DXY rebounded firmly Friday night as Trump tax reform is go:

Australian dollar pulled back:

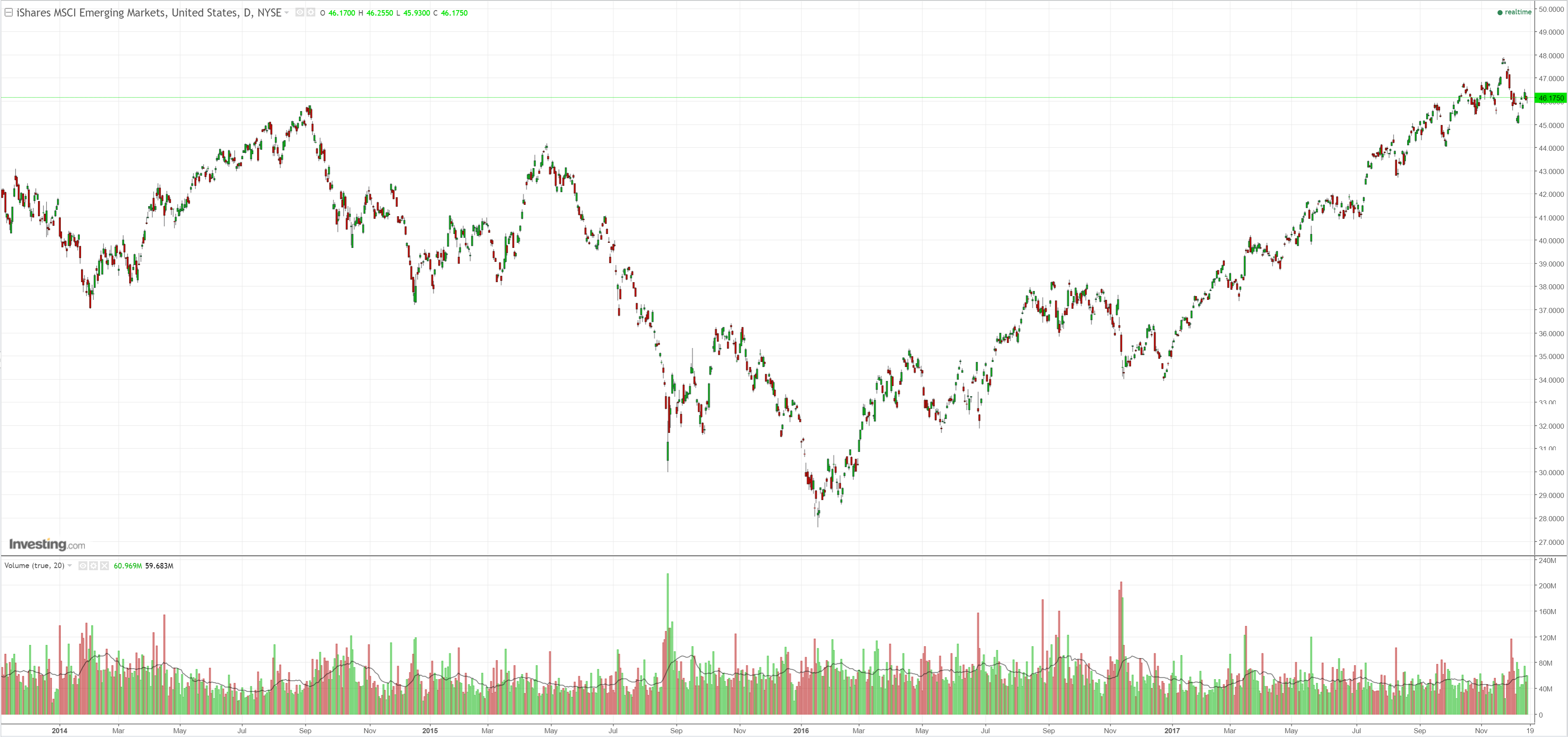

EM forex took off:

