From Credit Suisse comes the following assessment of east coast gas cartelier, Santos:

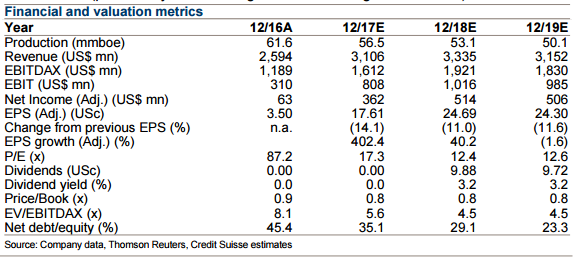

■ Largely uneventful result Underlying CY16 NPAT came in at US$63m, the top end of a very wide consensus range, but below our ~US$90mn estimate. The long awaited CY17 production cost guidance was relatively uneventful too, seemingly broadly flat at US$8-8.50/boe vs CY16 at US$8.45/boe.

■ This is not currently a sustainable business at US$40-60/bbl

Our definition of sustainable is keeping the same level of reserves and production steady through

■ This is not currently a sustainable business at US$40-60/bbl

Our definition of sustainable is keeping the same level of reserves and production steady through cycle. Santos seems to define it as producing their current reserve base. With 2P organic reserve replacement of 3%, 0%, 0% and 19% over the past four years the hopper is clearly not being filled. Indeed, the current capital spend seems to largely only produce developed 2P reserves, it needs to step up (GLNG and Cooper in particular) to produce undeveloped. To be fair, the Samter household often grapples internally with a view on what sustainable spending is as well. Sadly that is usually an issue of overspend, not underspend though …

■ What are go forward development costs?

Whilst effectively Santos has provided go forward development costs at GLNG, which we continue to struggle to reconcile with other CSM projects or economic logic, we are keen to understand it more in the Cooper Basin. There

■ What are go forward development costs?

Whilst effectively Santos has provided go forward development costs at GLNG, which we continue to struggle to reconcile with other CSM projects or economic logic, we are keen to understand it more in the Cooper Basin. There was ~200PJ of 2P reserves that were deemed uneconomic in the FY15 reserve statement. Given price assumptions appear unchanged, it would seem logical that if go forward development costs had been reduced these reserves would be written back. In terms of price assumptions, with much focus still on the ability to reprice “legacy” contracts (is anything legacy less than 10% of the way through contract life?), it would be hard to argue any repricing is needed if the Cooper is generating ~US$100m of FCF at the low oil prices of CY15.

■ Tweaks to earnings and valuation

We have lowered earnings by ~US$50mn in CY17 and CY18 on higher plant costs and pipeline tariffs than we had previously assumed. In terms of valuation, the net effect of numerous factors (the SPP, updated PNG LNG assumptions and particularly new lower restoration provision forecasts) is to move to $3.80/sh. It should be noted that the move in remediation provisions alone has added ~$0.35/sh – whilst Santos discussed this being US$311m lower

■ Tweaks to earnings and valuation

We have lowered earnings by ~US$50mn in CY17 and CY18 on higher plant costs and pipeline tariffs than we had previously assumed. In terms of valuation, the net effect of numerous factors (the SPP, updated PNG LNG assumptions and particularly new lower restoration provision forecasts) is to move to $3.80/sh. It should be noted that the move in remediation provisions alone has added ~$0.35/sh – whilst Santos discussed this being US$311m lower yoy, it is actually >US$500m lower than at 1H16. We dutifully model this number verbatim, but hold concerns about what might underpin these numbers (particularly asset lives given the declining reserve base).

This is the worst of the Curtis Island white elephants, not even operating as a viable business. Should it be nationalised?

We can’t just seize the reserves given we’re not a tin pot dictatorship but we could buy it. At $8bn in equity and $5bn in debt it’s a hefty price tag, though that could be offset by selling some assets.

Advertisement

You could perhaps force some kind of consolidation by selling the Curtis Island assets to Shell on the condition that they develop Arrow. But that comes with the problem that STO only owns 30% and the other partners Santos, PETRONAS 27.5%; Total 27.5%; and KOGAS 15% are not going to very impressed we forced losses onto their businesses. Neither should they be!

So there is not much point in discussing outright nationalisation.

An alternative path might be to make an offer to Shell and PetroChina for Arrow Energy which they bought in 2010 for $3.5bn with the intention of developing a fourth LNG plant. Its 17% of east coast reserves are just sitting the ground with the LNG plant now forgotten as the global glut builds. A public operation pumping those reserves at a dictated margin would benchmark local prices.

Advertisement

Another way of forcing the gas price down locally is to tax the exports and recycle the revenue as power subsidies for big gas consumers. A kind of Piguvian tax to offset the raging market failure now leeching the entire east coast economy.

Or you might put the two together, sit down with the cartel, and have a gentlemanly discussion about how it’s going to be one or the other!

Of course, all of this assumes a government interested in doing something over nothing.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.