By Gareth Aird, senior economist at CBA:

Key Points:

- Spare capacity in the Australian economy continues to weigh on inflation and wages growth.

- Labour market slack varies across the states reflecting divergences in state final demand.

- Talk of rate rises is premature because there is a significant amount of spare capacity in the economy.

Overview:

Australia remains stuck in a low wage, low inflation and low interest rate nexus. Domestic income has lifted recently due to big lift in commodity prices and the terms of trade. But the income boost has been largely confided to the corporate sector. Wages growth remains weak. The latest national accounts showed that both disposable real household income and the compensation paid to employees actually fell in QIV 2016 (chart 1).

Labour’s share of national income has declined because higher profits aren’t translating into higher nominal wages. There are a few reasons for this, but the primary one is that there is plenty of spare capacity in the labour market which reduces the ability of employees to negotiate pay rises. Productivity and the terms of trade are also important determinants of real wages growth. But the degree of labour market slack is the main driver of nominal wages growth and inflation at the moment.

In the past, the unemployment rate was deemed sufficient to measure labour market slack and therefore very little air time was given to the underemployment rate. But over the past two years it’s become increasingly important to talk about the underemployment because the spread been the unemployment and underemployment rates has been rising. We have written extensively over the past year about the economic and policy implications of slack in the labour market. But we haven’t yet drilled down to underemployment and underutilisation at the state level. In this note, we update our previous work on labour market slack and the implications for wages, inflation and monetary policy. And we expand our work to include a comparison with the US and an Annex that looks at labour market spare capacity by state.

National Picture

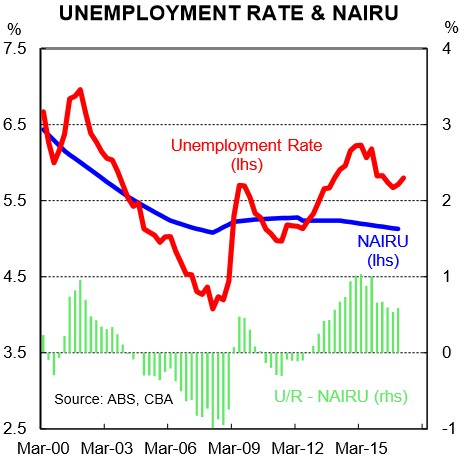

The unemployment rate trended broadly sideways over H2 2016, but lifted in the first two months of 2017. The latest employment report (February) put the unemployment rate at 5.9% – up from 5.7% in January and almost a full percentage point above where we put the ‘non-accelerating inflation rate of unemployment1’ (NAIRU). On this measure alone, the economy is operating below its potential and there is a fair bit of slack in the labour market (chart 2). But the unemployment rate only tells part of the story.

The underemployment rate lifted to a joint record high in February of 8.7%. The lack of full-time jobs growth has been accompanied by a rise in underemployment. To recap, people who are underemployment have a job but want to work more and can’t find the work. The number of additional hours of work wanted by underemployed workers has been stable at around two days (or a little under 15hrs) per week since the mid-2000s. This compares with unemployed people who are on average looking for an additional 33 hours per week.

The sum of the unemployment rate and the underemployment rate produces the underutilisation rate which is the broadest measure of spare capacity in the labour market – it is currently sat at 14½%, close to its highest point since the late 1990s.

Implications for wages

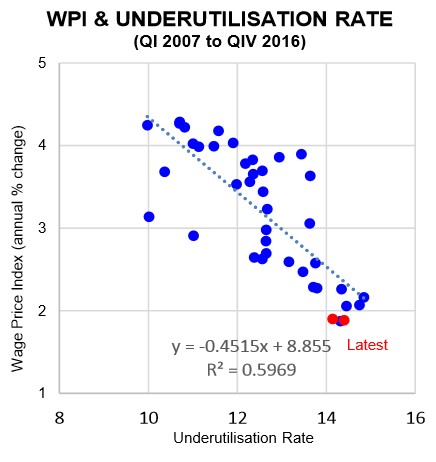

The lift in the underutilisation and associated increase in spare capacity in the labour market has contributed to a slowdown in wages growth (both real and nominal). Since mid-2010, wages growth has eased and is currently running at its lowest annual rate since the 1990s recession. A scatter plot (chart 3) shows we are currently at the least desirable place – high underutilisation and very low wages growth.