Advertisement

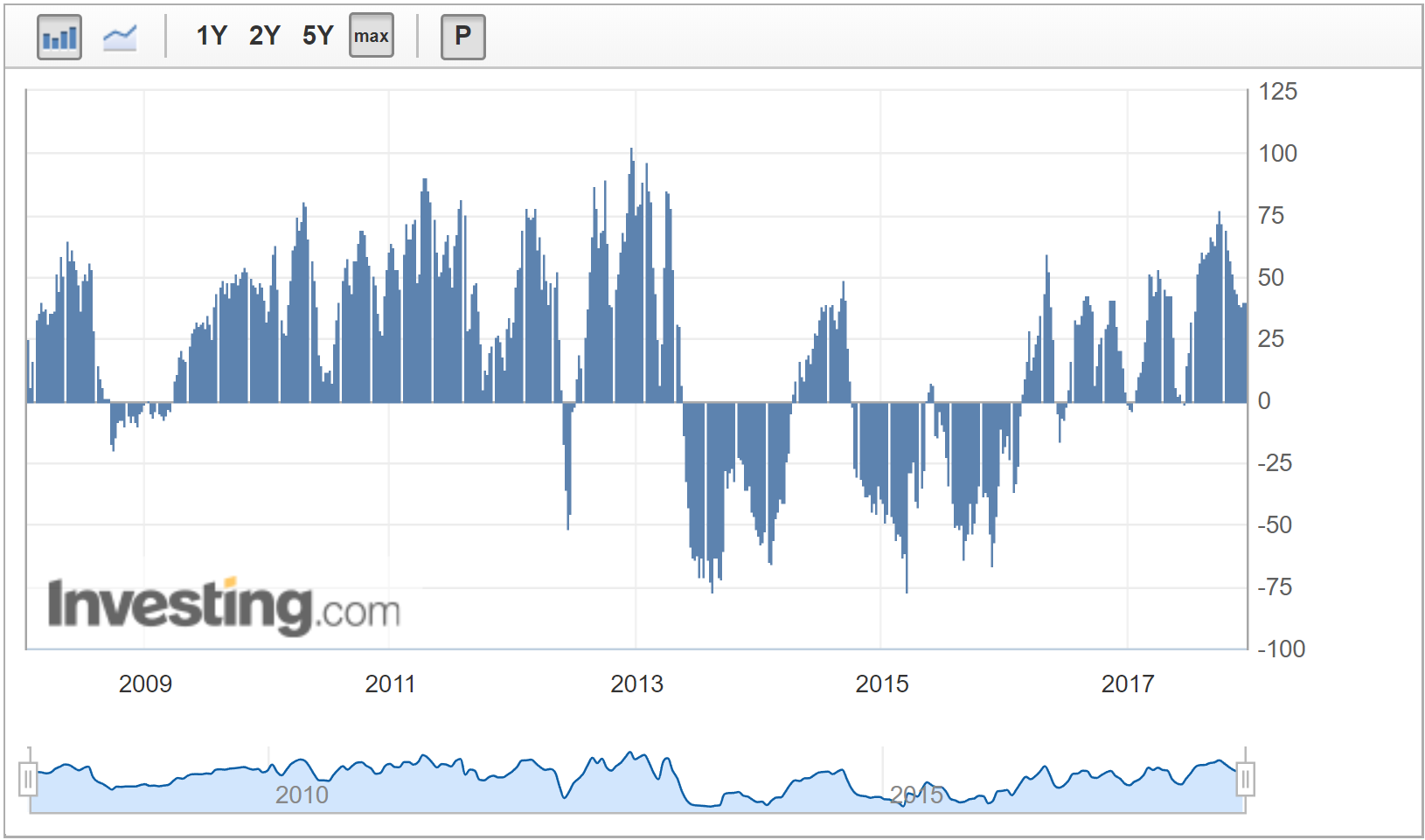

AUD CFTC speculative positioning lifted slightly to 41k last week, still moderately long:

Gold held:

Advertisement

Brent too:

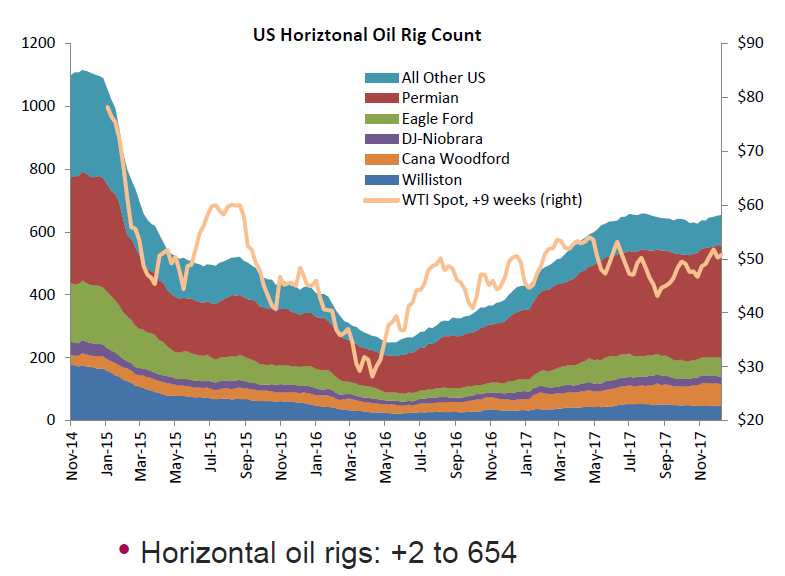

US rigs fell a bit last week but a new rush is coming:

Advertisement

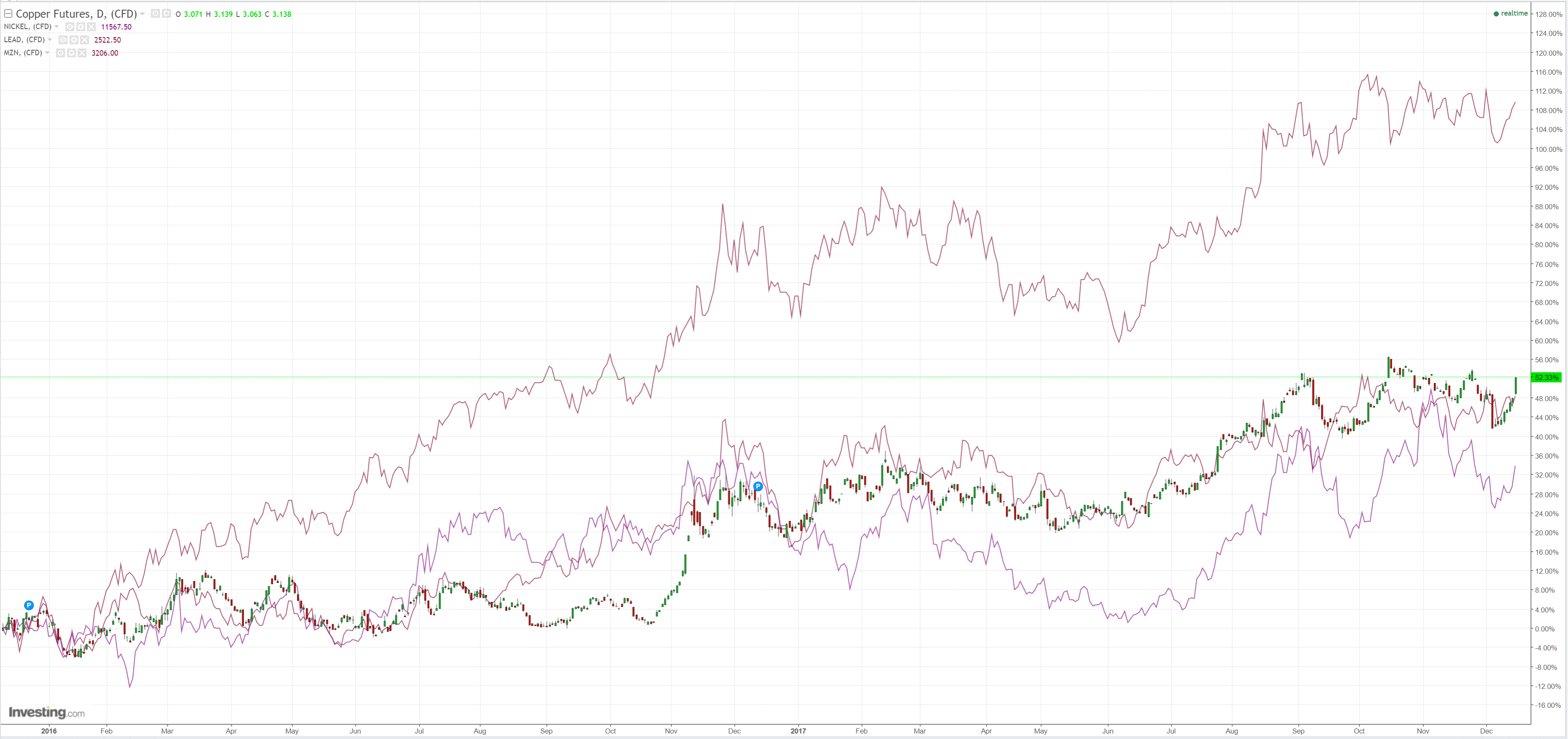

Base metals soared on growth hopes:

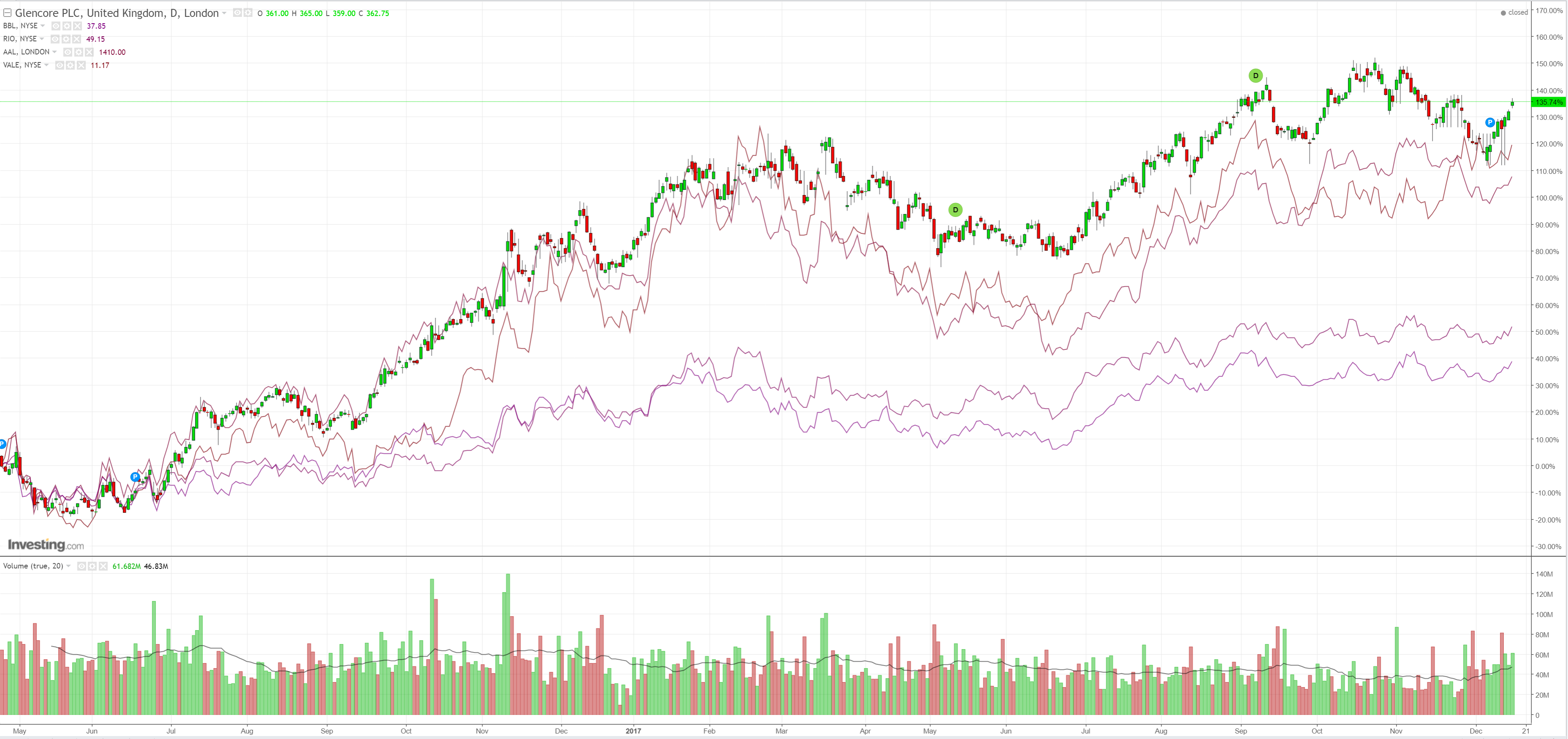

Big miners too as Bitiron joined in:

But EM stocks fell, sending another quiet warning:

