For months, the Reserve Bank of New Zealand (RBNZ) has been in negotiation with the National Government to have debt-to-income (DTI) limits added to the Memorandum of Understanding on macro-prudential policy with the Minister of Finance, which would enable the RBNZ to deploy such measures if the need arose.

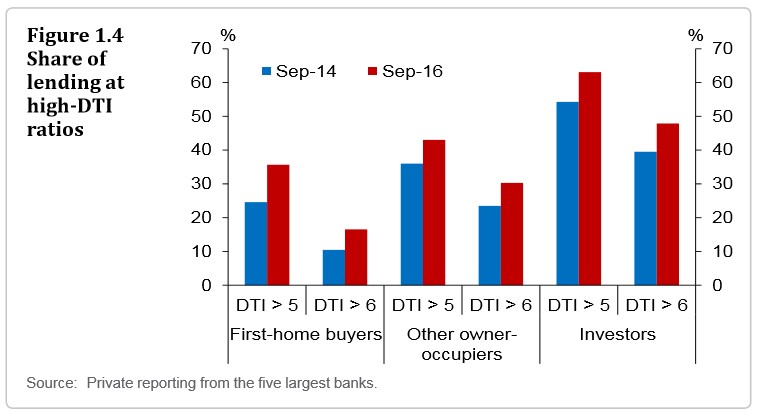

It is November Financial Stability Report, the RBNZ claimed that around a third of new mortgage lending was being conducted at a DTI ratio of over 6:

And that these “high DTI loans are at a higher risk of default in the event of an economic downturn, so an increasing concentration of this lending is of concern”. The RBNZ also noted that high DTI household are “likely to reduce consumption more sharply during a severe downturn, in an attempt to continue servicing loans and increase precautionary savings” and that “a number of studies have found that sharp falls in consumption by indebted households reinforced the economic impact of the GFC”.

Today, Interest.co.nz reports that a survey of bank executives reveals that the believe the RBNZ’s DTI ratio limit should be set between five and seven, but that many borrowers in New Zealand are already operating at levels between nine to 12:

The report notes bank bosses are in unanimous agreement that the Reserve Bank’s consideration of a DTI macro-prudential tool is happening too late given current DTI ratios have already topped levels that would have been considered ideal.

“According to executives an ideal DTI level would be in the range of five to seven. However, they say that most borrowers are already at levels of nine to 12,” the FIPS report says.

Both the Bank of England and the Central Bank of Ireland have introduced DTI ratios in recent years. The Bank of England’s DTI ratio of 4.5 applies to no more than 15% of the total number of new mortgage loans for owner-occupiers. And for Irish banks the DTI limit of 3.5 should not be exceeded by more than 20% of the value of all housing loans for owner-occupier homes during an annual period…

According to Interest.co.nz, the National Government has already delayed attempts by the RBNZ to get DTI limits added to its macro-prudential toolkit, instead requesting a cost-benefit analysis and stakeholder consultation before any decision is made.

It’s probably a wise move politically to delay any approval to after the 23 September general election. Because given the highly leveraged nature of many New Zealand mortgage holders, any implementation of DTI caps could become the pin that finally bursts New Zealand’s housing bubble.