By Gareth Aird, Senior Economist at CBA

Key Points:

- Australian residential property prices have fallen over the past nine months.

- Further declines appear likely over the next year due to softer credit growth, a continued lift in apartment supply, less foreign demand and more rational price expectations from would-be buyers.

- We retain our view, however, that a hard landing looks unlikely and is not our central scenario.

Overview:

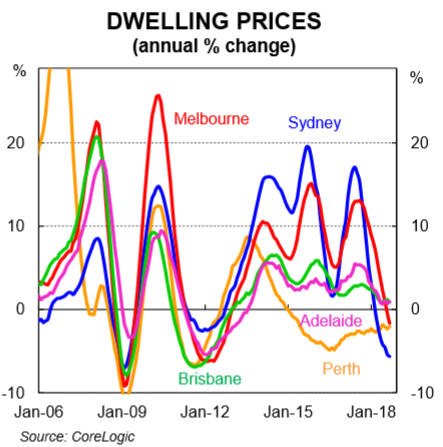

Australian capital city dwelling prices, led by Sydney and Melbourne, have fallen over the past nine months. The correction is occurring after five years of incredibly strong price growth. It is our view that prices will to continue to deflate over the next year as evidenced by the leading indicators. Credit standards

have been tightened and this will continue to weigh on the flow of new lending, new dwelling supply will remain elevated, mortgage rates are more likely to go up

rather than down and buyer expectations have adjusted downwards from exuberance to more sober levels.

We do not expect a hard landing, however. Population growth, driven by net immigration, is expected to remain strong. And rental growth is still positive, which

ensures yields look reasonable in a low interest rate world. We also expect the unemployment rate to gradually drift lower, which means that the risk of default is low. Against this backdrop we have the RBA on hold for at least another year. In summary, we expect the orderly deflation in dwelling prices to continue against an

economy that is performing relatively well from an output and employment growth perspective.

While predicting property prices can look foolish retrospectively, our quantitative assessment of the residential market overlaid with our qualitative views leads us to conclude that national property prices are likely to end the year down 3¼% (i.e. down by 3½% from the peak in December 2017). Further falls of around 2¼% look likely in 2019. As is generally the case, there is likely to be significant variation in outcomes by capital city. We expect Sydney and Melbourne to underperform

relative to the national average. This note discusses our outlook for Australian residential property prices and tables our forecasts by capital city.

Latest data

Dwelling prices in the eight capital cities combined fell by 0.4% in August. This was the eleventh consecutive monthly fall. Dwelling prices are down 2.9% over the year

and 3.1% from their peak in September 2017 (chart 1).

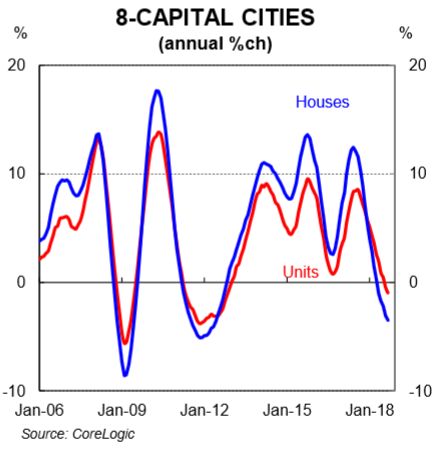

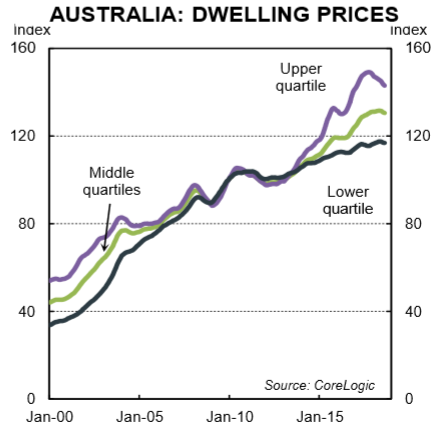

Units have generally been performing better than detached houses. Over the year, unit prices were down by 1.0% while detached houses were down 3.5% (chart 2). Units are generally cheaper than houses and the bottom end of the market is holding up better than the top (chart 3). That’s in part due to first home buyer assistance measures in NSW and Victoria that came into effect last year.