Advertisement

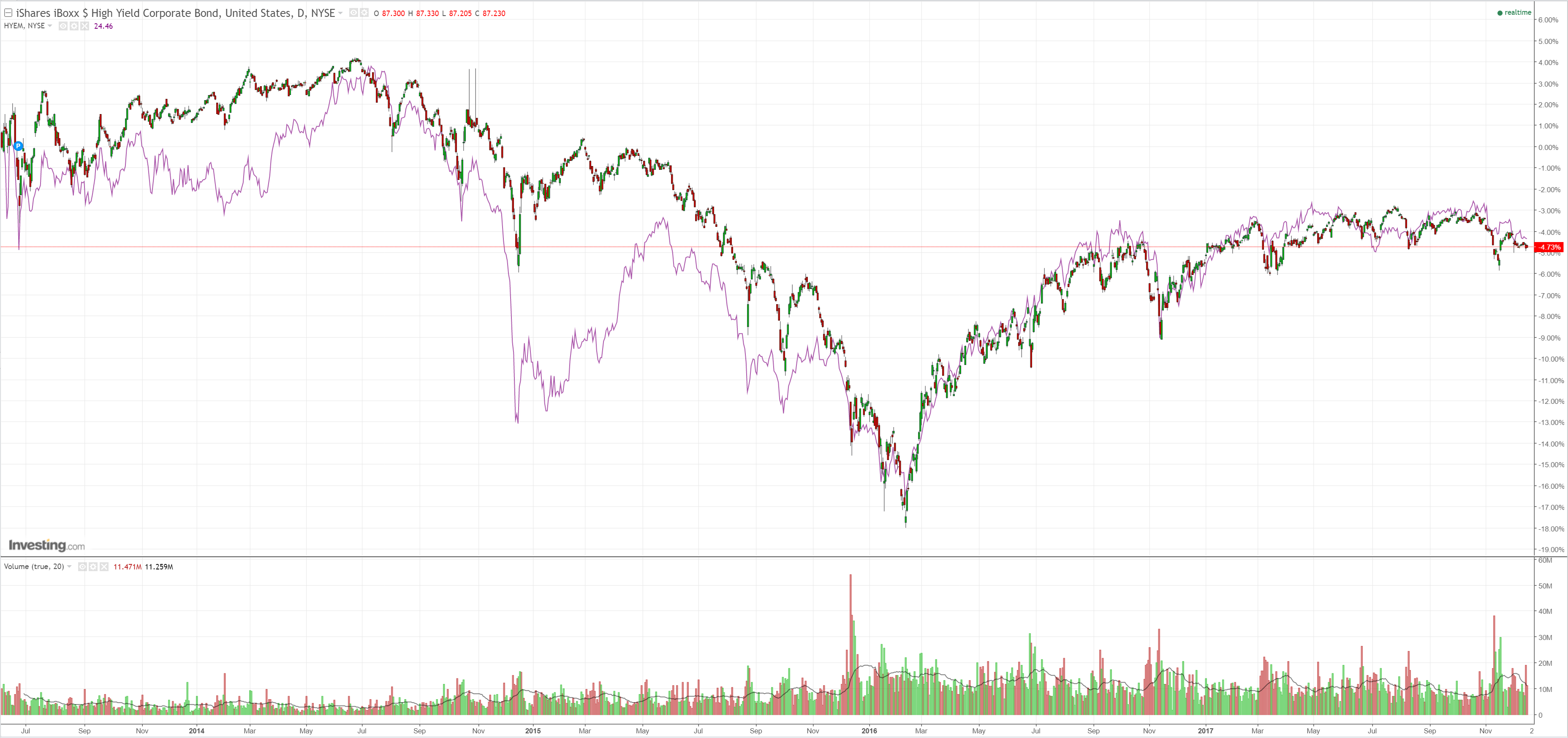

So did junk:

