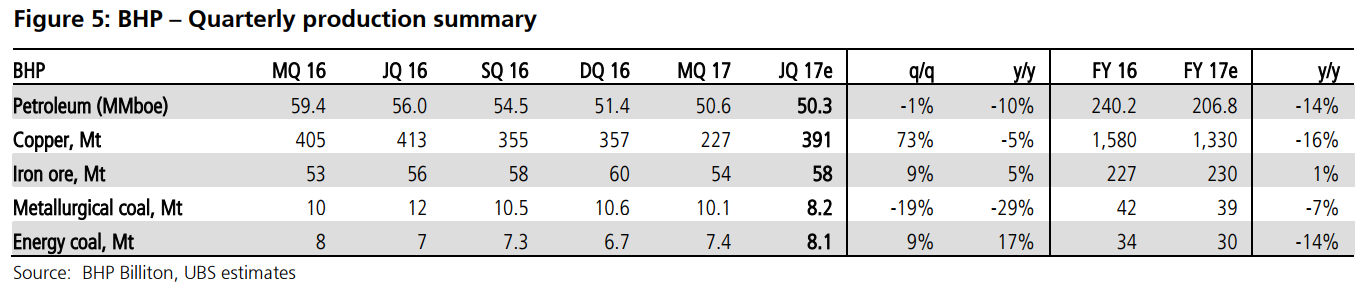

Iron ore shipments for the quarter from WAIO are forecast to be up ~13% sequentially at 70.8Mt (100% basis) based on vessel movements. This brings FY 17 shipments to 268Mt, a lift of 4% y/y. Global iron ore production (equity) is estimated at 58.4Mt, up 9% sequentially, and up 5% y/y. We see copper production up 73% on a sequential basis at 391kt vs 227kt in the March quarter, reflecting the strike at Escondida which impacted MQ production. BHP revised guidance for FY 17 copper production in April 2017 to 1.33-1.36Mt with Escondida at 780-800kt. UBSe for FY 17 is 1.33Mt. Coal production volumes for the quarter are forecast to be down 9% versus the March quarter at ~16Mt. We expect met coal production to drive the decrease as production was impacted by Cyclone Debbie at end March 2017. BHP in April 2017 lowered met coal production guidance for FY 17 to 39-41Mt (UBSe 39Mt) from 44Mt previously. Thermal coal production remained unchanged at 30Mt. We forecast a 1% decline in petroleum to 50.3MMboe versus 50.6MMboe in the March 2017 quarter. FY 17 production estimated at 207MMboe versus guidance of 200-210MMboe. FY 17 production split between US Onshore at 77-83MMboe and Conventional at 123-127MMboe.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.