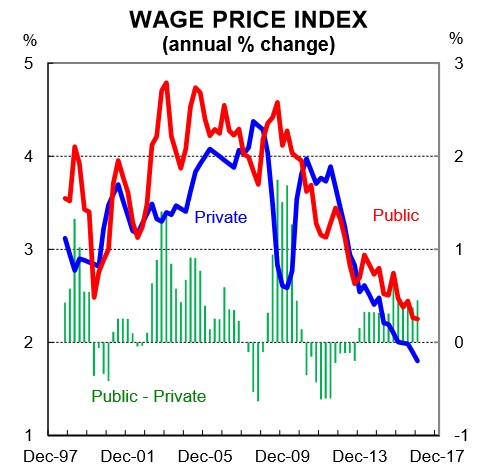

The decline in wages growth has been broad-based across the private and public sectors, though the public sector slowdown has not been as pronounced. The spread between annual public and private sector wages growth was a solid 0.5% in QIV 2016. In fact, public sector wages have been growing faster than those in private sector since March 2014. And more generally, over the past 20 years public sector wages growth has significantly outperformed the private sector (chart 4). Policymakers should take note!

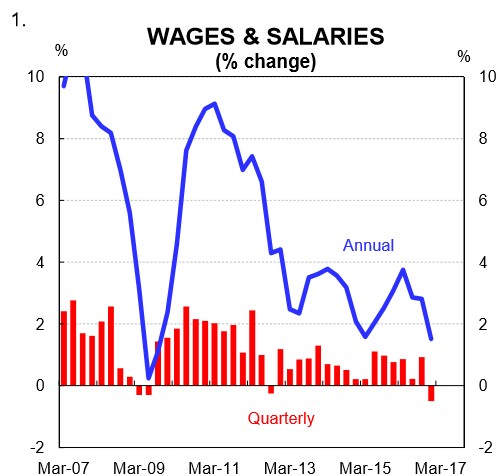

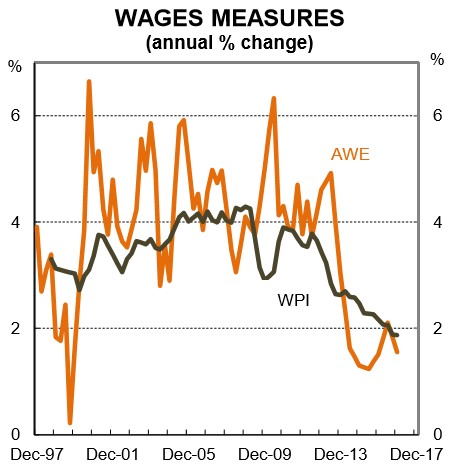

Most industries have experienced a slowdown in wages growth and the Wage Price Index was growing at a flaccid 1.9%pa in QIV 2016. The picture appears even softer when looking at Average Weekly Earnings (AWEs) which are running at just 1.6%pa (chart 5). The WPI measures changes in wages across a range of industries (just like the CPI picks up price changes for a basket of goods). But it doesn’t pick up compositional changes in the labour market. AWEs, however, do. Growth in AWEs has declined by more than growth in the WPI because of the shift in jobs away from higher paying mining-related jobs towards lower paid services sector jobs.

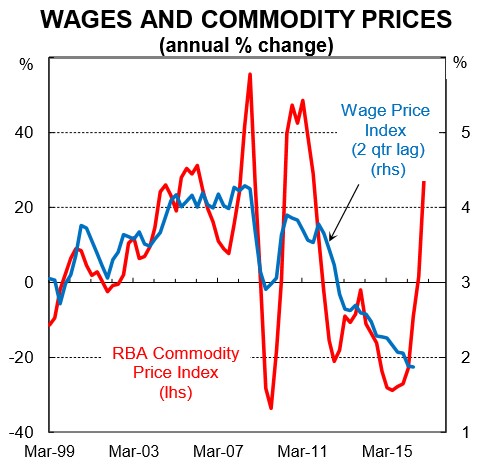

Historically, changes in commodity prices (i.e. the terms of trade) have been positively correlated with wages growth in Australia (chart 6). Wages growth could be expected to post a decent rise after the recent lift in commodity prices if history was to repeat itself. But we don’t see that happening this time around. The recent lift in commodity prices will not generate a lift in investment like in previous cycles and therefore the labour market is not expected to tighten. It’s a windfall to shareholders and a boost to the Government’s coffers. But without fiscal easing because of higher revenue, which we do not expect, the benefits of higher commodity prices won’t be spread around the economy more broadly. As such, labour market slack, and not commodity prices, will be the key driver of nominal wages growth over the medium term. And we don’t see the labour market tightening enough to generate a lift in wage inflation.