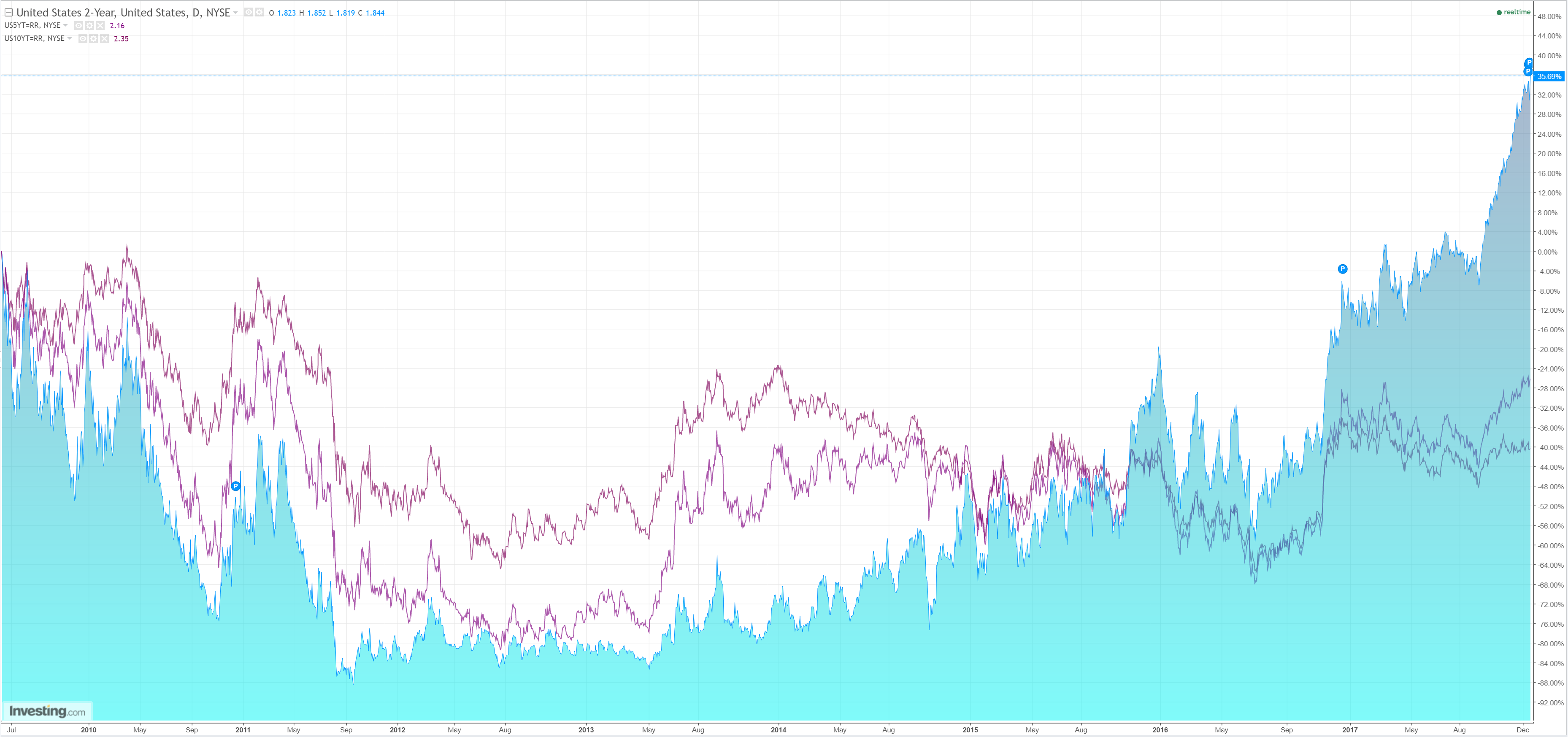

Treasuries were crushed but the curve flattened:

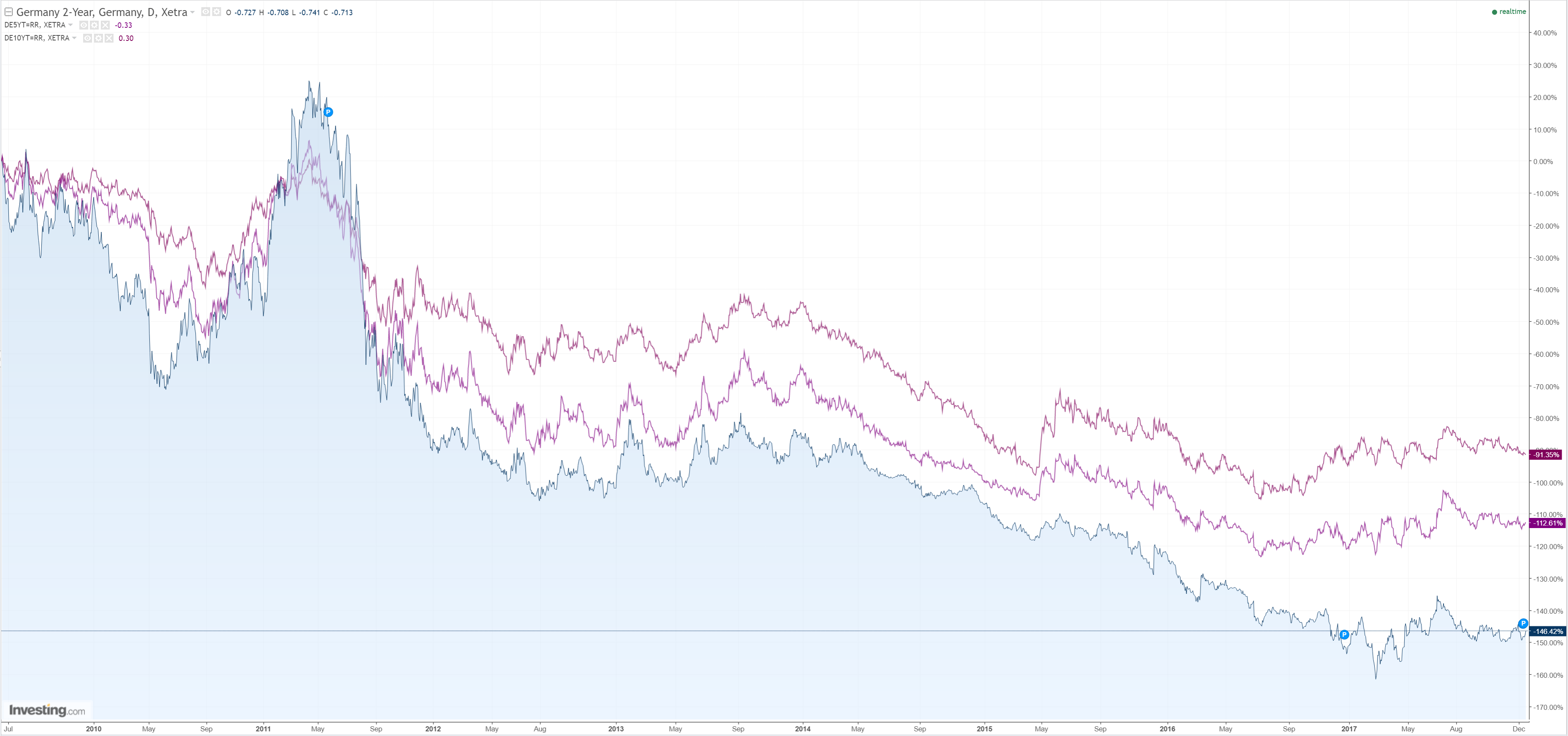

Bunds too:

Advertisement

Stocks flew to heaven:

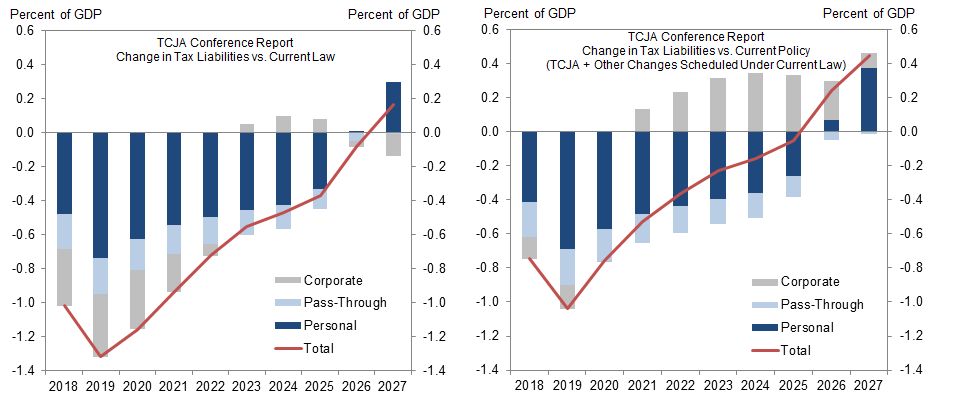

The Trump tax boom is go, via Goldman:

The tax cuts would be somewhat more front-loaded than Senate-passed plan and our own estimates. The revenue estimates of the conference agreement released by the Joint Committee on Taxation (JCT) suggest that, on a calendar year basis, the tax cut will be equal to 1% of GDP in 2018 and 1.3% of GDP in 2019 compared to a “current law” baseline that assumes several tax incentives expire on schedule (left panel of Exhibit 1). However, compared to policy as it stands today, the tax cut would equal 0.75% of GDP in 2018 and 1% of GDP in 2019. This is 0.6% of GDP greater in 2018 and 0.2% greater in 2019 than our assumption based on the Senate-passed bill. However, since most of the difference relates to the corporate tax cut taking effect in 2018 rather than 2019 as under the Senate bill, our preliminary take is that the growth effect should not be substantially different than the roughly 0.3% of GDP boost in 2018 and 2019 we previously estimated.

The corporate tax rate would be reduced to 21% starting in 2018. This increases the aggregate size of the tax in 2018 but does not create an incentive for businesses to pull forward capex and other deductible expenses as had appeared likely if the tax cut had taken effect with a delay starting in 2019. The corporate alternative minimum tax would be repealed, as expected.

The limitation on business interest deductibility represents a compromise between the House and Senate. For the next four years, through 2021, businesses (corporations as well as passthroughs) may deduct interest up to 30% of earnings before interest, taxes, depreciation, and amortization (EBITDA). Starting in 2022, this limit would become more restrictive, at 30% of earnings before interest and taxes (EBIT).

The restriction on net operating losses (NOLs) became incrementally more restrictive than prior versions. Under the final agreement, NOLs could not be carried back, as expected, and while they could still be carried forward, they could be used to offset only 80% of a company’s income, rather than the 90% previously proposed.

The international corporate provisions largely resemble the Senate’s provisions, as had appeared likely. The final bill includes a modified version of the Senate’s Base Erosion and Anti-Avoidance Tax (BEAT) as well as a modified version of the tax on global intangible low-tax income (GILTI). The minimum tax rate on such income would be set at an effective minimum tax of 13.125%. The agreement also imposes a slightly higher tax rate on accumulated untaxed foreign earnings (“deemed repatriation”) than the House or Senate bills; the final version would tax earnings held in liquid investments at 15.5%, other untaxed foreign earnings at 8%. Future foreign earnings (whether repatriated or not) would not be taxed by the US unless they are subject to the GILTI tax.

On the individual side, the top marginal rate declines to 37%, as opposed to 38.5% under the Senate bill and 39.6% in the House bill. Additionally, it allows state and local tax deductibility – including property as well as income – up to $10k. The final agreement allows mortgage interest deductibility with mortgage principal capped at $750k (existing loans will be grandfathered), but it disallows home equity debt-related interest. The individual AMT remains in the conference agreement, but with increased exemption amounts and phaseout thresholds.

Pass-through provisions are similar to the Senate version, but the deduction rate is lowered to 20% (from 23%) of eligible income. Taxpayers with income over a threshold of $315k (down from $500k) face additional restrictions. This further deters high-income taxpayers from using the deduction for wage income. Qualified REIT dividends, cooperative dividends, and publicly traded partnership income is eligible for the 20% deduction.

We expect the House to vote on the plan Tuesday, Dec. 19, and the Senate to vote on Wednesday, Dec. 20. With public announcements from Sens. Corker (R-TN) and Rubio (R-FL) that they plan to vote for the bill, the probability of passage looks very high. That said, Sens. McCain (R-AZ) and Cochran (R-MS) have missed votes recently due to health issues and there has not yet been any formal announcements from Sens. Collins (R-ME), Flake (R-AZ), or McCain (R-AZ) on how they plan to vote. While there is still some uncertainty, all of these senators look more likely than not to support the final bill. The bill needs 50 senators to vote for the bill, assuming Vice President Pence breaks the tie, meaning that the bill can pass as long as no more than 2 of the 52 Senate Republicans votes against the bill or is absent. Prediction markets now put the odds of enactment before year end at around 90%.

That’s a much stronger corporate tax result than many expected and is enough to trigger a roughly 10% lift in S&P earnings next year by itself. That’s before the various repatriation measures also flood US corporations with cash, leading to a boom in capital management strategies such as buy-backs, deleveraging and mergers and acquisitions. This is short term stock market boom 101 policy-making.

