Last week, economist John Adams penned an excellent article exposing the way that the Australian Prudential Regulatory Authority (APRA) has airbrushed Australian history to paint over the huge housing risks facing the economy:

This event was predicated on the assumption that a downturn in China would lead to a collapse in demand for Australian commodities which would in turn lead, over a period of approximately three years, to:

a subsequent downgrade in sovereign and bank debt ratings leading to a temporary closure of offshore funding markets;

a sell-off in the Australian dollar;

widening in credit spreads;

Australian real GDP falling by 4 per cent;

unemployment doubling to 11 per cent; and

house prices declining by 35 per cent…

The conclusion of APRA’s industry stress test was that Australian ADIs would suffer capital losses on their residential mortgage books of $AUD 40 billion over an approximate three-year period, which, while damaging, would not result in any Australian banks failing.

This quantum of capital loss, APRA claims, would be equivalent to losses experienced in the United Kingdom in the early 1990s, but would be less than what was experienced by either Ireland or America during the GFC.

Alarmingly, APRA’s $40 billion capital loss calculation, to which no documentary evidence justifying the calculation has been published, has already been criticised and disputed by independent analysts.

LF Economics analyst Lindsay David, using Westpac’s loan data as recently revealed at the current Banking Royal Commission, as a representative baseline for the Australian banking industry, estimated the potential gross capital loss for Australian ADIs on their residential mortgage books under APRA’s ‘severe, but plausible’ scenario would amount to a stunning $AUD 298 billion over the same 3‑year time period.

It is important to note that in LF Economics’ calculations is the use of their conservative assumption that only the riskiest fringe of borrowers default, that being borrowers who borrowed 11 times or more than their income or borrowers who have monthly uncommitted income of $AUD 70 or less.

This conservative assumption is a stark contrast to recent evidence from both Ireland and America where borrowers who borrowed more than 7 times their income in the case of Ireland and 8 times or more in the case of America defaulted.

Alternatively, Principal Analyst Martin North from Digital Finance Analytics using data from his own exclusive and extensive 52,000 Australian household surveys and surveys of small and medium enterprises coupled with his own independent economic model, calculated that the gross losses to Australian ADIs would be approximately $AUD 310 billion over five years.

These significant disparities in estimated capital losses are concerning and requires prompt clarification by APRA.

…it is beyond dispute that Australia is currently experiencing the biggest debt bubble in its history at the same time we are in biggest global debt bubble in the history of the world.

Given this frightening observation, it is stunning that APRA did not reference Australia’s previous economic depressions as a baseline worst-case scenario or in official parlance a ‘severe, but plausible scenario’…

It is abundantly clear that the purpose of APRA’s industry stress test is not to objectively assess the robustness of Australian ADIs under genuinely plausible economic conditions, but rather it is a public relations operation designed to artificially boost confidence in the Australian economy and domestic financial system.

However to achieve this objective, APRA can only design economic scenarios in which the banks can pass and in doing so, they have had to airbrush Australian economic history.

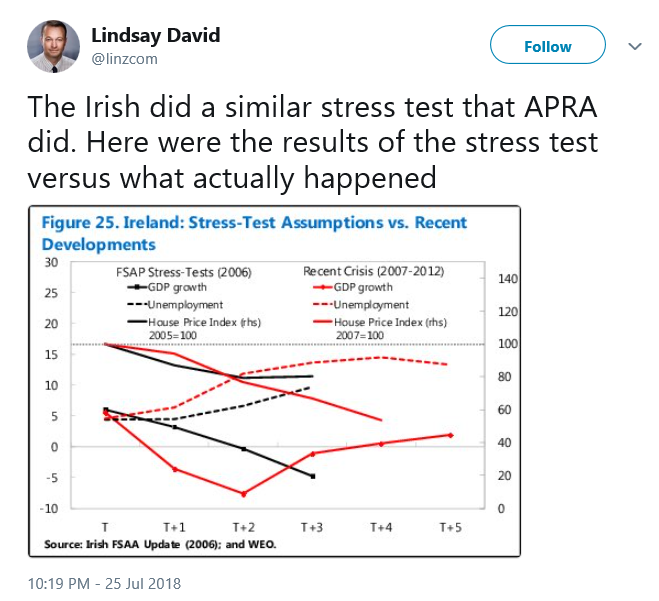

Founder of LF Economics, Lindsay David, also took to Twitter to lambast APRA’s Panglossian modelling:

Now John Adams and DFA’s Martin North have teamed up to dissect APRA’s dodgy modelling and possible future scenarios:

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.