Why are prices falling?

Changes in dwelling prices are impacted by a variety of factors. At present, several of the factors that influence prices are working in a way that is putting downward

pressure on values.

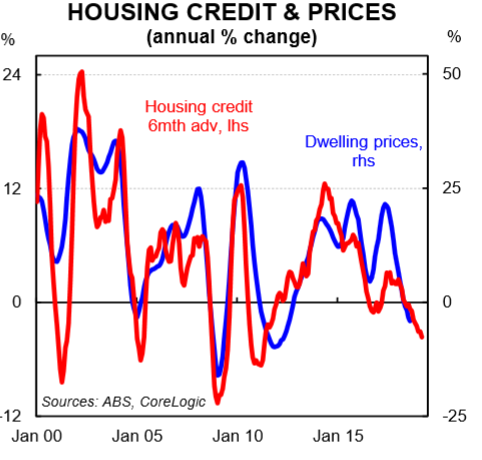

First, although the RBA’s policy rate has been on hold since August 2016, some mortgage rates have risen. Regulatory changes introduced to slow the flow of credit to investors as well as growth in interest only lending has resulted in higher mortgage rates on some types of loans. These higher mortgage rates have dampened the appetite for credit amongst investors. As a result, the total flow of credit has fallen and this is weighing on prices (chart 4).

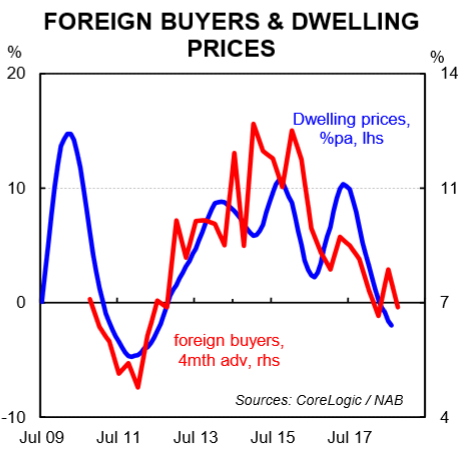

Second, foreign investment in Australian property has waned a little (chart 5). That is, the foreign investor share of property purchases has fallen. Controls on Chinese residents looking to deploy capital outside of China have had an impact. And the lift last year in State Government stamp duties levied to foreign investors in NSW and Victoria has dampened the overall demand for Australian property by international investors.

Third, expectations around property price appreciation have adjusted downwards. According to the WBC / Melbourne Institute, the proportion of households expecting dwelling prices to rise over the next twelve months has fallen to its lowest level since the question was first asked in late 2009.

Four, total listings remain elevated, particularly in Sydney. Five, there is a general fatigue in the market which is to be expected after such a prolonged period where

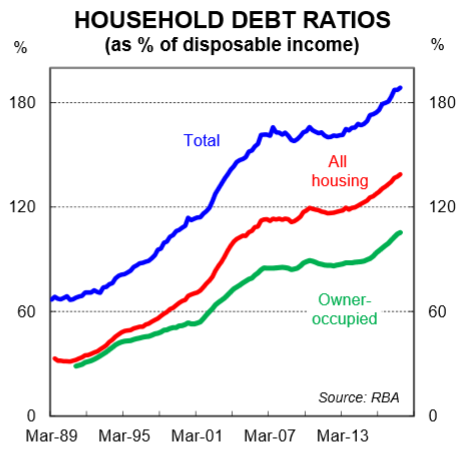

price growth outstripped income growth – there is a limit to the amount of debt that households can take on relative to income. Debt to income is currently at a record high in Australia (chart 6).

How far will prices fall?

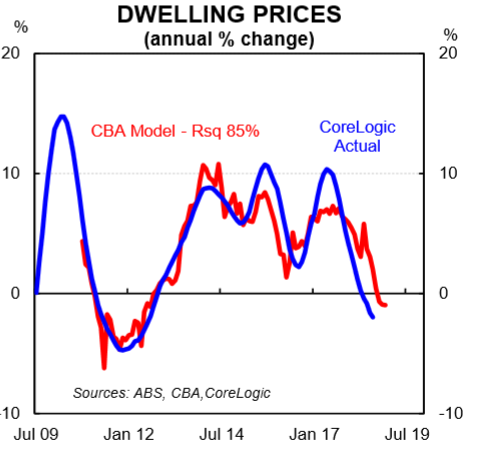

We have developed a model that puts the annual change in national dwelling prices as a function of the annual change in mortgage rates (1 year advanced), the annual change in the flow of credit (six months advanced), auction clearance rates (four months advanced) and the house price expectations index from the WBC/MI Consumer

Sentiment survey (2 months advanced). The model explains trends in dwelling prices very well (chart 7).