Implications for inflation

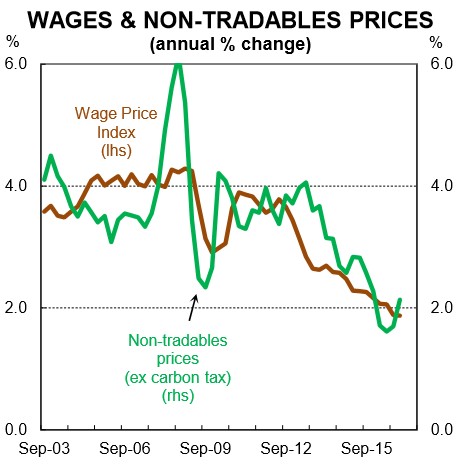

The impact of declining wages growth as a result of a lift in spare capacity has put downward pressure on non-tradables (i.e domestic) inflation (chart 7). At the same time, tradables inflation is barely positive and the recent strength in the AUD suggests some further downward pressure on the imported component of the CPI in H1 2017.

We expect domestic inflation pressures to remain weak primarily because spare capacity in the labour market will keep a lid on wages costs. Firmer commodity prices and global reflation will put some upward pressure on inflation in Australia at the margin. But wages growth is unlikely to lift until the unemployment rate gets closer to the NAIRU and underemployment falls. In our view, we are some way off that. The forward looking indicators of the labour market have improved more recently. But we think that there is a lot of spare capacity that needs be gobbled up to generate a broad-based lift in wages inflation.

In our view, core inflation bottomed out in Australia in QIII 2016. And the annual headline inflation rate looks to have hit its cyclical low point in QII 2016 at just 1.0%. That said, we don’t expect inflation to pick up materially in 2017 and essentially have the annual rate of underlying inflation tracking sideways in at around 1¾% range throughout the year – below the RBA’s target.

A comparison with the US

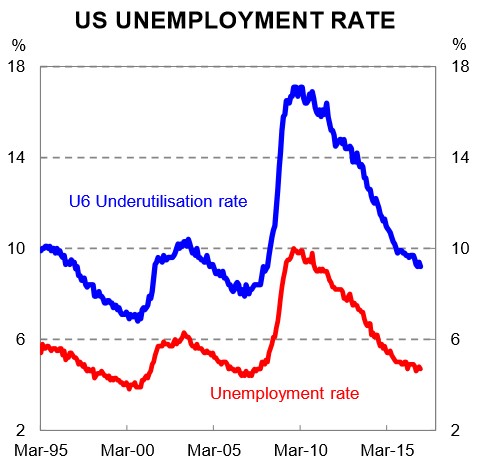

At present, conditions in the Australian labour market look quite different from those in the US. The labour market has been tightening in the US for many years and the unemployment rate has come down to where it currently sits at 4¾%. The underutilisation rate (U6) has also been falling (chart 8).

As a result, wages growth has accelerated with average hourly earnings growing at their fastest pace since mid-2009 (chart 9). The sustained tightening in the US labour market coupled with the rise in earnings has pulled US inflation higher. The FOMC has responded by raising the fed funds rates twice over the past few months (December 2016 and March 2017) following their first hike in December 2015. Further tightening is expected. This is very different to conditions in the local labour market which are characterised by elevated spare capacity which has pulled down wages growth and inflation.

We often hear from policymakers about how well our GDP growth rate stacks up against other OECD countries. But over the past few years we’ve heard very little about how the Australian labour market compares to other OECD countries. As we have flagged previously, the Australian economy doesn’t look as strong on a per capita basis as it appears on an aggregate GDP growth basis because strong population growth boosts aggregate growth rates.

