A generally positive day across Asian risk markets excepting mainland China, following the good mood on Wall Street overnight. The Australian dollar continued to tank following yesterday’s release of the RBA minutes while the NZD was relatively stable despite an uptick in monthly CPI. Yen strengthened slightly after a big breakout in USD strength overnight while gold steadied at the $1485USD per ounce level.

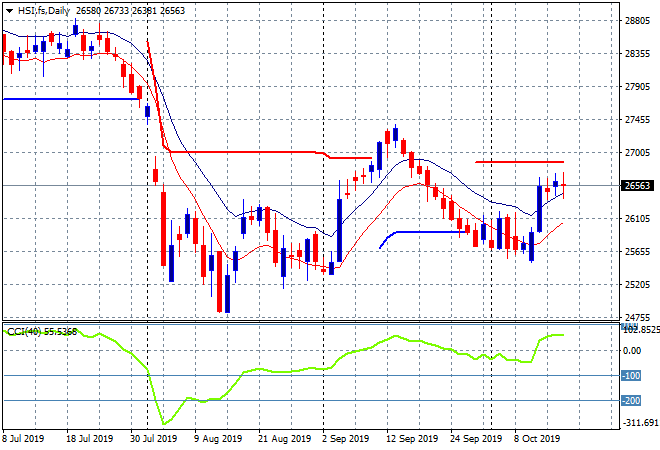

The Shanghai Composite spiked on the open but couldn’t hold the gains after the long lunch break, currently down over 0.4% to 2980 points while the Hang Seng Index went the other way and has gained over 0.4%, now up to 26618 points and looking to solidify the previous breakout and make another attempt at cracking resistance at 27000 points:

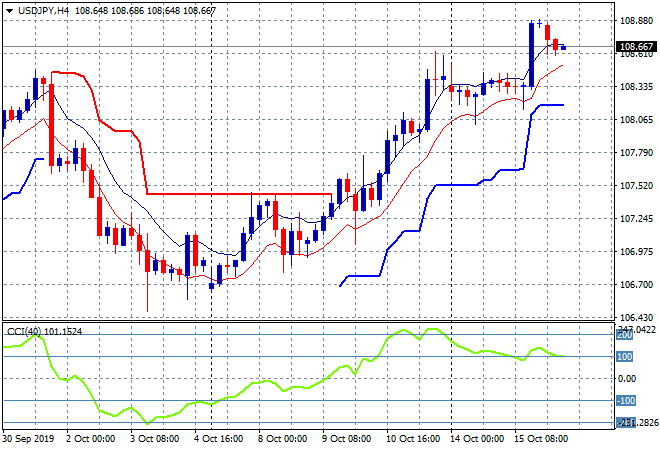

Japanese share markets advanced on the overnight weaker move in Yen and the positive sentiment overall with the Nikkei 225 closing 1.3% higher at 22501 points. The USDJPY pair pulled back slightly following that big move overnight as expected, easing back to the 108.70 level after almost cracking through the 109 handle in what has been a sharp advance this last week and a half:

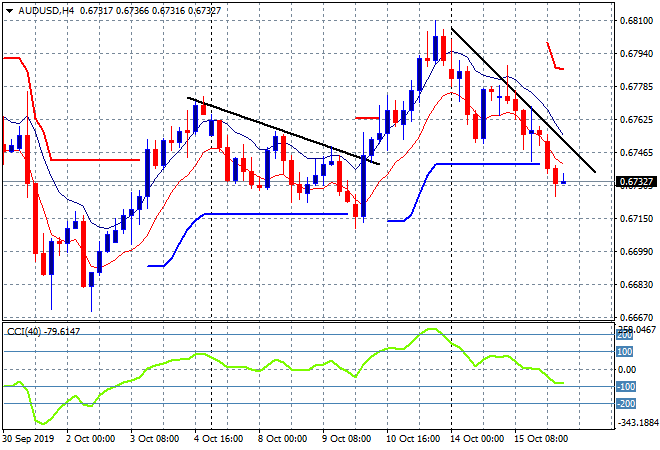

The ASX200 was also a big mover, finishing 1.2% higher at 6736 points helped by the continuing weak move in the Australian dollar, which has now fallen below ATR support at the 67.40 level. The next level of support at the 67 handle proper may come under pressure in tomorrow’s numberwang unemployment print:

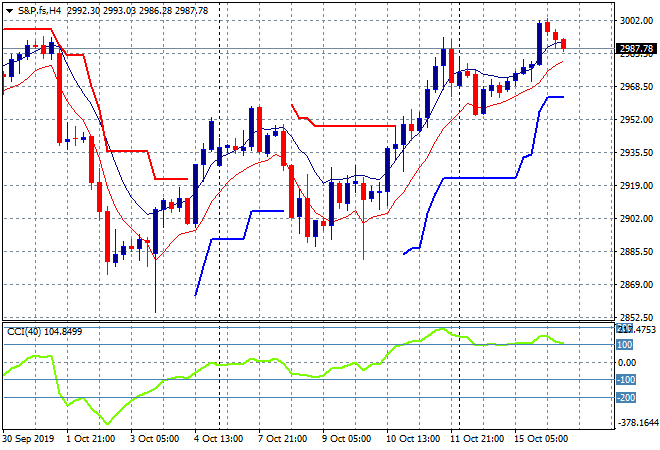

Despite the positive moves here in Asia, both S&P and Eurostoxx futures are down slightly with the S&P500 four hourly chart still showing a reluctance to break over the psychologically important 3000 point barrier, as traders continue to weigh up overseas macro risks:

The economic calendar has a CPI focus tonight, with final September results for the UK, EZ and Canada while advanced retail sales numbers from the US will be an important release as well.