Clearly, we can’t forecast auction clearance rates or the household perception around the future path of dwelling prices. But we have the latest data on both of those measures which helps us to project near term movements in prices. In addition, the flow of credit and changes in mortgage rates have historically had a lagged impact on dwelling prices of between six and twelve months. So we believe that we can forecast dwelling prices over a six-twelve month period with a reasonable degree of confidence.

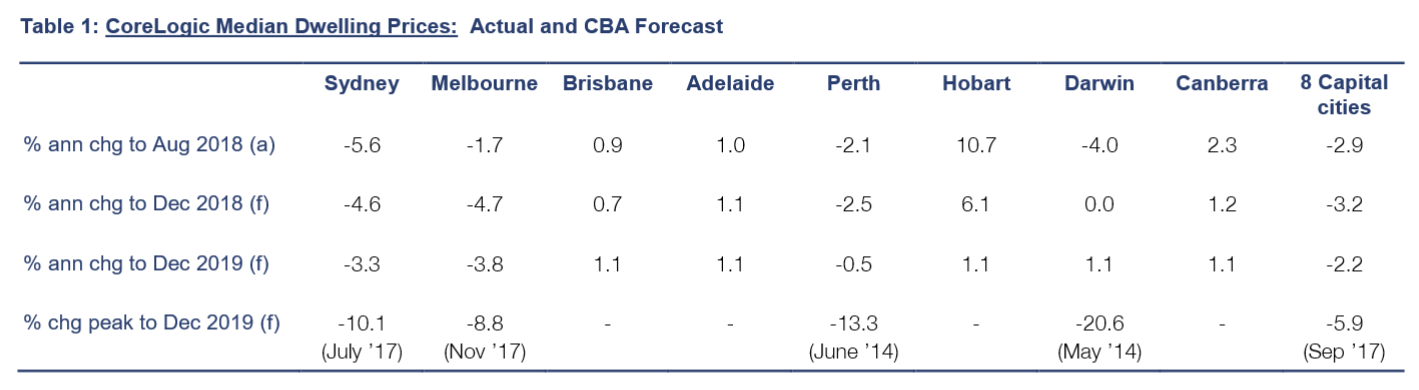

Our base case for property prices has them down by 5%pa in Sydney and Melbourne by end 2018. That would take the fall in Sydney prices from its July 2017 peak to around 7½%. For Melbourne, prices would be down by around 5% from their November 2017 peak. Some further dwelling price deflation looks probable in 2019 and we see the peak to trough being around 10% in Sydney and a little less in Melbourne. For Brisbane, we see prices trending broadly sideways over the next 1½ years. Dwelling prices are likely to stabilise in Perth in 2019 as vacancy rates decline and rents trough. Nationally, we think prices will end the year down by around 3% with a roughly

similar outcome likely in 2019.

That would mean the total correction in dwelling prices is not too dissimilar to the corrections of 2010 and 1989.

Table 1 details our point forecasts by capital city. They have been prepared on a no policy change basis.

Why not a crash?

A crash could be broadly defined as a fall from peak to trough of around 20%. Many international observers (and a few local ones) expect this result. But that would be a significant correction and would require a lift in the unemployment rate or materially higher interest rates. We have neither outcome in our central scenario. We see the unemployment rate as more likely to drift a little lower from here while any tightening in monetary policy is likely to be very gradual.