Advertisement

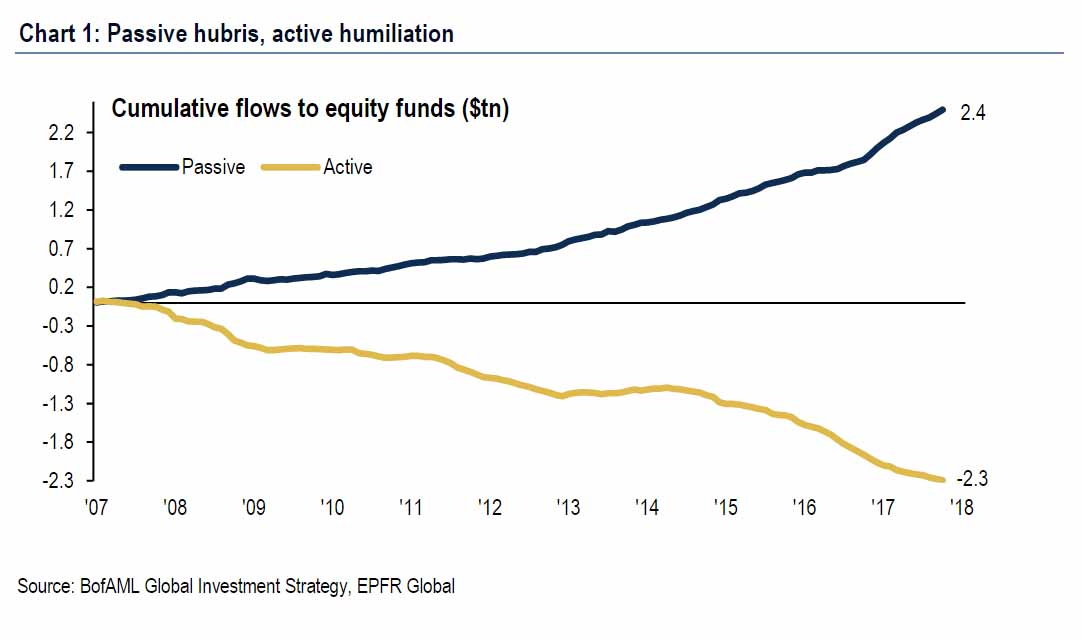

BofAML is seeing more signs of a growing bubble:

Passive hubris, active humiliation: 2nd largest week of inflows ($31.4bn) ever into equity ETFs vs 4th largest week ever of outflows from equity mutual funds (Chart 1)

…investors respond to Fed hike & US tax reform with biggest inflows to US large cap since Apr’17 and biggest inflows to US value since Mar’17;”

Yet there is still no inflation and it is inflation that kills bubbles:

Advertisement

Ambrose Evans-Pritchard sums up the moving parts nicely:

The tectonic plates of the world economy are shifting in opposite directions. China is winding down fiscal stimulus very quickly and will be in soft-slump conditions by the middle of next year; the U.S. is on the cusp of overheating.

This unfamiliar mix will kill off the “Goldilocks” era that has so seduced us. It is likely to catch the analyst fraternity off-guard, judging by the “macro forecasts” for 2018. Goldman Sachs may have to paddle back on oil and copper. A global commodity boom with China on the sidelines is hardly possible. The Chinese central bank (PBOC) is keenly aware of the danger. It has drawn up a contingency plan, fearing that China may be compelled to “shadow” rate rises by the U.S. Federal Reserve and tighten interbank lending into the teeth of a downturn.

What is certain is that everything bubbles will not survive the U.S. tightening cycle of 2018.

The PBOC is fretting about a “grey rhino” scenario where disastrously timed tax cuts by the Trump administration – at the top of the U.S. economic cycle, with the broad “U6” jobless rate at a 16-year low – will provoke a more ferocious retort from the Fed than markets assume. Traders have priced in one rate rise next year. What if U.S. core inflation spikes and the Phillips curve comes back to life, and there are instead four rises? Adam Posen, from the Peterson Institute, thinks the dollar index (DXY) could blast towards 110. If that happens, the tightening shock would hit East Asia with the force of a sledgehammer.

“Asia’s sweet spot looks stretched to us and we warn of a rising risk of a potentially painful snapback. High debt leaves it exposed to a global repricing of credit risk, possibly triggered by inflation surprises,” said Rob Subbaraman from Nomura. “We believe that 2018 will be the year that China starts to address its moral hazard problem. We see a greater risk of a spike in credit defaults and capital flight,” he said.

Capital Economics says its proxy gauge of Chinese output has dropped to 5.2 per cent from a blistering pace of 6.6 per cent in July, and is likely to slow to 4.5 per cent next year. China’s fixed asset investment has already begun to contract in real terms. The slowdown is heading for levels that set off the recession scare in 2015. The Fed quietly came to the rescue on that occasion by suspending rate rises: this time the U.S. cycle is far more stretched.

Let us assume the Republicans pass US$1.4 trillion of unfunded tax cuts for the next decade, with “front-loaded” stimulus adding 0.8 per cent to America’s GDP growth in 2018.

Let us assume too that U.S. corporations repatriate a fifth of their estimated US$2.6 trillion of offshore funds to take advantage of a one-off 14 per cent tax holiday, whether switching from euros, yen, etc into dollars, or switching the money from the offshore dollar funding markets to the U.S.

Either sends a powerful impulse through global finance. Despite the rise of China and the creation of the euro, the world has never been so dollarized, or so highly geared to U.S. lending rates. The Bank for International Settlements says offshore dollar funding has risen fivefold to US$10.7 trillion since the early 2000s, with a further US$14 trillion of global dollar debt hidden in derivatives. BIS research suggests that the ups and downs of the dollar – and the cycle of dollar liquidity – are what drive the world’s animal spirits and asset prices. This liquidity spigot is clearly being turned off. The Fed is not just raising rates, it is also reversing bond purchases.

We will learn in 2018 just how much tolerance there is for an aggressive Fedand a dollar squeeze in a global economy where debt ratios have risen to a record 327 per cent of GDP, up from 276 per cent a decade ago, and this time emerging markets have been drawn into the quagmire as well.

My guess is that tolerance will be low. It is hard to see how the “everything bubble” could survive 100 basis points of rapid tightening.

