiment from US earnings overnight (notably Tesla and Microsoft) and a lower USD keeps risk spirits going. Commodity prices remain stalled as the oil price lifted overnight with bond yields also steady going into a slew of economic releases and catalysts tonight.

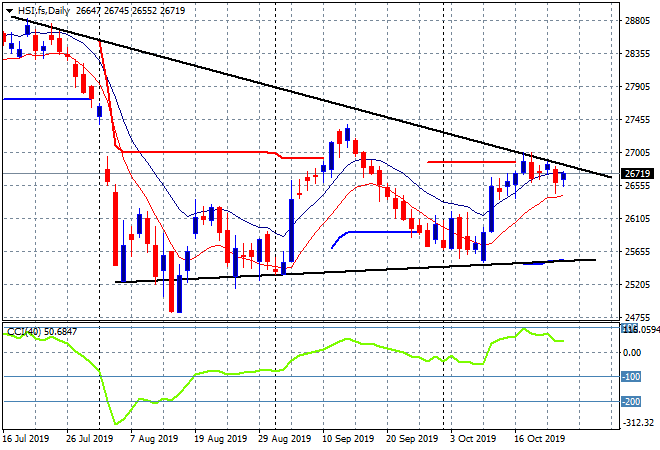

The Shanghai Composite is still struggling to get back on track but is slipping late in the session, down a handful of points to 2939, remaining well below 3000 points as the Hang Seng Index launches higher, up 0.6% to take back half of its previous losses, currently at 26727 points and still unable to crack resistance overhead at the 27000 point level:

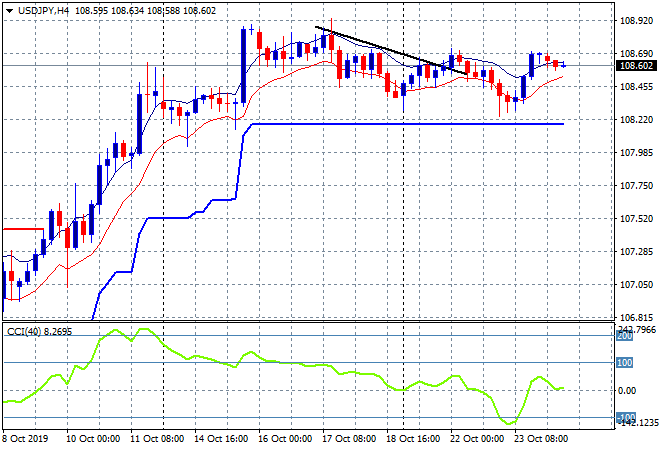

Japanese share markets are doing well with the Nikkei 225 up 0.55% to 22750 points despite a wishy-washy move in Yen throughout the session, with the USDJPY pair unable to beat its overnight high at the 108.70 level after a recent bounce off the trailing ATR support level, leaving it open to a stall here:

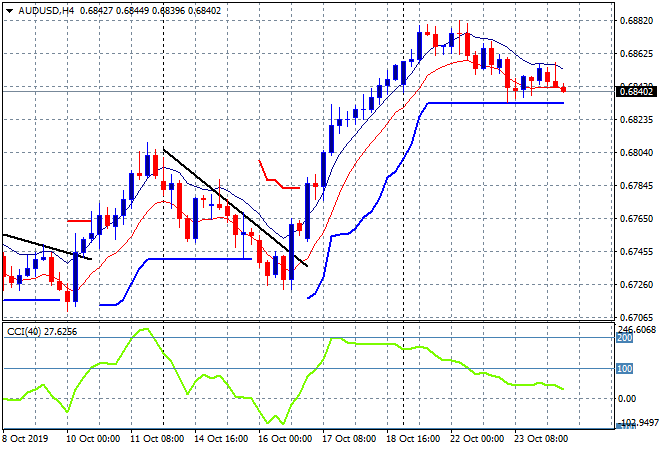

The ASX200 started well, up over 0.5% before deflating going into the close to be up 0.3% and just shy of 6700 points. The Aussie dollar is not finding any buying support with a series of slightly lower session lows, gravitating down to ATR support at the 68.20 level and ready to breakdown:

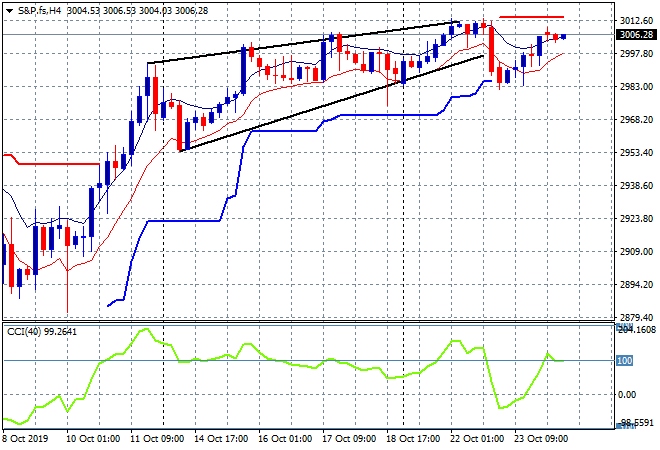

Both S&P and Eurostoxx futures are relatively flat with the latter up only a few points with the S&P500 four hourly chart showing a desire to return to the previous highs above the psychologically important 3000 point barrier, with support at 2980 points a good uncle point from here:

The economic calendar is stacked tonight with the ECB monthly meeting, plus a slew of monthly PMI’s from both sides of the Atlantic and the latest US durable goods orders.