Implications for the RBA

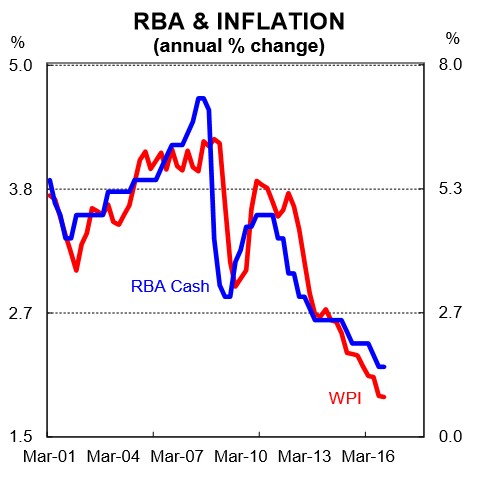

Normally we would say that the degree of spare capacity in the economy is paramount to monetary policy decisions because it is the primary driver of domestic inflation. And normally, the RBA’s views on the outlook for inflation would dictate near term rate moves. The RBA’s two rate cuts in 2016, for example, came purely down to the Bank’s concerns about entrenched low inflation and disinflation risks in part because of elevated labour market slack. Governor Stevens took a rigid approach to the Bank’s inflation target and cut rates as the rate of inflation fell. But the RBA’s reaction function has changed under Governor Lowe.

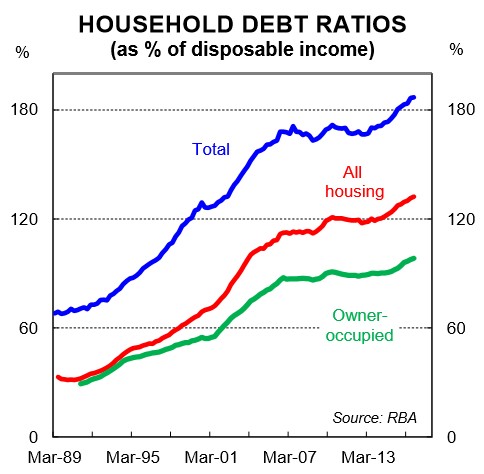

History now shows that in 2016 the RBA, under Stevens, underestimated the impact that rate cuts would have on the property market. Lending growth to investors and dwelling price growth took off again in Sydney and Melbourne after the RBA cut rates. It appears that this time they may have learnt their lesson. With Governor Lowe now at the helm, the RBA is placing a greater emphasis on financial stability. Indeed, the housing market looks to be a very important factor in monetary policy deliberations. As does the rising level of household debt to income (chart 11).

We see little chance of further policy easing despite weak wages growth continuing, the unemployment rate being above the level associated with full employment, underemployment remaining high and core inflation running below target. The consistent message from the RBA over the last six weeks has been that rate cuts are off the table. Only a new round of tighter macroprudential measures aimed at materially slowing lending growth to investors would bring back policy easing to the table.

When Governor Lowe appeared before the House of Representatives Standing Committee on Economics in late February he stated that, “the market pricing is for interest rates to be constant right through this year. That seems a reasonable proposition to me.” He further added that, “the main effect (of another rate cut) would be more borrowing for housing, pushing up housing prices.”

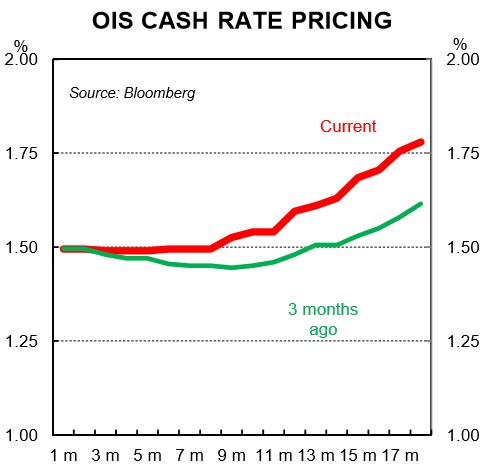

The risk of lower rates further stimulating activity in the housing market has all but ruled out another rate cut. But we very much doubt that the RBA would use its main policy lever to slow activity in the housing market while inflation is below target and spare capacity in the economy is elevated. It would be a very unusual move if it did. The market is pricing in a 60% change of a rate hike within the next 12 months (chart 12), but we cannot make or see the case for policy to be tightened. As such, we continue to expect the RBA to be on hold over 2017 and well into 2018.