Needless to say, the Fed will reverse course if there is carnage on the equity and credit markets for fear of blow-back into the U.S. economy. The world will be saved again. But first you have to have the carnage. The wild card is China. Its breathless “stop-go” lurch from boom to bust, to boom again, is nearing its limits. The once inexhaustible flow of rural migrants into the cities has dried up, knocking away the key prop for housing. Capital Economics says total demand for square footage peaked in 2013 and will decline 5-10 per cent per year from now on. A sector that once powered 16 per cent of Chinese GDP faces atrophy. Government spending has stepped into the breach. The International Monetary Fund thinks the “augmented fiscal deficit” hit 12 per cent of GDP this year, including spending by the regions.

The blast of stimulus over the last two years matches the post-Lehman spree in 2009. It is the chief reason why the global economy has sprung back to life, which raises awkward questions over what happens when it goes into rapid reverse.

The latest spending was political, culminating in a crescendo of infrastructure projects months before the consecration of Xi Jinping. Growth pulled forward from the future propelled Xi into the Communist pantheon alongside Mao. His thoughts now have constitutional status.

This has been a Faustian pact: the future eventually arrives. Non-financial debt has galloped up to 300 per cent of GDP. Yes, the banking regulator Guo Shuqing has been clamping down on shadow banking since February. This has hit smaller private firms the hardest. They face a credit crunch. There has been no such discipline for the state-owned behemoths (SEOs) that gobble up most bank loans. Xi’s pledges to cleanse these instruments of patronage have come to nothing. He needs them too much to maintain the iron grip of the Communist Party.

It is possible for a state-controlled banking system to roll over bad debts almost indefinitely. What it cannot do so easily is to conjure away funding problems. The mid-tier banks rely on short-term market finance to cover 34 per cent of lending, mostly on maturities below three months, like Northern Rock and Lehman. This is why the IMF has warned of a “funding shock” and a fire-sale of assets in a broken market if liquidity ever dries up, and why the PBOC’s governor has been muttering about a “Minsky moment.”

China has large foreign reserves and exorbitant domestic savings. It can weather a bout of stress. Whether those dependent on the Chinese economy are so well protected is another matter. What is certain is that “everything bubbles” will not survive the U.S. tightening cycle of 2018.

A couple more points for nuance:

Advertisement

MB is slightly less bearish on China than 2015 given housing will slow slowly and fiscal support persist plus external demand be solid. But the slowing is certain and material for commodities;

Winter shutdowns are distorting everything in and around China for now, offering cover for slowing Chinese data and allowing markets, particularly commodities, to ignore weakening underlying demand through Q2 2018. However, beyond that all bets are off;

we’re also a little less hawkish on Trump tax stimulus. Like all things these days, the big impacts will be on asset not real inflation. US inflation will firm but not tear away so the Fed will hike twice on balance, is our bets guess.

The lesson for Aussie investors is simple. It’s Trump boom time, then bust by the Fed’s hand, or by China’s, later next year. Either way, the Australian dollar cops in the neck in 2018 and, if we see both, then it will crash.

Precisely the MB Fund play book.

David Llewellyn-Smith is chief strategist at the MB Fund which is currently long local bonds and international equities that offer superior growth and benefit from a falling AUD so he is definitely talking his book.

Advertisement

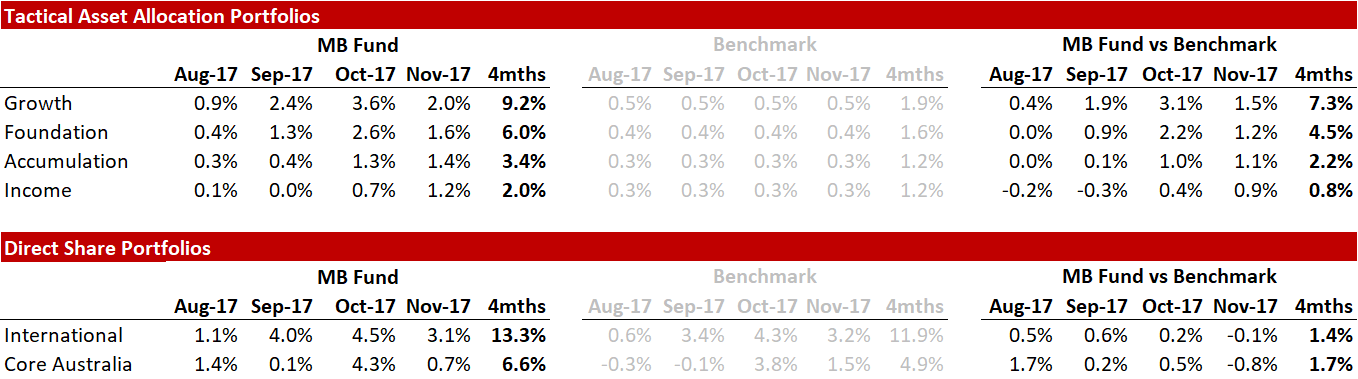

Here’s the recent fund performance:

Source: Linear, Factset

The returns above include fees and trading costs on a $500,000 portfolio. Note that individual client performance will vary based on the amount invested, ethical overlays and the date of purchase. The benchmark returns do not include fees. October monthly returns are currently at 4.9% for international and 4.2% for local shares.

If the themes in this post and the fund interest you then register below and we’ll be in touch:

The information on this blog contains general information and does not take into account your personal objectives, financial situation or needs. Past performance is not an indication of future performance. The MB Fund is a partnership with Nucleus Wealth Management, a Corporate Authorised Representative of Integrity Private Wealth Pty Ltd, AFSL 436298.

——————————————-

I’m off on holiday now and will return mid-January. Chris Becker and Damien Klassen will keep you up to date on markets in my absence. Have a happy and safe break.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.