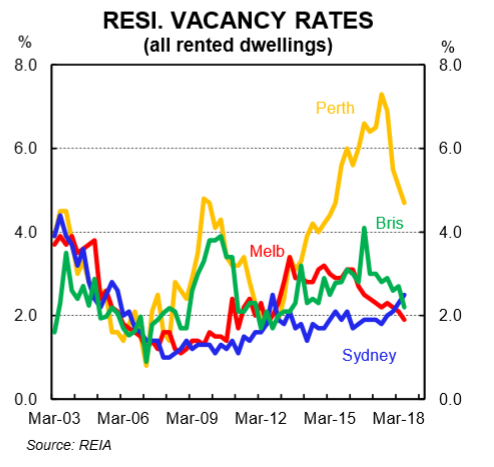

In addition, Australia’s high population growth rate, which is driven by a large intake of around 200k migrants each year, looks set to continue. Despite concerns being raised about Australia’s strong population growth, there is bipartisan support from both major political parties to run a big immigration intake each year. This props up the underlying demand for housing and has kept a lid on vacancy rates despite record levels of dwelling investment (chart 8). In fact, as dwelling commencements edge lower policymakers may revert to talking about a “housing shortage”.

The latest data on vacancy rates, to June 2018, has rates moving lower in Melbourne, Perth and Brisbane. Strong population growth is the cause.

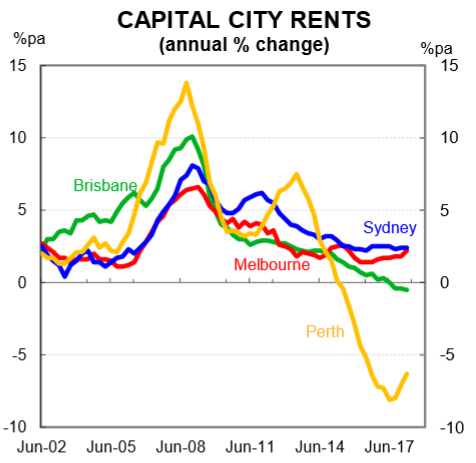

Finally, rental growth remains positive in Sydney and Melbourne (chart 9). We don’t see rents falling in Sydney or Melbourne without a change in Australia’s immigration policy. This provides a natural floor on how far dwelling prices can correct lower given interest rates remain around historic lows.

Risks

Downside risks:

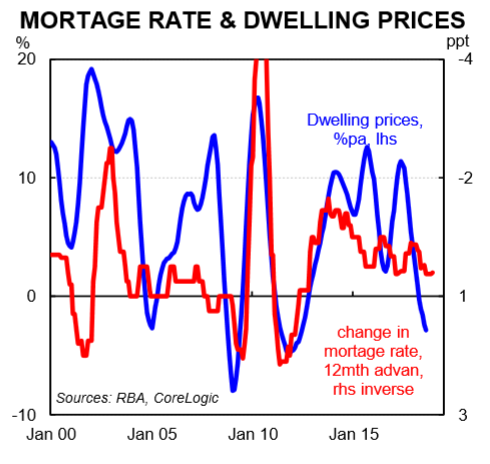

In our view there are three key downside risks to our view on property prices. First, higher interest rates. We expect the RBA policy rate to remain on hold until late 2019. But if the RBA was to tighten policy before then it would likely result in dwelling prices falling faster than we anticipate. In addition, any further material out-of-cycle interest rate hikes by the major lenders in Australia would put additional downward pressure on dwelling prices given the relationship between mortgage rates and

prices (chart 10).

Second, a reduction in the migrant intake. We are heading into an election year and there is a risk that one of the major parties opts for a different policy stance on immigration (i.e. they lower it). A decision to drop the migrant intake would reduce the demand for housing while it would have no short term impact on dwelling supply. As a result, prices would be lower than otherwise. And growth in rents would also be weaker.

Third, a change in the taxation treatment around housing. Specifically, reforms around negative gearing and the capital gains tax discount that reduce the attractiveness of property from a tax minimisation perspective would result in lower dwelling prices relative to our forecasts.

The Australian Labor Party has stated that it will reform negative gearing and the capital gains tax discount if they win government at the next election. They have not provided any specifics around timing, however.

Upside risks:

We consider there to be two key upside risks to our property forecasts. First, lower interest rates. We expect the RBA policy rate to remain on hold until late 2019. But if the RBA was to loosen policy before then it would likely result in dwelling prices not correcting as low as we anticipate. Second, any policy change to boost housing demand such as first home owner grants or lower stamp duty (to domestic or foreign buyers) is an upside risk to our base case.