ANNEX – Labour market slack, by State

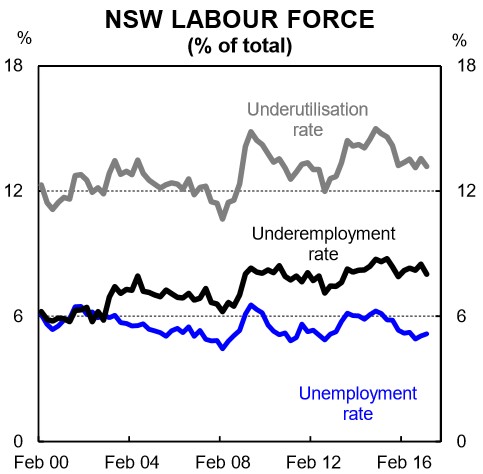

NSW

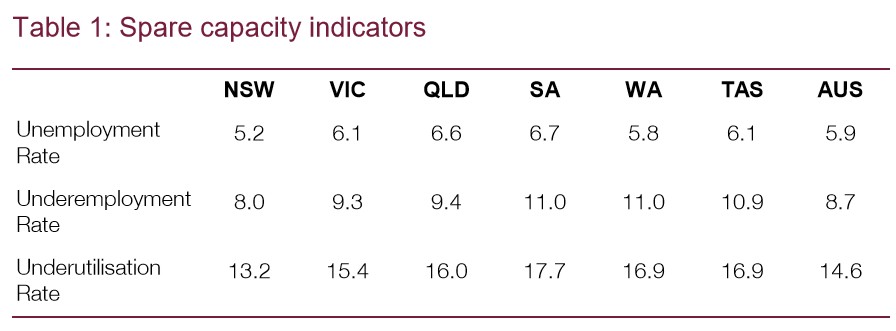

At present, Australia’s largest state has the tightest labour market (chart 13). The news isn’t too bad for job seekers in NSW. Both the unemployment and underemployment rates in the Premier state are the lowest across the states. The outperformance of the NSW labour market is broadly attributable to five factors: (i) a big lift in residential construction; (ii) positive wealth effects from an incredibly buoyant Sydney property market which have supported household consumption; (iii) a solid lift in public investment; (iv) a picking in non-mining investment from rate cuts and a lower AUD coupled with limited exposure to job losses from a downturn in mining investment; and (v) a solid lift in tourism exposed sectors because of massive lift in holidaymakers from China.

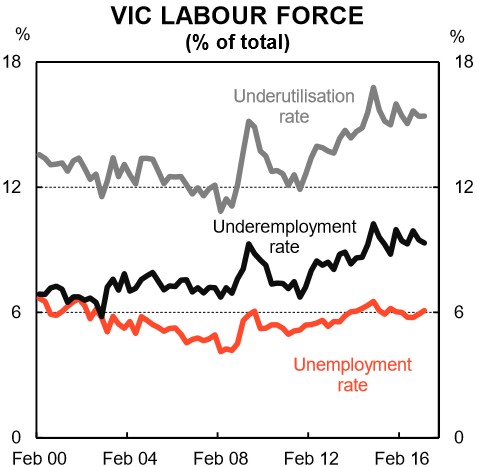

Victoria

Employment growth in Victoria is the strongest across the states, in large part because of a materially higher population growth rate. Spare capacity, however, remains elevated (chart 14). Solid jobs growth because of a fast growing population is not the same thing as having a tight labour market. In fact, despite Victoria being responsible for the bulk of Australia’s jobs growth over the past year, the trend unemployment rate has inched a little since mid-2016 and presently sits at 6.0%. Victoria’s underemployment rate has oscillated between 9 and 10% over the past year while underutilisation has been stuck above 15% since May 2014. These figures will not be helped by the closure of the car industry and the lagging impact it will have on local employment.

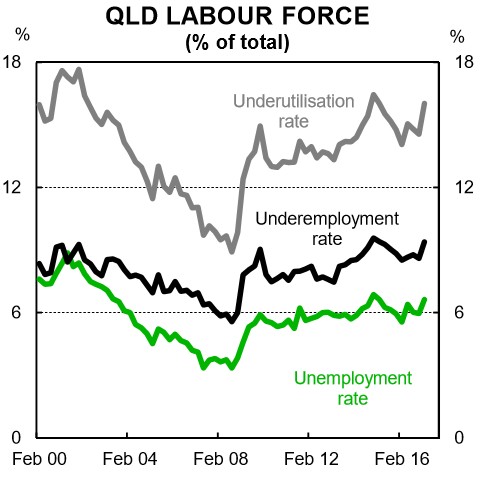

Queensland

The QLD labour market has plenty of slack in it despite the economy being relatively diverse (chart 15). The lower AUD has helped tourism-related employment but there have been a lot of job losses out of the resources sector. There are also some considerable differences in labour market outcomes throughout the state – notably between South East QLD and North QLD. The unemployment rate recorded a solid jump in February to 6.4% and notwithstanding the monthly volatility, the trend unemployment rate has been climbing. The underemployment rate also posted a solid lift in the three months to February taking underutilisation to its near cyclical high. Whichever you slice it, there is plenty of spare capacity in QLD’s labour market and the recent trend is somewhat concerning.

