Robert Gottliebsen (“Gotti”) has penned a warped piece slamming recent changes to the Aged Pension and cheering on the proposals to allow retirees to downsize their homes without affecting their pension or superannuation entitlements, as well as allowing first home buyers (FHBs) to access their superannuation to purchase a home. From The Australian:

Because bad decisions by previous treasurer Joe Hockey were not reversed, Australia is putting a big financial penalty on older people in certain asset brackets not to downsize their home and outrageously incentivising them to spend their money on cruises by giving them a 7.8 per cent return on every dollar of assets disposed.

The Abbott government policy, which came into operation around January 1, 2017, will be a big cost to our long-term pension bill, albeit there is a substantial short-term revenue gain. That’s worst type of decision making, and voters know it…

Then, this week, a breakthrough, The Australian’s David Crowe reported that the federal government will move within weeks to break down barriers that discourage older Australians from “downsizing” to smaller homes. There is a lot more to do but at least it’s a start…

By allowing young people to access superannuation for a deposit you help them acquire the greatest asset they can have in retirement — a dwelling. You also substantially reduce the cost of keeping them when they retire.

Planning such a superannuation exercise requires expertise that will not exist in Treasury but help is available outside of Canberra.

To be fair to Gotti, he does at least state that cutting negative gearing is necessary, but then claims “the Bowen plan is very dangerous because it would slash the price of dwellings because investors could not support the secondary housing market”.

Still, his other policy advice, if pursued, would be incredibly destructive to the Budget, as well as make the housing situation even worse.

Let’s first consider Gotti’s criticism of the pension reforms.

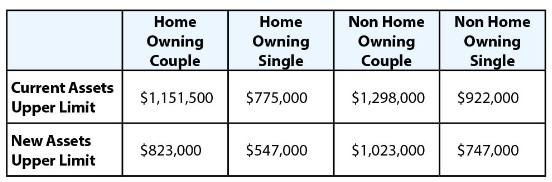

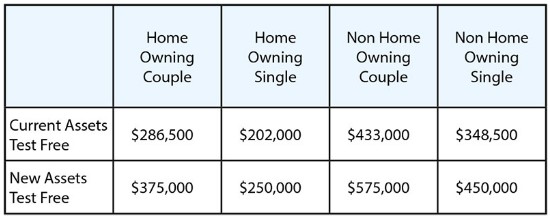

To recap, the 2015 Budget announced that the thresholds for the Aged Pension would be adjusted so that those with financial assets (in addition to the family home) of $547,000 for singles ($823,000 for couples) will no longer qualify for the part-pension (see below table).

According to these changes, financial assets above $375,000 for a couple will lose access to the Aged Pension at the rate of $3 per $1,000 in assets, up from $1.50 currently. It is important to note that this change merely restores the settings back to their pre-2007 state before Treasurer Peter Costello recklessly loosened the financial assets test.

However, while access to the part pension has been curtailed, the assets threshold has also been increased, thus benefiting those retirees with fewer financial assets (see below table).

Thus, the pension changes implemented in January will make the system more equitable. As such, they are supported by the Australian Council of Social Services, which noted the following after their passage:

“The changes to the Pension assets test passed by the Parliament last night help ensure that the Pension is going to people who need it, including improving the adequacy for people who have limited assets. The tightening of the assets test to pre-2007 levels reinforces the role of the pension as a safety net payment to prevent poverty,” said Dr Cassandra Goldie.

“ACOSS also welcomes passage of legislation abolishing the Seniors Supplement. This Supplement is very poorly targeted, going to older people who are not eligible for the Age Pension due to their substantial assets”.

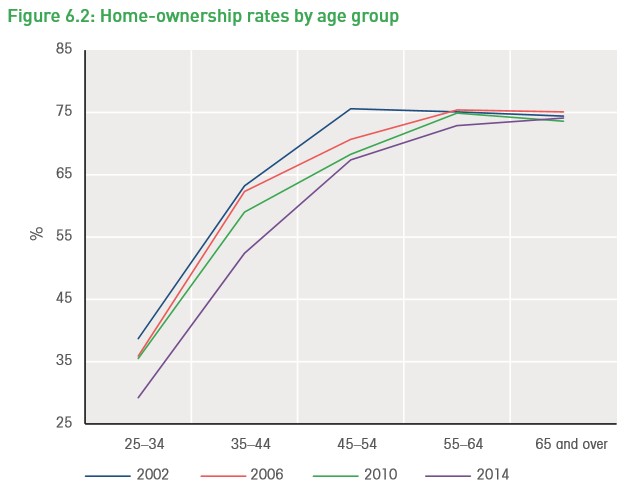

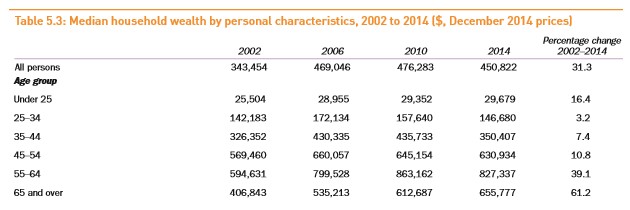

What Gotti also fails to mention is that the 75% of retirees that own their homes (most outright) have enjoyed massive windfall gains in wealth, thanks to the mammoth surge in Australian home values over the past 20 years (see below graphics).

This surge in retiree housing wealth has come at the direct expense of their children and grand children, whose wealth has barely increased, and who are now either locked-out of housing altogether or are required to undergo a lifetime of debt servitude in order to pay off a home.

How is it fair that these same mega-mortgaged or renting younger Australians are expected to fund the retirements of older home owners, who are in many cases far wealthier than they are?

This brings me to Gotti’s support of older Australians being allowed to downsize their homes without affecting their pension or superannuation entitlements. Again, there would likely be a significant cost to the Budget from this policy, which means that younger people’s taxes would need to rise in order to pay for the bloated entitlements of those who had the good fortune of purchasing their homes cheaply before they skyrocketed in value.

If Gotti cared at all about equity he would instead argue to:

- Include one’s principal place of residence in the assets test for the Aged Pension at some point in the future (e.g. 1 July 2020), thus allowing current retirees and prospective retirees adequate time to make arrangements.

- Raise the overall pension asset test threshold as well as the base rate.

- Extend the existing state sponsored reverse mortgage scheme, the Pension Loans Scheme, to all people of retirement age so that asset (house) rich retirees can continue to receive a regular income stream in exchange for a HECS-style liability that is recoverable from the person’s estate upon death, or upon sale of the person’s home (whichever comes first).

Under such a plan, asset rich pensioners choosing to remain in place could continue to receive an income stream as they do now under the Aged Pension, but with less drain on the Budget and on younger taxpayers. But they would similarly be incentivised to move as the family home would no longer be viewed as a tax free shelter. Poorer ‘house-less’ pensioners would also be made better-off via the combination of a higher asset test threshold and a higher pension base rate.

Finally, allowing FHBs to access their superannuation for a housing deposit would be disastrous. Not only would it be inflationary for house prices (and self-defeating from an affordability perspective), but it would cost the Budget billions in foregone revenue while placing Australia’s retirement system at risk.

Pandering to rent-seeking dunces is clearly not working for the Turnbull Government in the polls and any government MP tempted to follow Gotti’s hideously biased advice needs their head read.