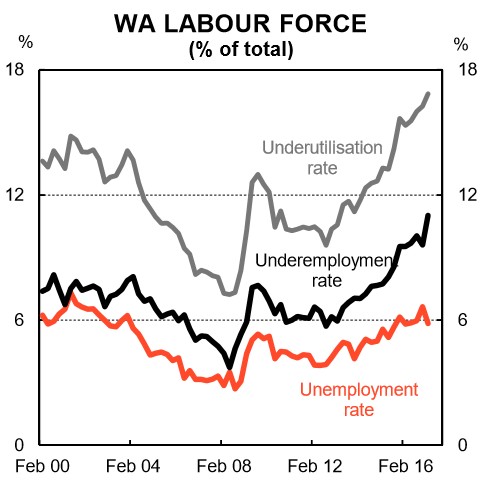

Western Australia

The WA economy has experienced recessionary type conditions in recent years because of the big downturn in mining investment and the associated jobs losses. In a positive development, WA’s unemployment rate eased to 5.8% in February. But the underemployment rate jumped sharply which took underutilisation to its highest level in 25 years (chart 16). WA has shed some 45k full-time jobs over the past two years while part-time employment has risen by around 40k. The net result has been for labour market slack to hit a multi-decade high which highlights just had badly the state has been hit by the downturn in mining investment. The lift in hard commodity prices over the past six months has been much welcomed. But it won’t translate into a lift in investment like it did a decade ago. As such, the outlook for labour demand in WA remains weak and we expect the unemployment rate to drift up to 6½% .

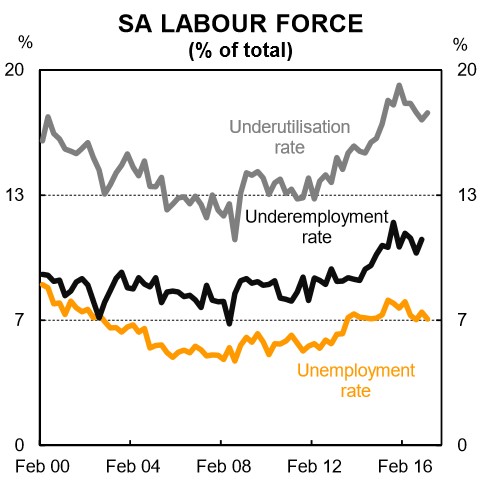

South Australia

The SA labour market is the weakest across the states (chart 17). Things have been poor for a long time for job seekers in the ‘festival state’. SA has the unenviable claim to being the state that has both the highest unemployment and underutilisation rates. In February, a whopping 17.7% of SA residents either couldn’t get a job or were looking for more work. The good news is that the underutilisation rate in SA looks to have peaked at 19.2% in November 2015 and has since moved a little lower. Notwithstanding, the overall level of slack in the SA labour market is incredibly high. Without a new long term growth engine or two it is hard to see the labour market materially tightening over the next two years.

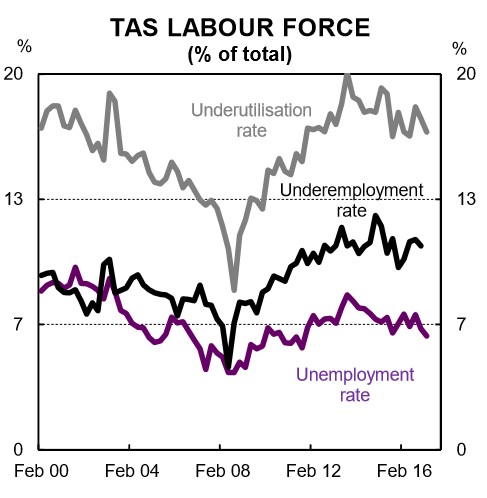

Tasmania

There are similarities between the SA and Tasmanian labour markets. The labour market is weak and conditions are soft (chart 18). But there has been some gradual improvement in conditions as evidenced by the modest downward trend in the unemployment rate. Notwithstanding, the overall level of underutilisation remains high and there is plenty of slack in the Tasmanian economy.